Download PDF

Download PDFMarket Overview

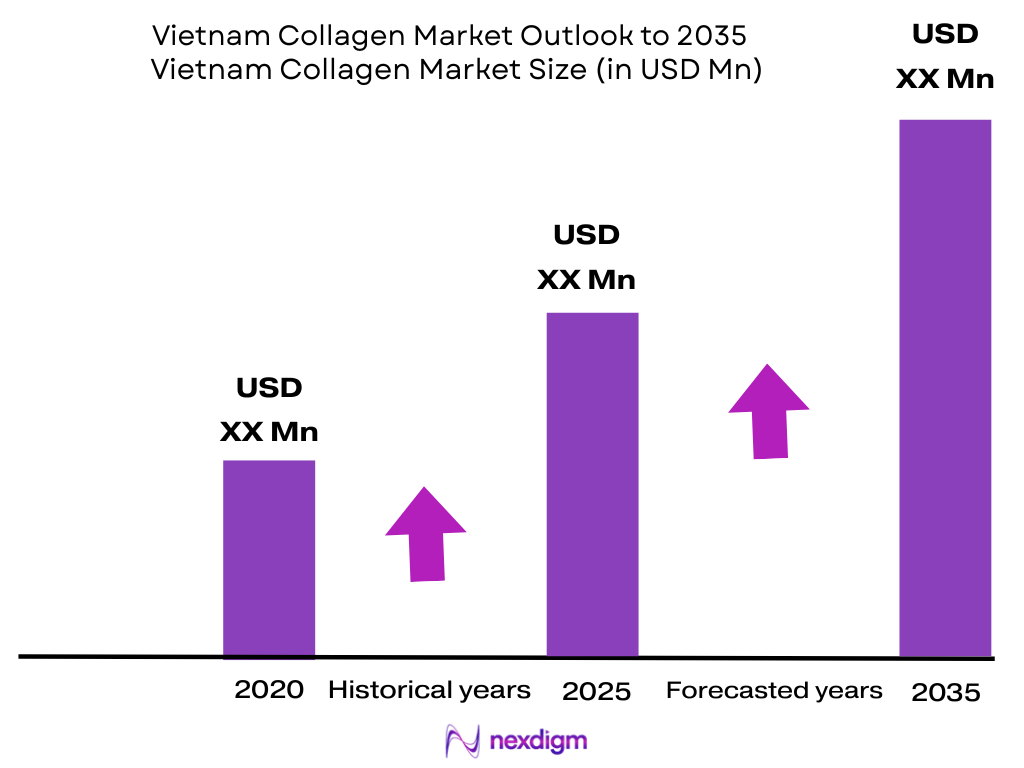

The Vietnam Collagen Supplements Market is valued at USD ~ million, based on a five-year historical analysis, and is expected to record 6.2% CAGR in the available long-term ASEAN collagen peptide outlook through 2035. The market is driven by marine collagen drinks, powders, tablets, jellies, capsules, pharmacy sales and e-commerce distribution. Vietnam’s GDP increased from USD 429.72 billion to USD 476.39 billion, strengthening consumer wellness spending. Ho Chi Minh City, Hanoi, Da Nang, Can Tho and Hai Phong dominate Vietnam collagen demand because they combine pharmacy networks, beauty retail, aesthetic clinics, online shopping and imported Japanese/Korean wellness products. Vietnam’s population increased from 100.35 million to 100.99 million, while GDP per capita increased from USD 4,287.1 to USD 4,717.3, supporting collagen powders, drinks, tablets and jellies in urban middle-income households.

Market Segmentation

By Form

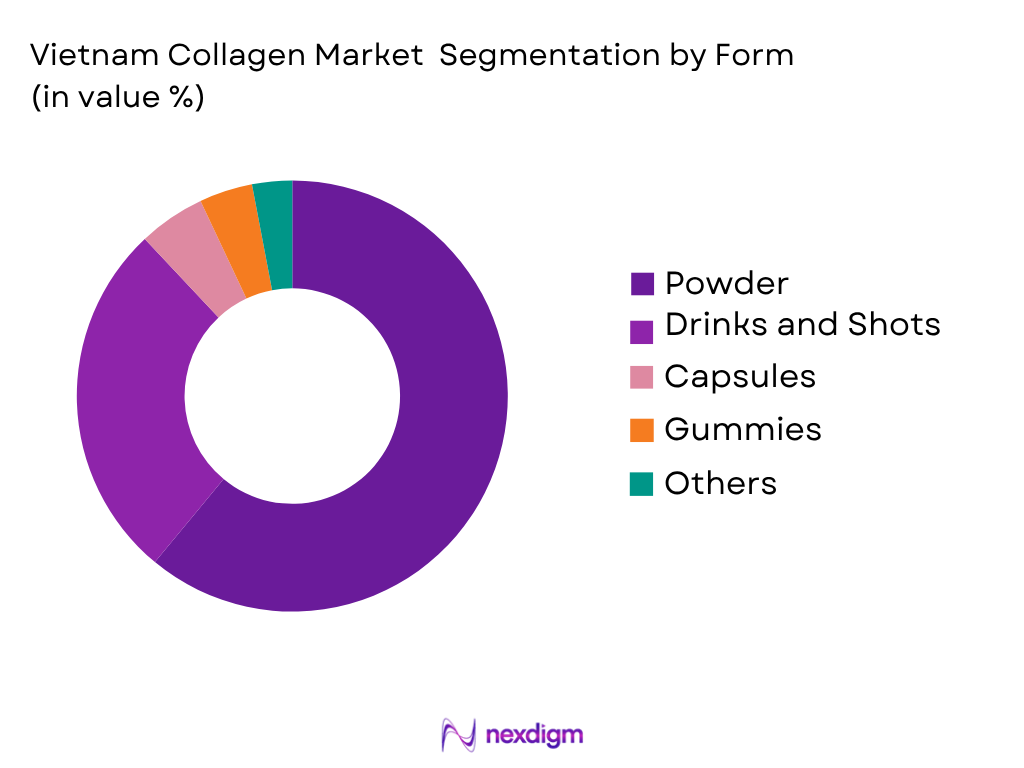

Vietnam collagen market is segmented by form into powder, drinks and shots, capsules, gummies and other formats. Recently, powder has a dominant market share in Vietnam under form segmentation because it offers flexible dosage, lower serving complexity, suitability for hydrolyzed marine collagen peptides, and compatibility with beauty routines involving water, juice, smoothies and functional beverages. Powder products also suit Vietnam’s imported collagen ecosystem, where Japanese, Korean and global brands sell jars, sachets and stick packs through pharmacies, Shopee, Lazada, TikTok Shop and beauty retailers. Powders are preferred by consumers who seek skin hydration, anti-aging, hair and nail support, and joint-health benefits without moving fully into higher-priced liquid beauty shots. Mordor Intelligence states that powder products held 43.10% of Vietnam collagen supplement sales, confirming their leading role in the product mix.

By Distribution Channel

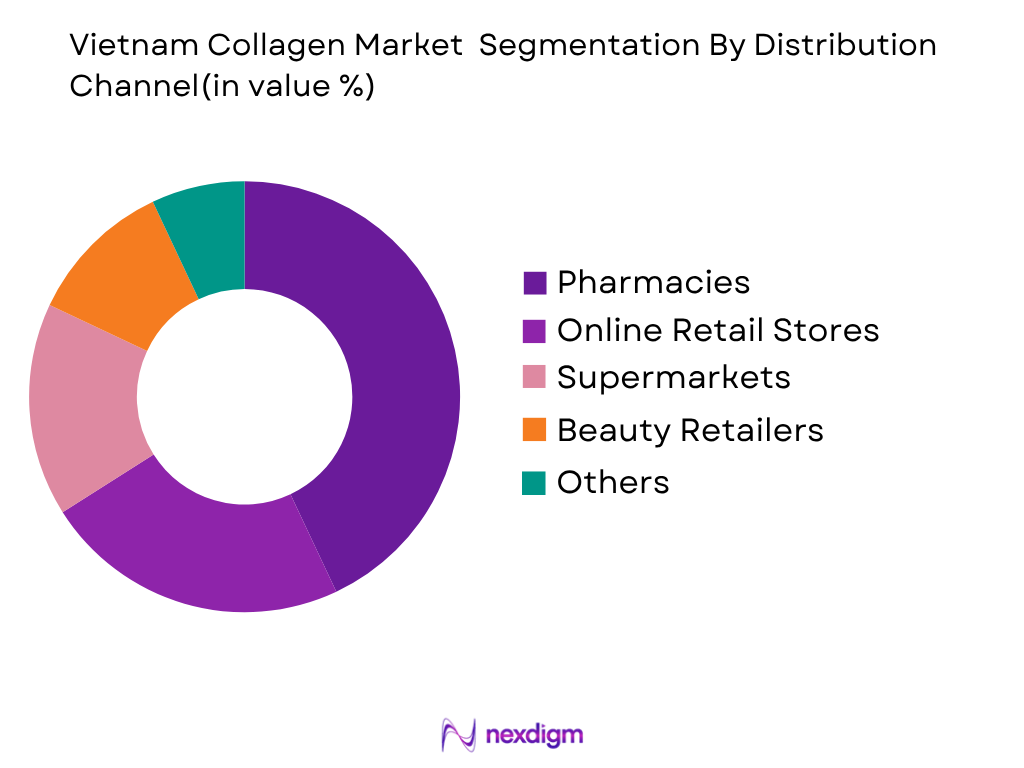

Vietnam collagen market is segmented by distribution channel into pharmacies/drug stores, online retail stores, supermarkets and hypermarkets, beauty retailers, and other channels. Recently, pharmacies and drug stores have a dominant market share in Vietnam under distribution channel segmentation because collagen is commonly classified and sold as a health protection food, making consumer trust, product registration, labeling and pharmacist recommendation important purchase factors. Pharmacy chains such as Long Châu, Pharmacity and An Khang support collagen visibility among consumers purchasing skin, joint, hair, nail and anti-aging products. This channel is also important because imported collagen products require documentation and consumer confidence around authenticity. Mordor Intelligence reports that pharmacies and drug stores commanded 56.15% of Vietnam collagen supplement sales, while online stores are the fastest-growing channel because of marketplace discovery, reviews and live-commerce promotion.

Competitive Landscape

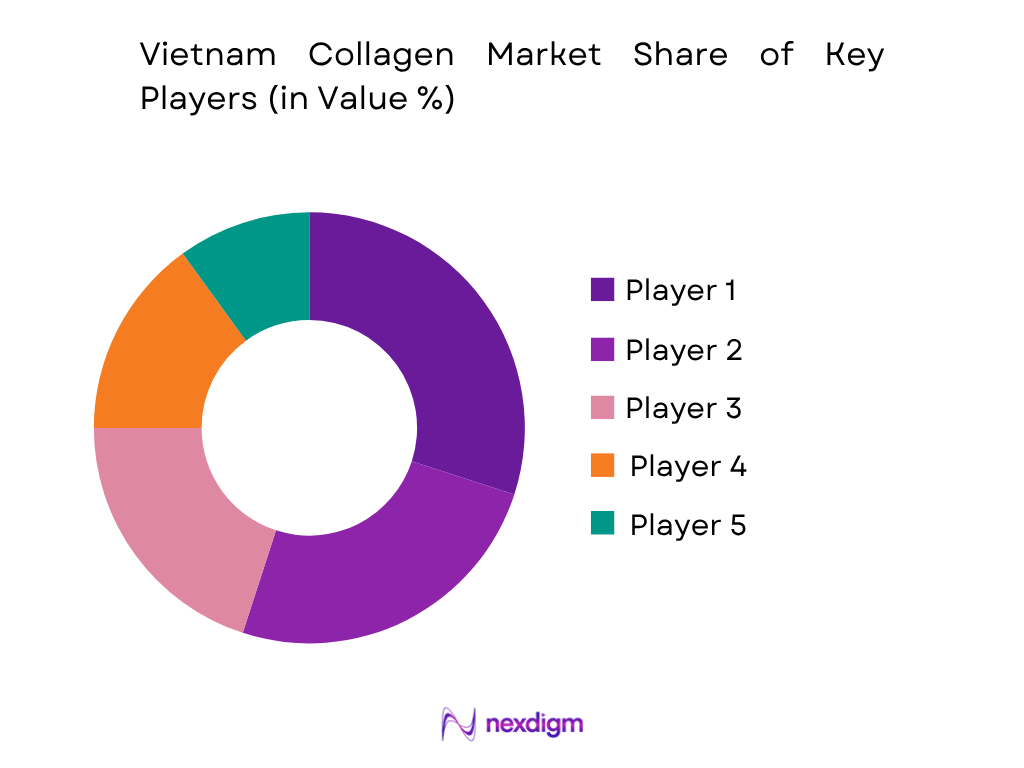

The Vietnam collagen market is moderately concentrated, with imported Japanese, Korean, U.S. and Australian brands competing against domestic distributors and emerging local wellness sellers. Imported brands are influential because Vietnamese consumers associate Japanese and Korean collagen with beauty-from-within, skin hydration and anti-aging routines. Pharmacy chains, e-commerce marketplaces and social-commerce sellers create a fragmented sales environment, but established brands benefit from trust, product documentation, QR verification, distributor control and recognizable country-of-origin positioning. Mordor Intelligence describes Vietnam collagen supplement market concentration as medium and identifies the market as segmented by form, source, end user and distribution channel.

| Company | Establishment Year | Headquarters | Collagen Portfolio | Main Source Focus | Application Coverage | Vietnam Market Role | Distribution Model | Strategic Strength |

| Shiseido | 1872 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Meiji Holdings | 1917 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| DHC | 1972 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Vital Proteins / Nestlé Health Science | 2013 | Chicago, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| NeoCell | 1998 | Irvine, California, USA | ~ | ~ | ~ | ~ | ~ | ~ |

Vietnam Collagen Market Analysis

Growth Drivers

Urban Wellness Consumption Supporting Collagen Powders, Drinks and Jellies

Vietnam collagen market is supported by a large urban consumer economy where collagen is positioned for skin hydration, hair support, nail health, anti-aging routines and joint mobility. World Bank reports Vietnam’s GDP at USD 476.39 billion and GDP per capita at USD 4,717.3 in 2024, supporting demand for premium imported wellness products. Vietnam’s population reached 100.99 million in 2024, creating a broad consumer base for pharmacy, beauty retail and online supplement distribution. The collagen category benefits because powders, drinks, jellies and capsules are mainly sold as daily beauty and health-protection products in urban retail channels.

Digital Commerce Expansion Improving Collagen Product Discovery

Vietnam collagen market is driven by e-commerce and social-commerce expansion because collagen products rely heavily on marketplace search, product reviews, livestream selling, beauty influencers and imported-brand comparison. The Vietnam Government Portal reported that the country’s e-commerce market reached USD 25 billion in 2024, making it the third-largest e-commerce scale in Southeast Asia after Indonesia at USD 65 billion and Thailand at USD 26 billion. This directly supports collagen powders, drinks, jelly sticks and capsules sold through Shopee, Lazada, TikTok Shop and pharmacy websites. World Bank data also places Vietnam’s GDP at USD 476.39 billion, supporting wider online health-product consumption.

Market Challenges

Health Supplement Registration and Advertising Compliance Burden

Vietnam collagen market faces a regulatory challenge because collagen products are commonly sold as health supplements or health protection foods, requiring product declaration, labeling compliance and advertising control. Vietnam’s Decree 15/2018/ND-CP covers 10 food-safety areas, including product self-declaration, registration of product declarations, imported and exported food inspection, food labeling, food advertisement, health supplement production conditions and tracing of food origin. This affects collagen drinks, powders, capsules and jellies using beauty or joint-support claims. In a USD 476.39 billion economy, compliance documentation becomes a core entry barrier for imported and domestic collagen brands.

Grey Imports and Counterfeit Risk in Social-Commerce Collagen Sales

Vietnam collagen market faces authenticity and trust challenges because imported Japanese, Korean, U.S. and Australian collagen products are frequently distributed through marketplaces, livestreams and informal sellers. The Vietnam Government Portal reported nearly 725,000 organizations and individuals conducting business on e-commerce platforms, creating wide reach but also higher product-verification pressure for health supplements. Decree 15/2018/ND-CP includes food labeling, food advertisement, imported food inspection and origin tracing, which are directly relevant to collagen products sold with QR codes, distributor stickers and Vietnamese-language labels. World Bank reports Vietnam’s population at 100.99 million, widening both legitimate and grey-channel demand.

Market Opportunities

Marine Collagen Development from Seafood and Pangasius Processing

Vietnam collagen market has an opportunity in domestic marine collagen because fish skin, scales and pangasius by-products can be converted into Type I collagen peptides for beauty drinks, powders, sachets and jelly sticks. Vietnam’s fisheries sector reported total seafood output of nearly 9.61 million tons in 2024, including 5.75 million tons from aquaculture and 3.85 million tons from capture fishing, while pangasius exports reached USD 1.88 billion. This supports local ingredient development rather than full reliance on imported collagen. World Bank data shows GDP per capita of USD 4,717.3, supporting premium marine collagen demand among urban consumers.

Pharmacy-Led Trust Building for Registered Collagen Products

Vietnam collagen market has a strong opportunity in pharmacy-led sales because collagen is often positioned as a health protection food, where consumers value registration, pharmacist recommendation, traceable importers and product authenticity. Decree 15/2018/ND-CP requires rules covering product declaration registration, food labeling, food advertisement, imported food inspection and origin tracing, supporting formal-channel differentiation for compliant collagen products. Vietnam’s population reached 100.99 million, and GDP per capita stood at USD 4,717.3 in 2024, creating an expanding base for verified beauty and joint-health supplements. Brands that strengthen pharmacy listings can reduce grey-import risk and improve repeat purchases.

Future Outlook

Vietnam collagen market is expected to expand steadily over the next decade, driven by urban beauty consumption, Japanese and Korean nutricosmetic influence, pharmacy-led product trust, and fast digital commerce adoption. The available Vietnam collagen supplement forecast indicates market movement from USD 139.82 million to USD 188.90 million, while the updated market outlook places the category at USD 157.58 million in 2026 and USD 212.07 million by 2031. For the long-term outlook to 2035, publicly available Vietnam-specific collagen CAGR data is limited. The closest available long-term benchmark is the ASEAN collagen peptide outlook, which indicates 6.2% CAGR from 2025 to 2035. This benchmark is directionally relevant because Vietnam is part of ASEAN and has strong exposure to imported collagen peptides, marine beauty formats and functional supplements. Future demand will be concentrated in powder sachets, liquid collagen bottles, jelly sticks, tablets, capsules, collagen gummies and collagen beauty foods. Consumers will increasingly look for marine collagen, low molecular weight peptides, hyaluronic acid, vitamin C, glutathione, elastin and ceramide combinations. Japanese and Korean formats will continue shaping product innovation, especially in Ho Chi Minh City and Hanoi. The market will also be influenced by regulatory scrutiny. Vietnam’s Decree 15 requires registration for health supplements, and imported products require documentation such as certificates and testing results. Advertisement content for health supplements must also be registered and must carry the required disclaimer that the product is not a drug and is not intended to replace medicine.

Major Players

- Shiseido

- Meiji Holdings

- DHC

- FANCL

- Orihiro

- The Collagen by Shiseido

- InnerB / CJ Wellcare

- Vital Proteins / Nestlé Health Science

- NeoCell

- Youtheory

- GNC

- Nature’s Way

- Swisse

- N-Collagen

- Hebora Collagen

Key Target Audience

- Collagen supplement importers

- Health protection food distributors

- Pharmacy and drugstore chains

- Beauty and nutricosmetic brands

- E-commerce and social-commerce wellness sellers

- Functional food and beverage manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies, Vietnam Food Administration, Ministry of Health, Ministry of Industry and Trade, Vietnam E-Commerce and Digital Economy Agency

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map of Vietnam collagen market, covering importers, Japanese and Korean brands, pharmacies, beauty retailers, e-commerce platforms, health protection food registrants, seafood processors and regulators. The objective is to define key variables such as source, form, channel, product registration, country of origin, claims, pricing architecture and consumer use case.

Step 2: Market Analysis and Construction

In this phase, historical and current data is compiled across collagen supplement revenue, imported product activity, pharmacy placement, e-commerce listings, form-factor demand, end-user profile and source mix. The analysis evaluates powders, drinks, tablets, capsules, jellies and gummies across beauty, joint-health, wellness and functional food applications.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted interviews with import distributors, pharmacy buyers, online sellers, beauty retailers, health supplement registrants, seafood processors and functional food manufacturers. These consultations help validate assumptions around powder dominance, pharmacy strength, Japanese/Korean brand influence, grey-import risk and social-commerce growth.

Step 4: Research Synthesis and Final Output

The final phase combines top-down market indicators with bottom-up SKU, channel and company-level checks. This approach validates Vietnam collagen market size, segmentation, competition, demand outlook, regulatory pressure and future growth opportunities, producing a structured view for investors, manufacturers, importers, retailers and consumer-health companies.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Validation, Bottom-Up Validation, Import Mapping, SKU Benchmarking, Primary Interviews, Regulatory Review, Competitive Mapping, Forecast Model, Limitations)

- Definition and Scope

- Market Genesis and Evolution

- Timeline of Major Players

- Business Cycle and Beauty Supplement Seasonality

- Growth Drivers (Japanese Beauty Influence, Korean Inner Beauty Trend, E-Commerce Penetration, Urban Female Consumers, Seafood Processing Base, Pharmacy Retail Expansion, Functional Food Adoption)

- Market Challenges (Grey Imports, Counterfeit Products, Advertising Violations, Product Registration Burden, Source Disclosure, Marine Allergen Risk, Low Consumer Awareness of Dosage)

- Market Opportunities (Domestic Marine Collagen, Pangasius Skin Valorization, Beauty Drinks, Collagen Jellies, Clinical Joint Formulas, Pharmacy-Led Premiumization, Pet Collagen, Medical-Grade Collagen)

- Market Trends (Collagen Drinks, Jelly Sticks, Marine Collagen, Hyaluronic Acid Pairing, Vitamin C Pairing, Low Molecular Weight Claims, TikTok Shop Selling, QR Authentication)

- SWOT Analysis

- Porter’s Five Forces

- PESTLE Analysis

- By Value (2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Source (In Value %)

Marine Collagen

Bovine Collagen

Porcine Collagen

Poultry Collagen - By Product Type (In Value %)

Hydrolyzed Collagen Peptides

Gelatin

Native Collagen

Undenatured Type II Collagen

Collagen Beauty Foods - By Distribution Channel (In Value %)

Import Distributors

Pharmacies and Drugstores

Beauty Retailers

Supermarkets and Modern Trade

E-Commerce Marketplaces - By Region (In Value %)

Ho Chi Minh City

Hanoi

Da Nang

Can Tho and Mekong Delta

Hai Phong and Northern Industrial Belt

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (Collagen Source Portfolio, Product Format Portfolio, Country-of-Origin Positioning, Vietnam Regulatory Registration Readiness, Pharmacy and E-Commerce Reach, QR Authentication and Anti-Counterfeit Systems, Ingredient Stacking Capability, Influencer and Livestream Commerce Strength)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Shiseido

Meiji Holdings

DHC

FANCL

Orihiro

The Collagen by Shiseido

InnerB / CJ Wellcare

Vital Proteins / Nestlé Health Science

NeoCell

Youtheory

GNC

Nature’s Way

Swisse

N-Collagen

Hebora Collagen

- Supplement Brand Demand

- Beauty and Nutricosmetic Brand Demand

- Food and Beverage Manufacturer Demand

- Pharmacy and Drugstore Demand

- E-Commerce Seller Demand

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now