Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Vietnam’s AI servers and GPU hardware market reached approximately USD ~ million based on a recent historical assessment, driven by hyperscale cloud expansion, telecom AI infrastructure investment, and enterprise adoption of accelerated computing for analytics and automation. Global technology vendors increased GPU server shipments to regional data centers supporting AI training and inference workloads. Government digital economy initiatives and domestic cloud providers also accelerated procurement of high-performance compute infrastructure to support AI applications across finance, manufacturing, and public sector domains.

Ho Chi Minh City and Hanoi dominate deployment due to concentration of hyperscale and colocation data centers, strong enterprise digitalization, and proximity to telecom backbone infrastructure. Northern industrial clusters including Bac Ninh and Hai Phong attract AI compute installations supporting electronics and semiconductor manufacturing analytics. Emerging digital hubs such as Da Nang gain relevance through data center development and smart city programs. These regions benefit from reliable power, connectivity, and proximity to enterprise demand centers requiring high-performance AI processing infrastructure.

Market Segmentation

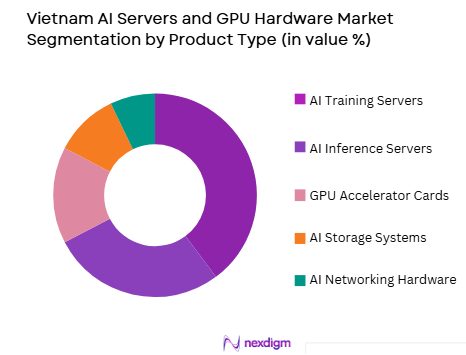

By Product Type

Vietnam AI Servers and GPU Hardware market is segmented by product type into AI training servers, AI inference servers, GPU accelerator cards, AI storage systems, and AI networking hardware. Recently, AI training servers has a dominant market share due to factors such as hyperscale cloud investment, demand for large-scale model development, and enterprise AI adoption across industries. Training workloads require high-density GPU clusters and advanced interconnects deployed in centralized data centers, leading to larger hardware spending compared with inference nodes. Cloud providers and telecom operators procure multi-GPU servers to support domestic AI platforms and enterprise machine learning services. Manufacturing and financial firms also invest in training infrastructure to develop proprietary AI models. Global GPU vendors prioritize shipment of high-performance training systems to Southeast Asian markets experiencing rapid AI adoption. National AI strategies emphasizing domestic model development further reinforce procurement of training-oriented compute infrastructure across Vietnam’s digital economy.

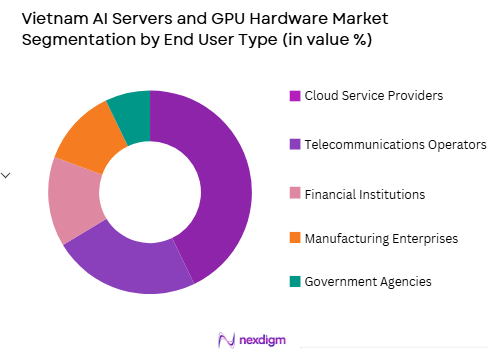

By End User

Vietnam AI Servers and GPU Hardware market is segmented by end user into cloud service providers, telecommunications operators, financial institutions, manufacturing enterprises, and government agencies. Recently, cloud service providers has a dominant market share due to factors such as hyperscale data center expansion, AI cloud service demand, and centralized GPU infrastructure economics. Domestic and regional cloud providers deploy large GPU clusters to offer AI training and inference as a service to enterprises lacking on-premise compute capability. AI application developers prefer cloud-based infrastructure for scalability and cost efficiency, concentrating demand within cloud operator facilities. Telecom companies and government agencies increasingly procure AI resources through cloud platforms rather than standalone deployments. Rapid growth of digital services, e-commerce, and fintech platforms in Vietnam further increases reliance on cloud-hosted AI compute. As enterprises shift toward managed AI infrastructure consumption, cloud providers continue to dominate procurement of GPU servers and accelerators.

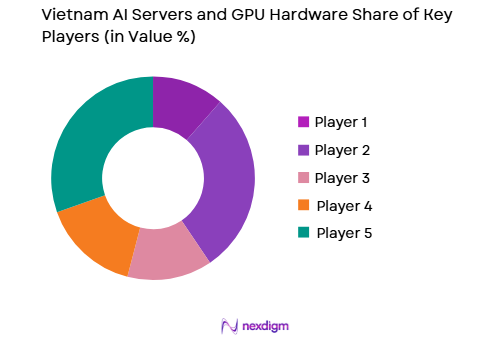

Competitive Landscape

Vietnam’s AI servers and GPU hardware market is shaped by global server manufacturers and GPU vendors collaborating with domestic telecom and cloud operators deploying hyperscale compute clusters. International firms dominate high-performance hardware supply, while local cloud providers control infrastructure deployment and service delivery. Strategic partnerships between global vendors and Vietnamese data center operators enable localized AI cloud capacity expansion. Competition centers on performance density, energy efficiency, and integrated AI software ecosystems supporting enterprise and public sector workloads.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | GPU Architecture Support |

| Viettel Group | 1989 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| FPT Corporation | 1988 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

| Lenovo | 1984 | China | ~ | ~ | ~ | ~ | ~ |

Vietnam AI Servers and GPU Hardware Market Analysis

Growth Drivers

Hyperscale Cloud and AI Platform Expansion

Vietnam’s rapid digital economy growth has accelerated hyperscale and regional cloud data center expansion, driving substantial procurement of AI servers and GPU hardware to support training and inference workloads across industries. Domestic cloud providers and telecom operators are investing in high-density GPU clusters to deliver AI-as-a-service platforms for enterprises developing machine learning models, analytics pipelines, and generative AI applications. Enterprises increasingly prefer cloud-hosted AI infrastructure due to scalability and reduced capital expenditure, concentrating hardware demand within centralized data centers operated by cloud companies. Government digital transformation strategies emphasize domestic AI capability and data sovereignty, encouraging cloud providers to deploy local AI compute capacity rather than relying on offshore infrastructure. Global GPU vendors collaborate with Vietnamese cloud operators to establish localized AI zones offering advanced compute services. Growth of e-commerce, fintech, and digital media platforms increases AI processing requirements, further stimulating GPU server procurement. Hyperscale cloud expansion also supports public sector AI initiatives including smart governance and digital public services. These structural shifts position cloud-centric AI infrastructure investment as a primary driver of Vietnam’s accelerated computing market growth.

Enterprise AI Adoption Across Manufacturing and Finance

Vietnam’s manufacturing and financial sectors are rapidly adopting artificial intelligence to enhance productivity, risk analytics, automation, and decision-making, leading to increased deployment of GPU-accelerated servers within enterprise data centers and private cloud environments. Manufacturers deploy AI training systems for machine vision, predictive maintenance, and process optimization models that require high-performance GPU clusters. Financial institutions utilize GPU servers for fraud detection, algorithmic trading analytics, credit scoring models, and customer behavior prediction platforms demanding large-scale parallel computation. Enterprises increasingly seek localized AI compute infrastructure to maintain data sovereignty and ensure low-latency processing of sensitive operational data. Domestic technology integrators and system vendors support enterprises in deploying on-premise or hybrid GPU infrastructure aligned with regulatory and performance requirements. As AI adoption matures, enterprises expand compute capacity from pilot deployments to production-scale infrastructure, significantly increasing GPU hardware procurement. Government incentives for Industry 4.0 and digital finance further accelerate enterprise AI investment. This broadening adoption across core economic sectors sustains long-term demand for AI servers and accelerators in Vietnam.

Market Challenges

Dependence on Imported GPU and Advanced Semiconductor Supply Chains

Vietnam’s AI servers and GPU hardware market relies heavily on imported GPUs, accelerators, and high-performance server components sourced from global semiconductor vendors, creating vulnerability to supply constraints, export controls, and geopolitical trade restrictions. Limited domestic semiconductor manufacturing capability prevents local production of advanced AI chips, forcing data center operators and enterprises to depend on foreign suppliers. Global shortages of high-end GPUs and export regulations affecting advanced computing hardware availability can delay infrastructure deployment timelines. Import tariffs, logistics costs, and currency fluctuations increase procurement expense for Vietnamese buyers relative to larger global markets. Domestic assembly and integration capabilities exist but do not mitigate dependence on core semiconductor components. Rapid evolution of GPU architectures also risks technology obsolescence for early deployments. These structural supply chain dependencies constrain scalability and cost competitiveness of Vietnam’s AI compute infrastructure market.

High Capital and Energy Intensity of AI Compute Infrastructure

AI servers and GPU clusters require significant capital investment and high power consumption, posing financial and operational challenges for Vietnamese data center operators and enterprises deploying accelerated computing infrastructure. High-density GPU servers consume substantial electricity and generate thermal loads requiring advanced cooling systems and reliable power distribution infrastructure. Energy costs and grid reliability constraints in certain regions increase operational expenditure and limit deployment scale. Data center operators must invest in redundant power, liquid cooling, and environmental controls to maintain performance and uptime. Enterprises evaluating on-premise GPU infrastructure face uncertain return on investment due to rapidly evolving AI workloads and hardware lifecycles. Limited domestic expertise in high-density AI infrastructure design and management further increases deployment complexity. These cost and infrastructure constraints slow broader adoption beyond major cloud and telecom operators.

Opportunities

Development of Sovereign AI Cloud and National Compute Infrastructure

Vietnam’s strategic emphasis on digital sovereignty and domestic AI capability creates opportunity for national AI cloud platforms and sovereign compute infrastructure initiatives requiring large-scale GPU server deployment. Government and telecom operators can establish centralized AI supercomputing facilities supporting public sector analytics, research, and domestic AI model development. Sovereign AI clouds enable sensitive data processing within national borders while reducing reliance on foreign compute providers. Public investment programs and digital economy strategies can fund deployment of national AI infrastructure accessible to enterprises and startups. Collaboration between global GPU vendors and domestic operators can accelerate local AI ecosystem development. Such sovereign compute initiatives would drive sustained demand for high-performance AI servers across Vietnam’s public and private sectors.

AI Infrastructure for Emerging Digital Services and Smart Economy Applications

Vietnam’s expanding digital services ecosystem including fintech, e-commerce, healthcare, and smart city platforms presents significant opportunity for AI server and GPU infrastructure deployment supporting advanced analytics and automation. Localized AI compute enables real-time recommendation engines, fraud detection, medical imaging analysis, and intelligent urban management applications requiring large-scale parallel processing. Startups and technology firms increasingly build AI-driven products that depend on accessible GPU infrastructure delivered through cloud or hybrid models. Telecom and cloud providers can monetize GPU clusters by offering industry-specific AI platforms and managed services. Growth of generative AI applications and digital content creation further increases demand for accelerated computing. As Vietnam’s smart economy evolves, AI infrastructure becomes foundational to digital service innovation, creating long-term market expansion opportunities.

Future Outlook

Vietnam’s AI servers and GPU hardware market is expected to expand rapidly as domestic AI adoption deepens across cloud, enterprise, and public sector domains. Hyperscale and sovereign AI infrastructure initiatives will increase national compute capacity. Enterprises will scale AI deployments from pilot to production workloads. Energy-efficient GPU architectures and liquid-cooled data centers will improve deployment economics. Regulatory support for digital sovereignty and AI innovation will further stimulate infrastructure investment across Vietnam’s digital economy.

Major Players

- Viettel Group

- FPT Corporation

- VNPT

- CMC Telecom

- VNG Corporation

- Viettel IDC

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Huawei Technologies

- Inspur

- Supermicro

- ASUS

- GIGABYTE

- Foxconn Industrial Internet

Key Target Audience

- Cloud service providers

- Telecommunications operators

- Data center operators

- Financial institutions

- Manufacturing enterprises

- Government and regulatory bodies

- Investments and venture capitalist firms

- AI platform developers

Research Methodology

Step 1: Identification of Key Variables

Key demand and supply variables including GPU shipments, data center capacity expansion, cloud infrastructure investment, and enterprise AI adoption intensity were identified. Hardware procurement volumes, vendor revenues, and deployment patterns across cloud, telecom, and enterprise sectors were mapped to estimate market structure.

Step 2: Market Analysis and Construction

Bottom-up modeling combined server shipments, GPU accelerator sales, and data center infrastructure investment to construct market size. Segmentation reflected product categories and end-user adoption patterns derived from infrastructure deployment and procurement data across Vietnam’s digital economy sectors.

Step 3: Hypothesis Validation and Expert Consultation

Industry consultations with cloud operators, telecom providers, and infrastructure vendors validated deployment trends, cost structures, and technology adoption drivers. Technical experts confirmed GPU architecture preferences, infrastructure requirements, and regulatory influences shaping Vietnam’s AI compute ecosystem.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights were synthesized into market estimates, segmentation, and competitive analysis. Cross-verification ensured consistency across infrastructure deployments, enterprise adoption, and vendor supply chains to produce final market intelligence outputs.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of hyperscale and colocation AI data center infrastructure

Enterprise AI adoption across finance manufacturing and digital platforms

National AI and digital transformation strategies driving compute investment - Market Challenges

Dependence on imported advanced GPU and AI processor supply chains

High capital and power density requirements of AI compute infrastructure

Limited domestic expertise in large scale AI cluster deployment - Market Opportunities

Vietnam emergence as regional AI compute and data center hub

Government funded national AI infrastructure and research programs

Growth of AI enabled smart city and digital economy applications - Trends

Deployment of GPU dense hyperscale AI clusters in urban corridors

Adoption of AI inference servers in enterprise data centers

Partnerships between cloud providers and telecom operators for AI platforms - Government regulations

National AI Strategy and Digital Transformation Program mandates

Data localization and cybersecurity compliance requirements

Technology import and high performance computing regulations - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

GPU Accelerated AI Servers

AI Training Supercomputing Clusters

AI Inference Servers

High Performance GPU Accelerator Cards

AI Edge GPU Systems - By Platform Type (In Value%)

Hyperscale Data Center AI Platforms

Enterprise Private AI Infrastructure

Telecom AI Network Optimization Platforms

Government and Research AI Compute Platforms

Cloud AI Infrastructure Services - By Fitment Type (In Value%)

On-Premise GPU Server Installations

Colocation Data Center Deployments

Hyperscale Cloud GPU Clusters

Integrated OEM AI Appliances

Modular AI Compute Racks - By End User Segment (In Value%)

Cloud and Data Center Providers

Telecommunications Operators

Financial Services and Banking Institutions

Manufacturing and Industrial Enterprises

Government and Academic Research Bodies - By Procurement Channel (In Value%)

Direct OEM Hardware Procurement

Cloud Service Provider Contracts

System Integrator AI Deployments

Telecom Infrastructure Procurement

Government Technology Tenders

- Market Share Analysis

- Cross Comparison Parameters (Compute Performance Density, GPU Architecture Support, Data Center Integration Capability, AI Software Ecosystem Compatibility, Regional Deployment Presence, Cooling and Power Efficiency, AI Workload Optimization Capability, Local Integration and Support Strength, Hyperscale Partnership Depth, Supply Chain Reliability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA Vietnam

AMD Vietnam

Intel Vietnam

Dell Technologies Vietnam

Hewlett Packard Enterprise Vietnam

Lenovo Vietnam

Supermicro Vietnam

Inspur Vietnam

Huawei Vietnam

FPT Smart Cloud

Viettel IDC

VNPT Technology

CMC Telecom

AWS Vietnam

Microsoft Vietnam

- Cloud providers lead procurement of GPU servers for regional AI workloads

- Telecom operators deploy AI infrastructure for network optimization and services

- Financial and manufacturing enterprises adopt AI compute for analytics automation

- Government and research institutions invest in national AI computing capacity

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now