Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Vietnam’s cloud infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by enterprise digital transformation, hyperscale cloud localization, and expansion of domestic data center capacity. Global and regional cloud providers increased investment in compute, storage, and networking infrastructure to support e-commerce, fintech, and digital public services platforms. Government data localization regulations and national digital economy programs further accelerated deployment of in-country cloud infrastructure and hyperscale-ready data center facilities serving enterprise and public sector workloads.

Ho Chi Minh City and Hanoi dominate cloud infrastructure deployment due to concentration of data centers, telecom backbone connectivity, and enterprise IT demand across finance, retail, and technology sectors. Southern industrial regions including Binh Duong and Dong Nai host colocation and hyperscale facilities supporting manufacturing and logistics enterprises. Northern technology clusters around Bac Ninh and Hai Phong benefit from proximity to electronics manufacturing ecosystems and international connectivity. These regions provide power reliability and fiber density essential for large-scale cloud infrastructure operations.

Market Segmentation

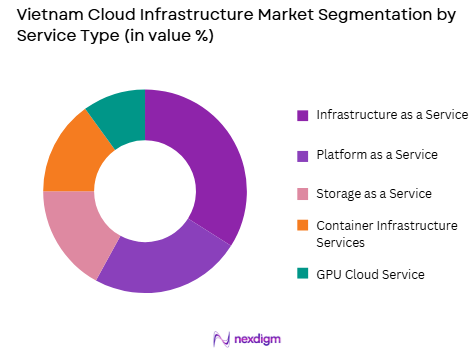

By Service Type

Vietnam Cloud Infrastructure market is segmented by service type into infrastructure as a service, platform as a service, storage as a service, container infrastructure services, and GPU cloud services. Recently, infrastructure as a service has a dominant market share due to factors such as enterprise migration of core workloads, demand for scalable compute resources, and rapid cloud adoption across digital businesses. Enterprises transitioning from on-premise IT environments prioritize virtualized compute and networking resources delivered through IaaS platforms. Cloud providers expand regional data centers to supply elastic compute capacity for e-commerce, fintech, and software platforms. Government and telecom organizations also deploy private and hybrid cloud environments built on IaaS foundations. As foundational compute infrastructure underpins higher-level cloud services, infrastructure as a service remains the largest revenue component across Vietnam’s cloud ecosystem.

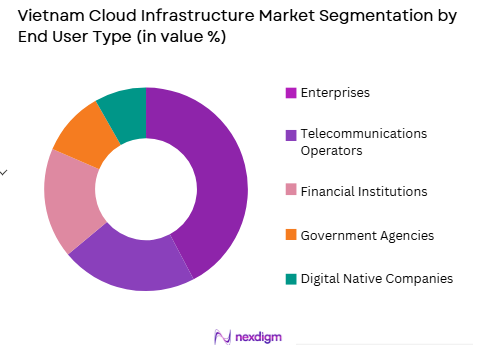

By End User

Vietnam Cloud Infrastructure market is segmented by end user into enterprises, telecommunications operators, financial institutions, government agencies, and digital native companies. Recently, enterprises has a dominant market share due to factors such as large-scale IT modernization, cloud migration of enterprise applications, and demand for scalable infrastructure across manufacturing, retail, and services sectors. Enterprises increasingly adopt hybrid and public cloud environments to reduce capital expenditure and improve operational agility. Manufacturing firms migrate ERP and analytics workloads to cloud platforms, while retail and logistics companies deploy digital platforms requiring elastic infrastructure. Domestic cloud providers offer enterprise-focused hosting and managed infrastructure services accelerating adoption. As enterprise digital transformation expands nationwide, enterprises remain the largest consumers of cloud infrastructure capacity in Vietnam.

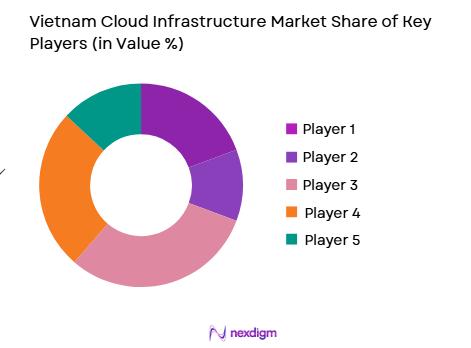

Competitive Landscape

Vietnam’s cloud infrastructure market is characterized by partnerships between global hyperscale cloud providers and domestic telecom and data center operators deploying localized infrastructure capacity. International firms supply cloud platforms and software ecosystems, while Vietnamese operators provide in-country data center and network infrastructure to meet regulatory requirements. Competition centers on data center footprint, service breadth, and compliance with data localization policies across enterprise and public sector markets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Data Center Presence |

| Viettel Group | 1989 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| FPT Corporation | 1988 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| VNPT | 1995 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

Vietnam Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Cloud Migration

Vietnam’s enterprises across manufacturing, retail, finance, and services sectors are accelerating digital transformation initiatives that require scalable computing, storage, and networking infrastructure delivered through cloud platforms rather than traditional on-premise IT environments. Organizations are migrating enterprise resource planning, analytics, customer engagement, and supply chain systems to cloud infrastructure to improve agility, reduce capital expenditure, and enable real-time data processing across distributed operations. Rapid growth of e-commerce and digital services platforms also compels enterprises to deploy elastic infrastructure capable of handling variable demand and transaction volumes. Domestic cloud providers and telecom operators offer managed cloud environments tailored to Vietnamese regulatory and language requirements, lowering adoption barriers. Hybrid cloud architectures allow enterprises to maintain sensitive workloads locally while leveraging public cloud scalability. As enterprises modernize legacy systems and adopt digital business models, demand for infrastructure-as-a-service and related cloud capacity continues to expand across Vietnam’s economy.

Hyperscale Data Center Localization and Regulatory Data Sovereignty

Vietnam’s regulatory framework emphasizing data localization and digital sovereignty has driven global and domestic cloud providers to deploy in-country data center infrastructure and localized cloud regions serving enterprise and government workloads. Regulations requiring storage and processing of certain data categories within national borders encourage hyperscale providers to partner with local telecom and data center operators to establish compliant infrastructure. Telecom companies expand carrier-neutral colocation and hyperscale-ready facilities to host cloud platforms. Government digital transformation programs also mandate domestic hosting for public sector systems, increasing demand for sovereign cloud environments. Localization improves latency and service performance for Vietnamese users while ensuring regulatory compliance. As data sovereignty requirements strengthen, investment in localized hyperscale cloud infrastructure remains a major structural driver of Vietnam’s cloud infrastructure market.

Market Challenges

Data Center Power and Infrastructure Constraints

Expansion of cloud infrastructure in Vietnam faces challenges associated with power availability, grid reliability, and cooling efficiency required for hyperscale data center operations. High-density compute environments consume substantial electricity and require stable power supply and advanced cooling systems to maintain uptime. Industrial zones and urban areas may face capacity constraints or energy cost variability affecting large-scale data center deployment. Operators must invest in redundant power systems, backup generation, and efficient cooling technologies to ensure service continuity. Infrastructure readiness varies across regions, limiting geographic diversification of cloud facilities. Environmental and land-use regulations also influence site selection and construction timelines. These infrastructure constraints affect scalability and operational cost of Vietnam’s cloud infrastructure expansion.

Dependence on Foreign Cloud Platforms and Technology Ecosystems

Vietnam’s cloud infrastructure market relies heavily on global hyperscale providers and foreign technology ecosystems for advanced cloud platforms, orchestration software, and hardware architecture, creating dependence risks and limiting domestic technological sovereignty. Domestic providers often partner with or license technology from international vendors to deliver competitive cloud services. Limited indigenous development of hyperscale cloud software stacks constrains differentiation and innovation. Enterprises may prefer established global cloud platforms for reliability and ecosystem breadth, intensifying dependence on foreign providers. Technology transfer and local ecosystem development remain gradual. These structural dependencies challenge long-term competitiveness of domestic cloud infrastructure providers.

Opportunities

Sovereign and Government Cloud Infrastructure Development

Vietnam’s emphasis on digital sovereignty and secure public sector digitalization creates opportunity for sovereign cloud platforms and government-dedicated cloud infrastructure requiring localized data center and compute capacity. Public sector agencies increasingly migrate services and data to controlled cloud environments hosted within national jurisdiction. Domestic telecom and technology firms can develop government-compliant cloud platforms tailored to regulatory, security, and language requirements. National cloud initiatives reduce dependence on foreign providers while strengthening domestic infrastructure capability. Expansion of e-government and digital public services further drives sovereign cloud adoption across ministries and state enterprises. These initiatives create sustained demand for domestic cloud infrastructure deployment.

Cloud Infrastructure for AI, Fintech, and Digital Economy Platforms

Vietnam’s rapidly expanding digital economy including AI development, fintech services, e-commerce platforms, and digital media applications generates opportunity for scalable cloud infrastructure supporting compute-intensive and data-driven workloads. AI training and analytics platforms require high-performance cloud infrastructure integrated with GPU resources. Fintech platforms require secure, scalable environments for transaction processing and risk analytics. Digital commerce and content platforms depend on elastic infrastructure to support user growth. Cloud providers can deliver specialized platforms for these verticals, increasing infrastructure utilization. As Vietnam’s digital economy matures, demand for advanced cloud infrastructure services continues to expand.

Future Outlook

Vietnam’s cloud infrastructure market is expected to expand rapidly as enterprise cloud adoption deepens and hyperscale localization investments increase. Data sovereignty policies will continue to drive domestic infrastructure deployment. Growth of AI, fintech, and digital commerce platforms will increase demand for scalable cloud capacity. Expansion of regional data center hubs will improve geographic coverage. Domestic and global provider partnerships will strengthen ecosystem maturity and sustain long-term market growth.

Major Players

- Viettel IDC

- FPT Corporation

- VNPT

- CMC Telecom

- VNG Cloud

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Alibaba Cloud

- ST Telemedia Global Data Centres

- NTT Global Data Centers

- Equinix

- Digital Realty

- Huawei Cloud

- True IDC

Key Target Audience

- Enterprises

- Telecommunications operators

- Financial institutions

- Government and regulatory bodies

- Digital platform companies

- Data center operators

- Investments and venture capitalist firms

- Cloud service integrators

Research Methodology

Step 1: Identification of Key Variables

Key variables including data center capacity, cloud adoption rates, enterprise IT spending, and hyperscale investment were identified. Infrastructure deployment patterns and service demand across industries were mapped to quantify cloud infrastructure requirements in Vietnam.

Step 2: Market Analysis and Construction

Bottom-up modeling combined data center capacity, cloud service revenues, and enterprise migration trends to estimate market size. Segmentation reflected service types and end-user adoption patterns across Vietnam’s digital economy sectors.

Step 3: Hypothesis Validation and Expert Consultation

Industry consultations with cloud providers, telecom operators, and data center developers validated deployment trends, cost structures, and regulatory influences. Technical experts confirmed infrastructure requirements and adoption drivers shaping Vietnam’s cloud ecosystem.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights were synthesized into market estimates, segmentation, and competitive analysis. Cross-verification ensured consistency across infrastructure capacity, service demand, and vendor supply chains to produce final outputs.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid enterprise digital transformation and cloud adoption

Expansion of hyperscale and colocation data center capacity

Government digital economy and e-government initiatives - Market Challenges

Data localization and cybersecurity compliance complexity

Limited domestic hyperscale infrastructure ownership

Shortage of advanced cloud engineering expertise - Market Opportunities

Development of sovereign and national cloud platforms

Expansion of regional cloud data center hubs in Hanoi and Ho Chi Minh City

Growth of AI and analytics workloads on cloud platforms - Trends

Hybrid and multi-cloud adoption across enterprises

Partnerships between global hyper scalers and local telecom operators

Deployment of modular and edge-enabled cloud infrastructure - Government regulations

Data localization and cybersecurity law requirements

National Digital Transformation Program mandates

Cloud service licensing and data governance policies - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Cloud Data Center Infrastructure

Hyperscale Cloud Platforms

Private Cloud Infrastructure

Hybrid Cloud Systems

Edge Cloud Infrastructure - By Platform Type (In Value%)

Public Cloud Infrastructure

Enterprise Private Cloud Platforms

Government Cloud Platforms

Telecom Cloud Infrastructure

Industry-Specific Cloud Platforms - By Fitment Type (In Value%)

Greenfield Cloud Data Centers

Colocation Cloud Facilities

On-Premise Cloud Installations

Modular Cloud Infrastructure

Integrated Hyperscale Campuses - By End User Segment (In Value%)

Digital Enterprises and Platforms

Telecommunications Operators

Government and Public Sector

Financial Services Institutions

Manufacturing and Industrial Firms - By Procurement Channel (In Value%)

Direct Cloud Provider Contracts

System Integrator Cloud Deployments

Telecom Managed Cloud Services

Colocation and Hosting Agreements

Government Cloud Procurement Programs

- Market Share Analysis

- Cross Comparison Parameters (Data Center Scale, Cloud Service Portfolio Depth, Hybrid and Multi Cloud Capability, AI and Analytics Infrastructure Support, Regional Infrastructure Presence, Network Connectivity and Latency Optimization, Enterprise Integration Strength, Security and Compliance Capability, Sovereign Cloud Support, Managed Services Maturity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Viettel IDC

VNPT Cloud

FPT Smart Cloud

CMC Telecom

VNG Cloud

AWS Vietnam

Microsoft Vietnam

Google Cloud Vietnam

Alibaba Cloud Vietnam

Huawei Cloud Vietnam

ST Telemedia Global Data Centres Vietnam

NTT Global Data Centers Vietnam

Equinix Vietnam

GDS Vietnam

Keppel Data Centres Vietnam

- Digital enterprises lead cloud adoption for platforms and services

- Telecom operators expand cloud infrastructure and services

- Government agencies deploy national and sovereign cloud platforms

- Financial and industrial firms adopt cloud for analytics and operations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now