Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Vietnam Cold Chain Logistics market generated approximately USD ~ billion in revenue, supported by expanding demand for temperature-controlled storage and transportation across pharmaceutical distribution, seafood exports, and processed food supply chains. According to data published by the General Statistics Office of Vietnam and the Vietnam Association of Seafood Exporters and Producers, seafood exports alone exceeded USD ~ billion in value, requiring extensive refrigerated logistics infrastructure. Rapid growth in modern retail chains, pharmaceutical imports valued above USD ~ billion, and expanding frozen food consumption continue strengthening demand for cold warehouses, refrigerated trucking fleets, and integrated cold logistics networks.

Major cold chain logistics activity is concentrated in Ho Chi Minh City, Hanoi, Hai Phong, and Da Nang, where industrial zones, international seaports, and large consumer markets create strong demand for refrigerated distribution networks. Ho Chi Minh City serves as the primary logistics hub for seafood exports and food processing industries connected to Mekong Delta aquaculture production. Hanoi supports pharmaceutical imports and national food distribution networks. Hai Phong and Da Nang dominate refrigerated cargo handling due to their strategic port infrastructure, export-oriented manufacturing clusters, and expanding cold storage facilities supporting regional seafood processing and agricultural supply chains.

Market Segmentation

By Service Type

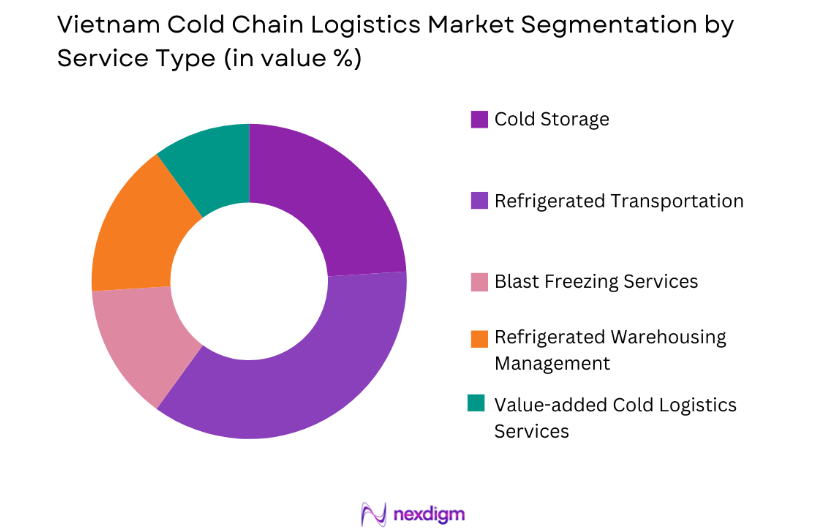

Vietnam Cold Chain Logistics market is segmented by service type into cold storage, refrigerated transportation, blast freezing services, refrigerated warehousing management, and value-added cold logistics services. Recently, refrigerated transportation has a dominant market share due to increasing demand for temperature-controlled cargo distribution across food retail supply chains and export logistics operations. Expanding seafood exports, pharmaceutical imports, and frozen food distribution require reliable refrigerated trucking fleets capable of maintaining strict temperature control during long-distance transportation. Logistics companies continue expanding refrigerated vehicle fleets connecting aquaculture farms, food processing plants, ports, and urban retail distribution centers across Vietnam.

By End Use Industry

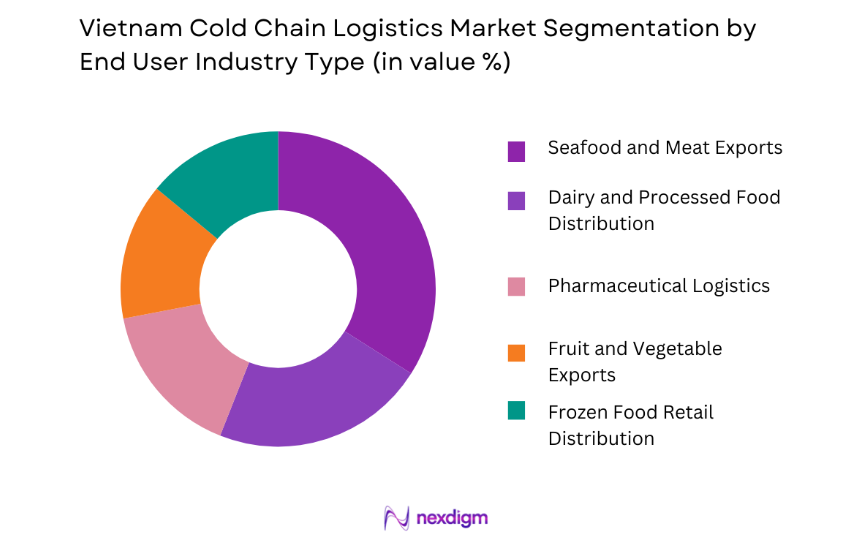

Vietnam Cold Chain Logistics market is segmented by end use industry into seafood and meat exports, dairy and processed food distribution, pharmaceutical logistics, fruit and vegetable exports, and frozen food retail distribution. Recently, seafood and meat exports have a dominant market share due to Vietnam’s globally competitive seafood production sector and strong export demand across international markets. Large volumes of shrimp, pangasius, tuna, and processed seafood require temperature-controlled storage and transport to maintain quality standards required by global food safety regulations. Export-oriented seafood processors depend heavily on cold warehouses located near coastal processing zones and port terminals.

Competitive Landscape

The Vietnam Cold Chain Logistics market remains moderately fragmented with a combination of international logistics providers and domestic cold storage operators competing for industrial clients across food exports and pharmaceutical distribution networks. Major global companies have expanded investment in automated cold warehouses and integrated supply chain services, while domestic operators focus on regional cold storage facilities near seafood processing zones. Strategic partnerships with food exporters, retail chains, and pharmaceutical distributors have become a major competitive factor, enabling logistics companies to secure long-term temperature-controlled logistics contracts.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Storage Capacity |

| Lineage Logistics | 2012 | United States | ~ | ~ | ~ | ~ | ~ |

| Americold Logistics | 1903 | United States | ~ | ~ | ~ | ~ | ~ |

| CJ Logistics | 1930 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Nichirei Logistics Group | 1945 | Japan | ~ | ~ | ~ | ~ | ~ |

| Swire Cold Storage | 1980 | Australia | ~ | ~ | ~ | ~ | ~ |

Vietnam Cold Chain Logistics Market Analysis

Growth Drivers

Rapid Expansion of Seafood Export Supply Chains and Global Food Trade

Rapid expansion of seafood export supply chains significantly strengthens demand for cold chain logistics infrastructure across Vietnam’s food export economy. Vietnam is among the world’s largest exporters of shrimp, pangasius, and tuna, generating billions of dollars in annual export value that requires temperature controlled logistics networks capable of preserving product quality during storage and international transportation. Processing facilities located throughout the Mekong Delta depend on refrigerated logistics providers to move seafood products from aquaculture farms to export processing plants, cold warehouses, and international ports. Maintaining strict temperature control throughout the logistics chain is essential for complying with international food safety standards required by markets such as the United States, Japan, and the European Union. Logistics providers therefore invest heavily in cold storage warehouses, blast freezing facilities, and refrigerated trucking fleets capable of handling high cargo volumes generated by seafood processing clusters. Export logistics operations also require advanced monitoring systems that track temperature levels throughout transportation routes to prevent spoilage and ensure regulatory compliance. International buyers increasingly demand traceable cold supply chains that guarantee product freshness and quality upon arrival at overseas markets. As Vietnam continues expanding its seafood production capacity and strengthening export relationships with global food markets, demand for reliable cold chain logistics infrastructure continues increasing across storage, transportation, and distribution networks supporting the seafood export industry.

Growth of Modern Retail Chains and Frozen Food Consumption

Growth of modern retail chains and frozen food consumption significantly accelerates development of cold chain logistics infrastructure across Vietnam’s domestic food distribution system. Rapid urbanization and rising household incomes have increased demand for packaged frozen foods, dairy products, processed meat, and ready to cook meals distributed through supermarkets, convenience stores, and online grocery platforms. Retail chains require reliable refrigerated storage facilities and transportation networks capable of maintaining consistent product temperatures from food processing plants to retail shelves. Expanding supermarket chains including Co.opmart, VinMart, and Big C depend on integrated cold distribution systems connecting central distribution warehouses with urban retail outlets. Logistics providers therefore expand refrigerated trucking fleets and automated cold warehouses designed to support large scale retail food distribution networks. Maintaining consistent temperature control is essential for preserving product quality, preventing food spoilage, and complying with national food safety regulations. Digital supply chain monitoring systems allow retailers and logistics providers to track inventory movement and temperature levels throughout transportation and storage operations. Growing consumer preference for frozen seafood, packaged ready meals, and chilled beverages continues increasing demand for refrigerated logistics services. As Vietnam’s modern retail sector expands further across major cities and secondary urban centers, cold chain logistics infrastructure becomes increasingly critical for supporting nationwide food distribution networks.

Market Challenges

High Capital Investment Requirements for Cold Storage Infrastructure Development

High capital investment requirements present a major challenge limiting the rapid expansion of cold chain logistics infrastructure across Vietnam’s food and pharmaceutical supply chains. Construction of modern refrigerated warehouses requires specialized insulation systems, temperature monitoring technologies, energy efficient refrigeration equipment, and backup power infrastructure designed to maintain stable cold environments. These facilities involve significantly higher development costs compared to conventional warehousing infrastructure, creating financial barriers for smaller logistics operators attempting to expand cold storage capacity. Maintaining reliable electricity supply is also essential for operating refrigeration equipment continuously, which increases operational costs and infrastructure complexity. Refrigerated trucking fleets require specialized vehicles equipped with cooling units capable of maintaining precise temperature ranges during long distance transportation routes connecting farms, food processing plants, and urban distribution centers. Many domestic logistics companies face difficulties securing financing required to invest in large scale refrigerated infrastructure expansion. Limited access to advanced refrigeration technologies and skilled technicians capable of maintaining complex cooling systems also restricts operational efficiency within the sector. High energy consumption associated with refrigeration systems further increases operational costs for logistics providers. As demand for temperature controlled logistics services continues growing, the industry must address significant infrastructure investment challenges in order to expand cold storage capacity and support increasing shipment volumes.

Fragmented Cold Chain Infrastructure and Supply Chain Inefficiencies

Fragmented cold chain infrastructure remains a major operational challenge affecting efficiency and reliability within Vietnam’s temperature controlled logistics sector. Cold storage facilities and refrigerated transportation networks are unevenly distributed across the country, with most advanced infrastructure concentrated in major urban centers and export processing zones. Many agricultural production regions lack sufficient refrigerated storage capacity, forcing producers to transport perishable products over long distances without consistent temperature control. This infrastructure gap increases the risk of food spoilage and product quality degradation during transportation. Small scale logistics operators frequently rely on outdated refrigeration equipment that cannot maintain stable temperature levels required for pharmaceutical products and high value food exports. Lack of integration between cold storage facilities, transport operators, and distribution centers further complicates logistics coordination across the supply chain. Limited adoption of digital supply chain management platforms also reduces shipment visibility and temperature monitoring capabilities. These inefficiencies increase operational costs for exporters and retail distributors relying on refrigerated logistics networks. Government initiatives promoting logistics infrastructure modernization are gradually addressing these challenges, but the industry continues facing significant gaps in nationwide cold chain connectivity. Improving coordination between logistics providers, agricultural producers, and export processing companies remains essential for strengthening cold supply chain reliability.

Opportunities

Expansion of Pharmaceutical Cold Chain Logistics and Vaccine Distribution Networks

Expansion of pharmaceutical cold chain logistics presents a major opportunity for logistics providers operating within Vietnam’s temperature controlled supply chain industry. Pharmaceutical products including vaccines, biologics, and specialty medicines require strict temperature management throughout storage and transportation processes to maintain product efficacy and safety. Vietnam’s pharmaceutical import market continues expanding as healthcare infrastructure improves and access to advanced medicines increases across the country. Hospitals, pharmaceutical distributors, and biotechnology companies depend on specialized logistics providers capable of maintaining temperature ranges required for sensitive medical products. This creates strong demand for validated cold warehouses, refrigerated transport systems, and advanced temperature monitoring technologies designed specifically for pharmaceutical logistics. Regulatory authorities increasingly require strict compliance with Good Distribution Practice standards governing pharmaceutical storage and transportation operations. Logistics companies therefore invest in temperature controlled packaging systems, real time monitoring sensors, and certified cold storage facilities designed to handle sensitive medical cargo. International pharmaceutical manufacturers also rely on specialized cold chain logistics partners capable of distributing imported medicines across national healthcare supply networks. As pharmaceutical consumption and biotechnology development continue expanding, demand for high reliability pharmaceutical cold chain logistics services will create new growth opportunities for specialized logistics providers.

Development of Integrated Cold Logistics Hubs Supporting Agricultural Exports

Development of integrated cold logistics hubs supporting agricultural exports represents a significant opportunity for Vietnam’s cold chain logistics industry. Agricultural sectors including seafood, fruits, vegetables, and processed foods generate large export volumes requiring reliable refrigerated storage and transportation infrastructure connecting production areas with international ports. Establishing integrated cold logistics hubs near major agricultural production regions allows exporters to consolidate shipments, maintain product freshness, and streamline export logistics operations. These logistics hubs typically include cold storage warehouses, blast freezing facilities, packaging centers, and refrigerated cargo handling infrastructure designed to support high export volumes. Government initiatives promoting agricultural export competitiveness encourage investment in modern cold logistics infrastructure capable of meeting international food safety and quality standards. Logistics providers that develop integrated export logistics platforms can offer value added services including product grading, packaging, and export documentation management. Modern cold logistics hubs also improve supply chain efficiency by reducing transportation time between farms, processing facilities, and port terminals. As Vietnam continues strengthening its position as a major exporter of seafood and agricultural products, investment in integrated cold logistics infrastructure will create significant opportunities for logistics companies specializing in temperature controlled supply chain management.

Future Outlook

Vietnam’s cold chain logistics market is expected to experience sustained expansion driven by growth in seafood exports, pharmaceutical distribution, and modern retail food supply chains. Investments in automated cold warehouses, digital temperature monitoring systems, and refrigerated transport fleets are likely to improve logistics efficiency. Government infrastructure modernization initiatives and port development projects will strengthen export logistics capabilities. Increasing consumer demand for frozen food products and pharmaceutical imports will continue supporting expansion of temperature-controlled logistics networks across the country.

Major Players

- Lineage Logistics

- Americold Logistics

- CJ Logistics

- Nichirei Logistics Group

- Swire Cold Storage

- DHL Supply Chain

- DB Schenker

- Kuehne + Nagel

- Maersk Logistics

- Kerry Logistics

- Yusen Logistics

- OOCL Logistics

- Panalpina Logistics

- Cold Chain Connect Vietnam

- ABA Cooltrans

Key Target Audience

- Pharmaceutical manufacturers

- Food and beverage manufacturers

- Seafood export companies

- Cold chain logistics providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Retail supermarket chains

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the Vietnam Cold Chain Logistics market were identified through analysis of logistics infrastructure, food export volumes, pharmaceutical distribution networks, and refrigerated transportation capacity. Market drivers such as seafood exports, modern retail growth, and pharmaceutical imports were assessed to determine demand for cold logistics services.

Step 2: Market Analysis and Construction

The market structure was developed by examining cold storage capacity, refrigerated transport infrastructure, and supply chain integration across Vietnam’s food export and pharmaceutical industries. Data from government trade statistics, logistics associations, and industry reports were used to construct the market framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses were validated through consultation with logistics operators, supply chain experts, and export industry stakeholders. Feedback from professionals involved in seafood processing, pharmaceutical distribution, and refrigerated logistics operations was incorporated to refine market assumptions.

Step 4: Research Synthesis and Final Output

All data points and analytical insights were synthesized to develop a comprehensive assessment of Vietnam’s cold chain logistics market. The final output integrates quantitative data, infrastructure analysis, and industry dynamics to provide a structured outlook for stakeholders and investors.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising Demand for Perishable Food and Pharmaceutical Distribution

Expansion of E-commerce Grocery and Online Food Retail

Investment in Temperature-Controlled Infrastructure and Technology - Market Challenges

High Capital Expenditure for Refrigerated Equipment and Warehouses

Fragmented Cold Chain Logistics Providers Across Regions

Regulatory Compliance for Food Safety and Pharmaceutical Transport - Market Opportunities

Adoption of IoT-Enabled Temperature Monitoring Solutions

Expansion of Last-Mile Refrigerated Delivery Services

Partnerships Between Logistics Providers and E-commerce Platforms - Trends

Use of Automated and Electric Refrigerated Vehicles

Integration of Real-Time Temperature Monitoring and Tracking Systems - Government Regulations

Food Safety Standards and Cold Chain Compliance

Pharmaceutical Transport Regulations

Government Incentives for Infrastructure Development - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Trucks and Delivery Vehicles

Cold Storage Warehouses

Temperature Monitoring and Tracking Systems

Refrigerated Containers and Pallets

Automated Handling and Packaging Equipment - By Platform Type (In Value%)

Land Transportation Platforms

Air Freight Platforms

Maritime Shipping Platforms

Integrated Multimodal Platforms - By Fitment Type (In Value%)

On-premise Cold Chain Solutions

Cloud-based Cold Chain Solutions

Hybrid Cold Chain Solutions

Modular Refrigeration Systems - By End User Segment (In Value%)

Pharmaceutical and Healthcare Companies

Food and Beverage Manufacturers

E-commerce Grocery and Retail Platforms

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Technology Integration, Automation Level, Geographic Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

CJ Logistics Vietnam

Lotte Global Logistics Vietnam

Hanjin Transportation Vietnam

Hyundai Glovis Vietnam

Dongwon Logistics Vietnam

Korea Cold Storage Vietnam

Hyosung Logistics Vietnam

CJ Freshway Logistics Vietnam

Orion Logistics Vietnam

LF Logistics Vietnam

Kerry Logistics Vietnam

Maersk Logistics Vietnam

DB Schenker Vietnam

DHL Supply Chain Vietnam

Kuehne + Nagel Vietnam

- Pharmaceutical Companies Increasing Demand for Temperature-Controlled Logistics

- Food and Beverage Manufacturers Expanding Refrigerated Distribution Networks

- E-commerce Grocery Platforms Outsourcing Cold Chain Delivery Services

- Retailers Leveraging Technology for Real-Time Tracking and Efficient Delivery

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now