Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Vietnam AI Infrastructure market reached USD ~ million, supported by rapid cloud migration, rising enterprise AI adoption, and expanding compute capacity needs for model training and inference. Demand is reinforced by local champions scaling AI platforms, increased deployment of accelerators for vision and language workloads, and higher requirements for data center-grade networking and storage. Public sector digital programs and private investment in AI factories and high-density facilities continue to push infrastructure upgrades.

Hanoi and Ho Chi Minh City anchor infrastructure buildout due to dense enterprise demand, major telecom and technology headquarters, and proximity to policy and procurement decision makers. These hubs benefit from stronger fiber connectivity, larger colocation footprints, and a deeper pool of AI engineering talent tied to universities and innovation centers. Da Nang is emerging as a secondary node due to tech parks and its role in attracting delivery centers and R&D. Investment partnerships between local firms and global chip and platform providers are concentrated in these cities.

Market Segmentation

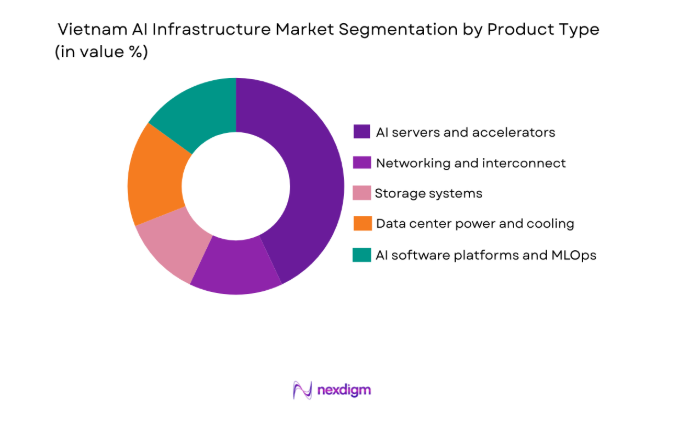

By Product Type

Vietnam AI Infrastructure market is segmented by platform type into hyperscale cloud platforms, enterprise private AI clusters, edge AI infrastructure, colocation AI ready data centers, and government and sovereign AI platforms. Recently, hyperscale cloud platforms has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The dominance is driven by fast GPU provisioning and scalable managed services that ease enterprise AI deployment. Expanding ecosystems and AI factory partnerships reinforce hyperscale consumption.

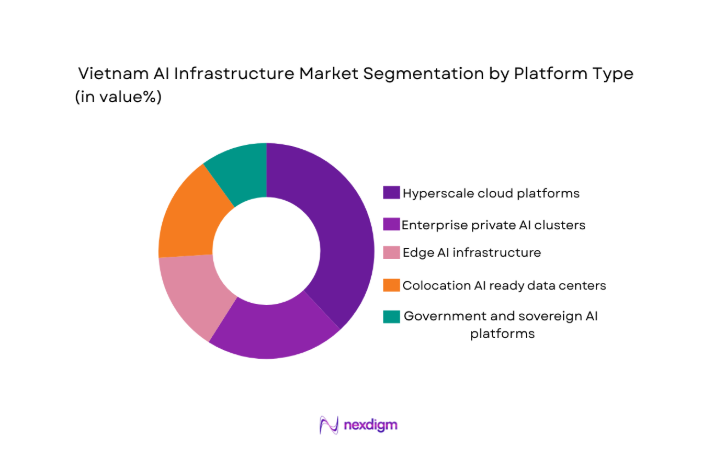

By Platform Type

Vietnam AI Infrastructure market is segmented by platform type into hyperscale cloud platforms, enterprise private AI clusters, edge AI infrastructure, colocation AI ready data centers, and government and sovereign AI platforms. Recently, hyperscale cloud platforms has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The dominance is driven by fast GPU provisioning, scalable storage, and managed services that simplify enterprise AI deployment. Strong ecosystems and AI factory partnerships further reinforce hyperscale led consumption.

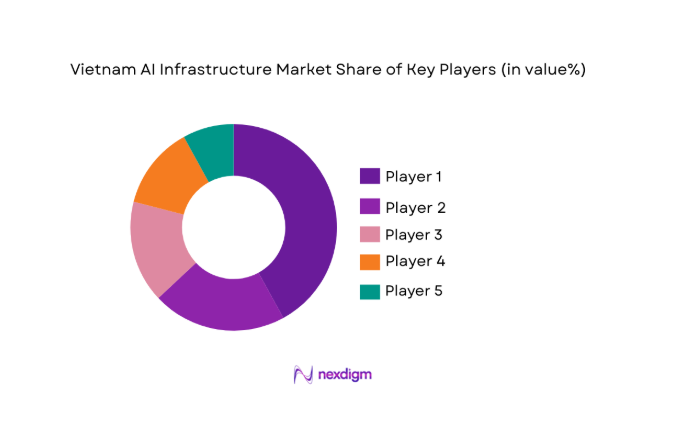

Competitive Landscape

The competitive landscape is increasingly consolidated around telecom groups and large technology integrators that combine connectivity, data center capacity, and AI platform delivery, while global chip and enterprise platform vendors shape reference architectures and accelerator supply. Partnerships and co investment models are prominent, with leading local players prioritizing AI factory buildouts, GPU supply access, and managed services bundling to capture enterprise demand as deployments scale.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI Infrastructure Footprint |

| FPT Corporation | 1988 | Hanoi, Vietnam | ~ | ~ | ~ | ~ | ~ |

| Viettel Group | 2004 | Hanoi, Vietnam | ~ | ~ | ~ | ~ | ~ |

| VNPT | 1945 | Hanoi, Vietnam | ~ | ~ | ~ | ~ | ~ |

| NVIDIA | 1993 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| IBM | 1911 | Armonk, USA | ~ | ~ | ~ | ~ | ~ |

Vietnam AI Infrastructure Market Analysis

Growth Drivers

Enterprise scale adoption of generative AI and applied analytics workloads

Vietnam’s AI infrastructure demand is accelerating because enterprises are moving beyond experimentation into production deployments that require reliable GPU capacity, low latency storage, and high throughput networks to support training, fine tuning, and inference at scale. Banks and fintechs are prioritizing fraud detection, credit decisioning, and conversational service automation, which increases round the clock inference demand and drives investment in resilient compute and failover designs. Manufacturers and logistics operators are expanding vision based quality inspection and predictive maintenance, pushing requirements for edge capable accelerators while still relying on centralized model training environments. Retail and digital commerce firms are deploying recommendation engines and content generation workflows that benefit from larger context windows and more frequent model refresh, raising compute intensity and storage I O needs. This shift favors integrated stacks that combine servers, accelerators, interconnect, and MLOps controls, encouraging larger deal sizes and platform standardization. Local leaders are reinforcing the trend by building AI factory style environments that package GPU infrastructure with software and services, lowering adoption barriers for mid market customers. The result is sustained pull through across compute, networking, and managed operations because organizations require predictable performance and governance rather than ad hoc infrastructure. This driver is further supported by visible large scale investments and partnerships that signal long term capacity commitments and shorten procurement cycles for enterprise buyers.

Data center and cloud capacity expansion aligned to AI ready requirements

Vietnam’s AI infrastructure market is also driven by the modernization of data center and cloud environments to handle higher rack densities, stricter power and cooling demands, and upgraded connectivity needed for accelerator clusters. AI workloads concentrate heat and power draw, so operators are investing in improved thermal management, power distribution upgrades, and facility engineering that can support dense GPU deployments without performance throttling. Cloud and telecom groups are leveraging their network reach to bundle connectivity with compute and storage, making it easier for enterprises to consume AI infrastructure as a service while meeting availability and security requirements. As new facilities and upgrades come online, infrastructure buyers gain access to larger contiguous GPU pools and better east west bandwidth, which improves model training efficiency and supports multi node scaling. Partnerships that include dedicated AI factories and expanded cloud capacity reinforce this build cycle, creating a feedback loop where more available capacity encourages broader adoption and larger workloads. Improved backbone connectivity between major hubs supports centralized training with distributed inference, which is important for applications in customer service, public services, and industrial monitoring. This driver also increases demand for professional services and managed operations, because AI ready environments require monitoring, cost control, and governance mechanisms that many enterprises lack internally. Overall, the combination of facility upgrades, cloud expansion, and bundled delivery models reduces time to deploy, expands addressable demand, and raises utilization of AI capable infrastructure across sectors.

Market Challenges

Constraint on advanced accelerator supply and deployment lead times

Vietnam’s AI infrastructure market faces a practical constraint because leading edge GPU and accelerator availability is volatile, and delivery schedules can be extended by global demand cycles, allocation policies, and supply chain bottlenecks. When procurement timelines slip, enterprise programs are forced to phase deployments, reduce model sizes, or rely on shared capacity, which can degrade performance and slow business value realization. This challenge is amplified for first time buyers that lack long term vendor relationships or cannot commit to large volume purchases, making it harder to secure priority allocations. Even when hardware arrives, integration is nontrivial because accelerator clusters require validated reference designs, specialized networking, and careful configuration of drivers and frameworks to achieve expected throughput. Data center readiness can become a gating factor, as dense GPU racks may exceed existing power and cooling envelopes, requiring retrofits that add cost and time. Skills gaps in cluster operations and MLOps further increase risk of underutilization, because organizations may struggle to schedule jobs, manage contention, and optimize inference efficiency. The combined effect is that some buyers delay purchases or adopt smaller initial footprints, which can slow overall market ramp even as demand remains strong. Over time, the market will depend on better supply planning, standardized architectures, and deeper operational capability to reduce these frictions and maintain deployment momentum.

Data governance, security, and compliance readiness for AI scale operations

Another major challenge is the gap between rapid AI adoption and the maturity of data governance, cybersecurity controls, and compliance practices needed to safely operate AI infrastructure at scale. AI systems ingest and generate sensitive data, and without strong access controls, logging, and model governance, organizations can face data leakage risks, misuse of proprietary information, or exposure through poorly secured pipelines. Many enterprises operate mixed environments across on premises, colocation, and cloud, which increases complexity in applying consistent security policies, identity controls, and encryption standards across data flows. The challenge extends to operational monitoring, because AI infrastructure requires visibility into utilization, model behavior, and incident response across compute, storage, and application layers. Public sector and regulated industries may need stronger assurance around data residency and auditability, which can slow procurement and require additional architecture work such as segmentation, sovereign controls, and dedicated environments. Limited specialist capacity in security engineering and AI governance can delay implementation of robust controls, increasing reliance on vendors and managed services that may not perfectly match internal risk expectations. As a result, some projects proceed cautiously with restricted scopes, while others incur higher costs to meet governance requirements, creating uneven adoption across sectors. Addressing this challenge requires coordinated investments in security frameworks, operational processes, and talent, alongside clearer compliance pathways for enterprise AI infrastructure programs.

Opportunities

AI factory and managed GPU platforms for mid market and sector specific adoption

A key opportunity in Vietnam’s AI infrastructure market is the expansion of AI factory style offerings that package GPU compute, storage, software stacks, and operational management into repeatable services tailored to industry needs. Many organizations want AI capabilities but cannot justify building private clusters, so managed GPU platforms with clear service tiers can unlock demand across banking, retail, healthcare, manufacturing, and digital services. Providers that offer standardized environments with pre validated frameworks, MLOps tooling, and secure tenant isolation can shorten onboarding time and improve utilization outcomes for customers that lack deep infrastructure teams. Sector specific bundles, such as vision inference platforms for manufacturing or compliant conversational AI environments for financial services, can further reduce adoption friction and increase willingness to commit to longer term consumption. This opportunity also supports ecosystem development, because local ISVs and system integrators can build solutions on top of managed platforms rather than replicating infrastructure work for each client. As AI factories are announced and capacity grows, providers can differentiate through governance features, cost transparency, and performance SLAs that address buyer concerns about reliability and risk. The commercial upside is stronger recurring revenue streams and higher customer stickiness, while the market benefit is broader diffusion of AI capabilities beyond large enterprises.

Domestic capacity building through talent development and international partnerships

Another opportunity is to pair infrastructure expansion with aggressive talent and capability building, leveraging partnerships between Vietnamese technology leaders and global AI hardware and platform firms to accelerate skills transfer and ecosystem maturity. As major investments in AI facilities and platforms progress, structured programs in accelerator operations, distributed training, data engineering, and MLOps can reduce the execution gap that often limits infrastructure ROI. This opportunity is particularly strong in the main hubs where universities, innovation centers, and large employers can coordinate curricula, apprenticeships, and certification pathways aligned to real world deployments. International collaborations can also catalyze best practice adoption in governance, security, and reference architectures, enabling faster scaling with fewer integration failures. For infrastructure providers, deeper local capability reduces support burdens and improves customer outcomes, which in turn supports higher utilization and expansion of consumption commitments. For enterprises, stronger domestic talent availability lowers dependency on scarce external specialists and enables more sustained innovation cycles, including model refinement and application development. As a result, Vietnam can strengthen its position as an AI delivery and deployment hub by ensuring that infrastructure growth is matched by operational excellence and solution building capacity, creating a reinforcing loop between demand, capability, and further investment.

Future Outlook

Over the next five years, Vietnam AI Infrastructure market momentum is expected to strengthen as more enterprises operationalize AI in core processes and scale compute intensive applications. Technology development will center on higher density GPU clusters, faster interconnects, and broader adoption of managed AI platforms that reduce integration effort. Regulatory support and public sector digital initiatives are likely to reinforce investment in secure and auditable AI environments. Demand side growth will be driven by banking, manufacturing, retail, and digital services seeking lower latency inference and faster model iteration. Competitive intensity will increase as local providers expand capacity and global vendors deepen partnerships tied to AI factory buildouts.

Major Players

- FPT Corporation

- Viettel Group

- VNPT

- NVIDIA

- IBM

- CMC Corporation

- VNG Corporation

- Samsung Electronics Vietnam

- Microsoft Vietnam

- Dell Technologies Vietnam

- HP Vietnam

- NEC Vietnam

- TMA Solutions

- Viettel AI

- Toshiba Vietnam

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Telecom operators and cloud providers

- Data center developers and colocation operators

- AI platform and software vendors

- Semiconductor and hardware OEMs

- Banking and financial services institutions

- Manufacturing and industrial automation firms

Research Methodology

Step 1: Identification of Key Variables

Define the AI infrastructure scope across compute, storage, networking, facilities, and managed services. Map demand drivers by end user industries and deployment models across major hubs.

Set inclusion criteria for vendors, platforms, and workloads to ensure comparability.

Step 2: Market Analysis and Construction

Compile secondary information on AI investments, facility expansions, and platform launches in the country. Normalize revenue and spend references into consistent USD terms for the defined scope. Construct segment level structure for product type and platform type based on purchasing behavior.

Step 3: Hypothesis Validation and Expert Consultation

Validate infrastructure adoption patterns through interviews with operators, integrators, and enterprise buyers.Cross check assumptions on dominant segments, deployment constraints, and procurement routes. Reconcile conflicting inputs using triangulation across multiple stakeholder perspectives.

Step 4: Research Synthesis and Final Output

Integrate findings into a coherent market narrative and segmentation framework for the defined period. Apply quality checks for internal consistency across market size, segmentation, and company mapping. Finalize outputs with clear assumptions, source alignment, and decision ready structure.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid AI and cloud adoption across enterprises and government sectors

National digital transformation and AI strategy incentives

Hyperscale and GPU-intensive data center investments

Expansion of submarine cable and connectivity infrastructure

Rising foreign investment openness in digital infrastructure - Market Challenges

Power availability and sustainable energy constraints for AI facilities

High capital intensity of hyperscale AI infrastructure deployment

Regulatory complexity in land, telecom, and data localization

Limited domestic advanced semiconductor and GPU ecosystem

Talent shortages in AI infrastructure engineering and operations - Market Opportunities

Green AI data centers linked to renewable energy programs

Regional AI training and compute hubs for Southeast Asia

Edge AI infrastructure for smart manufacturing and cities - Trends

Shift toward hyperscale and GPU-dense data centers

Integration of liquid cooling for AI compute density

Growth of AI-ready colocation facilities

Public-private partnerships in digital infrastructure

Localization of AI compute capacity - Government Regulations & Defense Policy

AI and digital infrastructure prioritized as strategic technologies

Telecommunications and investment laws enabling foreign ownership

Renewable power mechanisms for data centers - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value 2020-2025

- By Installed Units 2020-2025

- By Average System Price 2020-2025

- By System Complexity Tier 2020-2025

- By System Type (In Value%)

AI Data Center Infrastructure

High Performance Computing Clusters

AI Cloud Infrastructure Platforms

Edge AI Infrastructure Systems

AI Networking & Interconnect Systems - By Platform Type (In Value%)

Hyperscale Data Center Platforms

Enterprise AI Infrastructure Platforms

Telecom AI Infrastructure Platforms

Government & Public Sector Platforms

Colocation AI Platforms - By Fitment Type (In Value%)

On-Premise AI Infrastructure

Cloud-Hosted AI Infrastructure

Hybrid AI Infrastructure

Modular AI Infrastructure

Integrated AI Infrastructure - By EndUser Segment (In Value%)

Telecom & Digital Service Providers

BFSI & Fintech Institutions

Government & Smart City Programs

Manufacturing & Industry 4.0 Firms

Technology & AI Solution Providers - By Procurement Channel (In Value%)

Direct Enterprise Procurement

Government Tenders & PPP Programs

Telecom Infrastructure Contracts

Cloud & Colocation Service Agreements

System Integrator Partnerships - By Material / Technology (in Value%)

GPU-Accelerated Computing Systems

AI-Optimized Storage Infrastructure

High-Speed Optical Networking

Liquid Cooling & Thermal Systems

AI Data Center Power Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Viettel IDC

VNPT

FPT Smart Cloud

CMC Telecom

VNG Cloud

Nvidia

Intel

Supermicro

Dell Technologies

Hewlett Packard Enterprise

Huawei

ST Telemedia Global Data Centres

Keppel Data Centres

Amazon Web Services

Google Cloud

- Telecom operators driving hyperscale AI infrastructure capacity

- Government AI and smart city programs expanding demand

- Manufacturers adopting edge AI for Industry automation

- Cloud and tech firms localizing AI compute infrastructure

- Forecast Market Value 2026-2035

- Forecast Installed Units 2026-2035

- Price Forecast by System Tier 2026-2035

- Future Demand by Platform 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now