Download PDF

Download PDFMarket Overview

The Vietnam Food Acidulants Market was valued at approximately USD ~ billion in 2024 and is projected to grow at a CAGR of ~% during the 2026–2035 forecast period. The market is driven by the rapid expansion of Vietnam’s food and beverage processing industry, the country’s globally significant seafood and fish sauce processing sector, rising urbanisation and demand for processed and convenience foods, and growing production of instant noodles, RTD beverages, sauces, condiments, and packaged snacks that rely on acidulants for pH regulation, preservation, flavour enhancement, and shelf-life extension. Vietnam is one of Southeast Asia’s fastest-growing food processing economies, with the food and beverage sector contributing approximately USD 30 billion to national output according to the General Statistics Office of Vietnam (GSO) and the Vietnam Food Administration (VFA). According to the World Bank, Vietnam’s GDP reached approximately USD 430 billion in 2024, with sustained economic growth at approximately 6–7% annually supporting continued expansion of domestic food manufacturing and food export capabilities. Food acidulants — encompassing citric acid, lactic acid, acetic acid, malic acid, tartaric acid, phosphoric acid, fumaric acid, glucono-delta-lactone, and ascorbic acid — are essential ingredients across multiple food processing categories in Vietnam, from the country’s iconic fish sauce and fermented food traditions to its large-scale instant noodle manufacturing and rapidly growing RTD beverage sector. The Vietnam food acidulants market is characterised by heavy reliance on imported citric acid — predominantly sourced from Chinese manufacturers — alongside growing demand for specialty acidulants, fermentation-derived organic acids, and natural acidulant alternatives across Vietnam’s expanding and increasingly sophisticated food processing industry.

Market Segmentation

By Acidulant Type

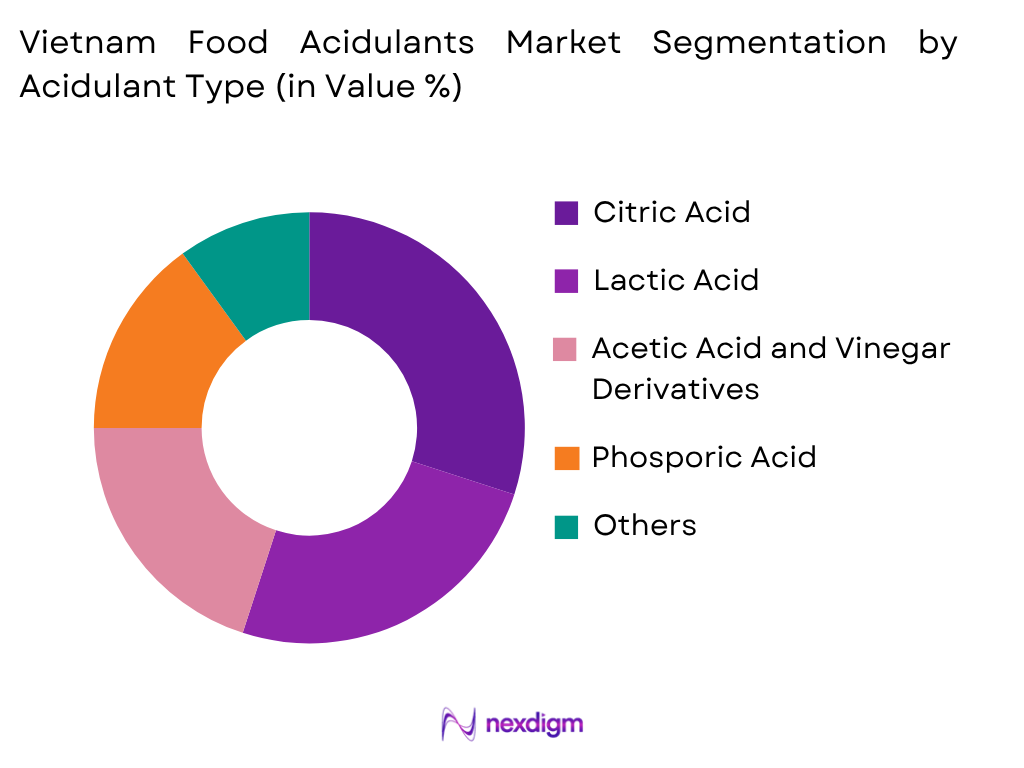

Citric acid dominates the Vietnam food acidulants market by volume and value, driven by its exceptionally broad application range across beverages, processed foods, condiments, seafood processing, and confectionery, combined with competitive pricing through well-established import supply chains primarily from Chinese manufacturers. According to industry estimates and Vietnam Customs data, citric acid accounts for the largest share of food acidulant imports into Vietnam, with the beverage sector — encompassing RTD soft drinks, juices, energy drinks, and flavoured waters — representing the single largest end-use application. Lactic acid and lactates represent the second-largest and fastest-growing segment, driven by their dual functionality as both pH regulators and natural preservation agents, aligning with Vietnam’s growing demand for cleaner-label preserved foods, as well as their important role in dairy acidification for yoghurt and cultured dairy product manufacturing. Acetic acid and food-grade vinegar occupy a distinctive position in the Vietnamese market given the country’s deeply embedded culinary traditions of fermented and pickled foods, condiments, and fish-based sauces where acetic acid plays both a functional and flavour role. Malic acid is gaining market share in the beverage sector, particularly among energy drink, sports drink, and flavoured beverage manufacturers who prefer its smoother, longer-lasting sour profile compared to citric acid for specific flavour applications. The phosphoric acid segment, while primarily serving the carbonated soft drink sector, represents a stable and well-established demand base closely tied to cola and carbonated beverage production volumes across Vietnam’s large and growing beverage manufacturing industry.

By Application

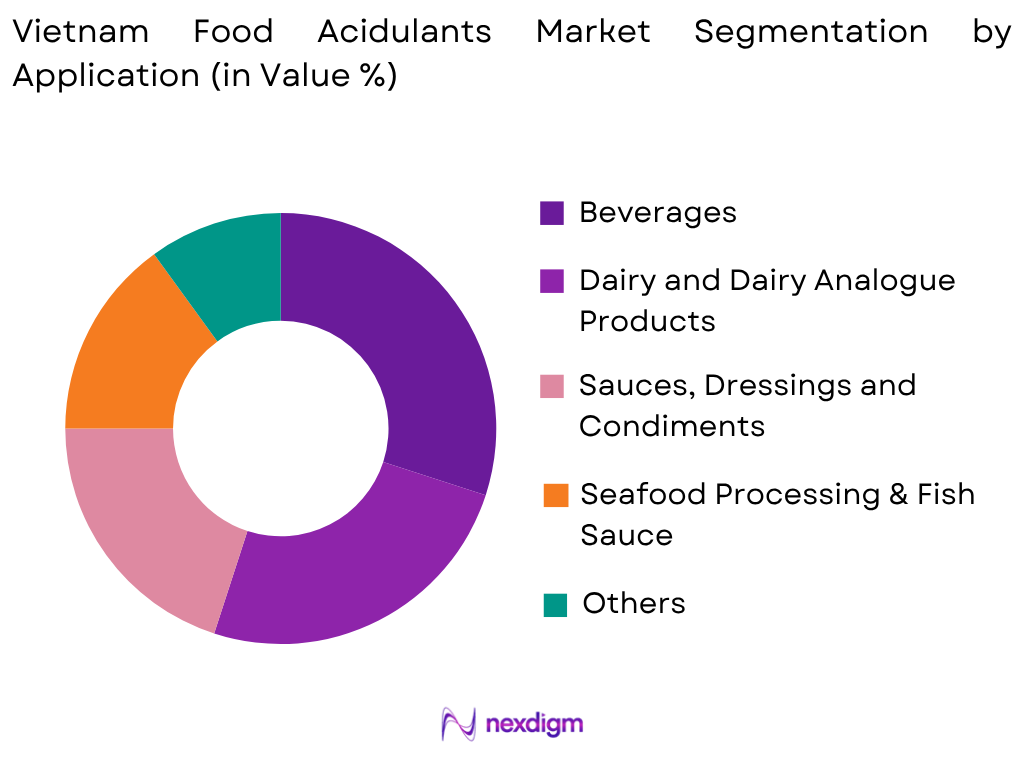

Beverages represent the largest application segment for food acidulants in Vietnam, encompassing RTD soft drinks, energy drinks, sports beverages, juices, flavoured waters, and carbonated drinks produced by both international companies including Coca-Cola Vietnam, PepsiCo Vietnam, and Red Bull Vietnam, alongside domestic beverage manufacturers including Tan Hiep Phat, Chuong Duong Beverages, and Sabeco’s non-alcoholic lines. Citric acid and phosphoric acid are critical acidulation and flavour components in these beverage categories, with inclusion rates and sourcing volumes directly proportional to Vietnam’s rapidly growing per capita RTD beverage consumption. Seafood processing and fish sauce production represent a uniquely Vietnamese and regionally significant application segment, encompassing the country’s large-scale shrimp, pangasius, and tilapia processing industries — which generated approximately USD 9 billion in seafood export revenues according to VASEP — as well as the traditional fish sauce (nuoc mam) and fermented seafood condiment sectors where acetic acid, lactic acid, and citric acid play essential preservation, pH control, and food safety roles. Processed food and convenience food manufacturing — including Vietnam’s iconic instant noodle sector led by Masan Consumer, Acecook Vietnam, Uniben, and Vifon, collectively producing billions of servings annually — represents another major acidulant application, with citric acid and lactic acid used extensively for flavour seasoning, pH stabilisation, and preservation of seasoning powder packets and sauce sachets.

Competitive Landscape

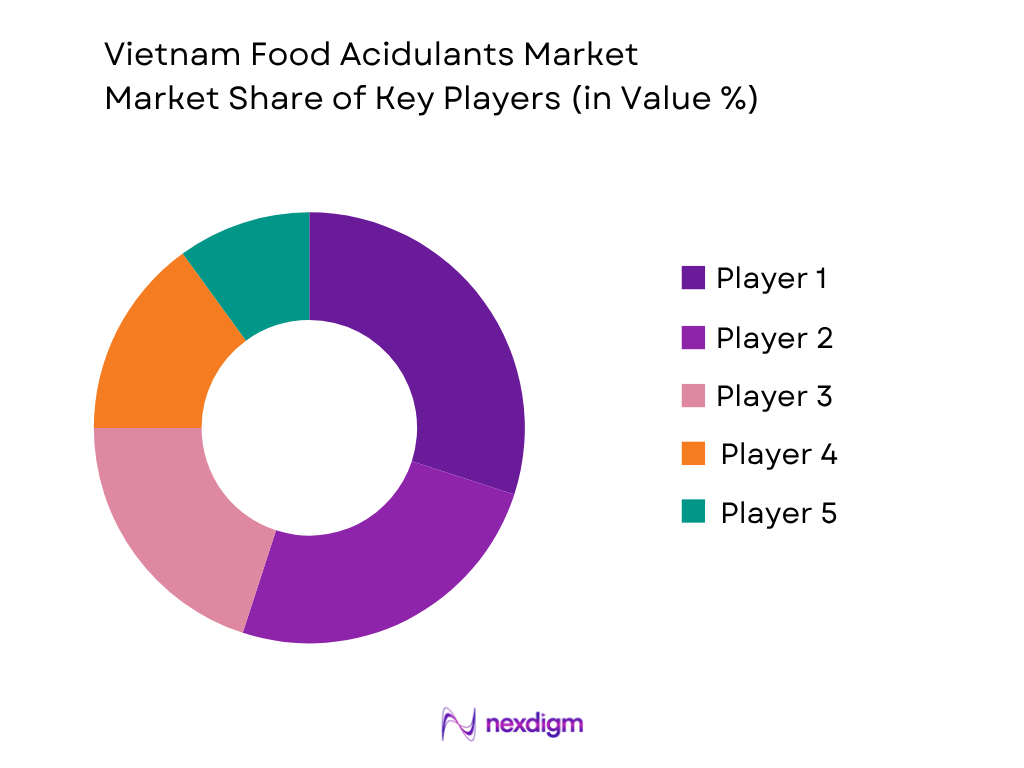

The Vietnam Food Acidulants Market is moderately competitive, with international specialty ingredient companies competing alongside Chinese citric acid manufacturers and their local trading agents who dominate the commodity citric acid segment on price competitiveness. Global specialty ingredient companies including Jungbunzlauer, Corbion, Cargill, and ADM compete through product quality, technical service support, and specialty acidulant portfolios encompassing lactic acid, malic acid, fumaric acid, and fermentation-derived organic acids targeting the growing premium food manufacturing and export-oriented processing segments. Chinese manufacturers — including Weifang Ensign Industry, COFCO Biochemical, and TTCA — dominate the commodity citric acid supply through competitive pricing, but periodic quality concerns and supply concentration risks are increasingly encouraging Vietnamese food manufacturers to diversify sourcing toward European and specialty suppliers. VFA regulatory compliance documentation, consistent supply reliability, technical application support, and price competitiveness represent the primary competitive differentiators across the Vietnamese food acidulants market.

| Company | Establishment Year | Headquarters | Primary Acidulant Portfolio | Key Application Industries

|

Manufacturing Presence | R&D Capability | Distribution Network | Clean Label Solutions |

| Jungbunzlauer Vietnam | 1867 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Corbion Vietnam | 1919 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Cargill Vietnam | 1987 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| ADM Vietnam (Archer Daniels Midland) | 1902 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Brenntag Vietnam (Distribution) | 1874 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

Vietnam Food Acidulants Market Analysis

Growth Drivers

Rapid Expansion of Vietnam’s Food and Beverage Processing Sector

Vietnam’s sustained economic growth and rapid expansion of its food and beverage manufacturing sector continue to be the most fundamental drivers of food acidulant demand. According to the General Statistics Office of Vietnam (GSO), the food and beverage processing sector is one of the country’s largest industrial contributors, with output growing consistently at rates significantly above the broader industrial sector average, driven by rising domestic consumption, export market expansion, and continued investment by both domestic and foreign companies in food manufacturing capacity. The World Bank reported Vietnam’s GDP at approximately USD 430 billion in 2024, with the country maintaining one of Southeast Asia’s highest economic growth rates at approximately 6–7% annually, progressively elevating household incomes and expanding consumer purchasing power for packaged and processed food products. The rapid growth of Vietnam’s RTD beverage sector — driven by companies including Tan Hiep Phat, Red Bull Vietnam, Coca-Cola Vietnam, and PepsiCo Vietnam — has significantly expanded citric acid and phosphoric acid demand, as beverages represent the single largest acidulant application category by volume. Vietnam’s instant noodle sector, one of the world’s largest by per capita consumption according to the World Instant Noodle Association (WINA), continues to expand production volumes driven by domestic demand and export growth, with acidulants playing essential roles in seasoning formulation and preservation. The entry into force of the EU-Vietnam Free Trade Agreement (EVFTA), CPTPP, and RCEP has further accelerated food export growth, driving investment in food manufacturing capacity and quality standards that increase demand for internationally compliant food ingredient supply chains including certified food-grade acidulants.

Vietnam’s Globally Significant Seafood Processing Industry

Vietnam’s position as one of the world’s leading seafood exporters creates a structurally important and distinctive demand driver for food acidulants that is unique to the Vietnamese market within the Southeast Asian context. According to the Vietnam Association of Seafood Exporters and Producers (VASEP), Vietnam generated approximately USD 9 billion in seafood export revenues in 2024, with shrimp, pangasius (catfish), and tilapia collectively accounting for the majority of export value, shipped primarily to the European Union, United States, Japan, China, and ASEAN markets. Food-grade citric acid, lactic acid, sodium citrate, and sodium lactate are extensively used in Vietnam’s seafood processing operations for water pH adjustment during processing, marinade and brine formulation, antimicrobial surface treatment, preservation and shelf-life extension, and colour stabilisation in processed seafood products. The increasingly stringent food safety and quality requirements imposed by importing markets — particularly the EU’s food contaminant regulations, the US FDA’s seafood HACCP requirements, and Japan’s rigorous food additive standards — drive Vietnamese seafood processors to source high-purity, food-grade certified acidulants from internationally recognised suppliers rather than lower-cost commodity sources. The traditional Vietnamese fish sauce (nuoc mam) and fermented seafood condiment sector, while primarily relying on natural fermentation-derived acidity, also utilises food-grade acetic acid and citric acid as supplementary acidulants and preservation aids across large-scale industrial production. Growth in Vietnam’s aquaculture output and export volumes is therefore expected to generate sustained incremental acidulant demand across seafood processing applications throughout the outlook period.

Market Challenges

High Import Dependency and Chinese Citric Acid Price Volatility

Vietnam’s food acidulants market faces a significant structural challenge in the form of near-complete import dependency for citric acid — the market’s largest volume ingredient — and the consequent exposure to Chinese citric acid production and pricing dynamics that create persistent supply and cost volatility for Vietnamese food manufacturers. According to Vietnam Customs statistics, the overwhelming majority of citric acid consumed by Vietnam’s food and beverage manufacturing sector is imported from Chinese manufacturers, reflecting China’s dominant position in global citric acid production — with Chinese manufacturers accounting for approximately 70–75% of global citric acid supply. This supply concentration creates material risks for Vietnamese food manufacturers when Chinese production is disrupted by environmental compliance shutdowns, energy cost increases, or government-mandated production restrictions, as experienced during China’s periodic regulatory crackdowns on industrial fermentation capacity. Chinese citric acid export prices have historically exhibited significant volatility, with price swings of 30–50% within single calendar years occurring on multiple occasions, creating substantial procurement cost uncertainty for Vietnamese beverage, snack, and condiment manufacturers operating with thin margin structures in competitive domestic and export markets. Simultaneously, Vietnam’s own domestic production capability for citric acid and other major acidulants remains negligible, with no significant domestic fermentation-based organic acid manufacturing capacity currently operating at commercial scale, meaning that all supply chain resilience must be achieved through import source diversification rather than domestic production development. Efforts to diversify citric acid sourcing toward European and other non-Chinese suppliers provide supply chain resilience but typically at meaningfully higher cost, creating a persistent trade-off between price and supply security for Vietnamese procurement managers.

VFA Regulatory Compliance and Intense Price Competition

Vietnamese food acidulant manufacturers and importers face ongoing challenges associated with navigating the Vietnam Food Administration’s food additive regulatory framework and managing intense price competition from low-cost regional suppliers, particularly Chinese commodity acid exporters. According to the Ministry of Health and the Vietnam Food Administration (VFA), food additives used in Vietnam’s food manufacturing sector must comply with the Permitted List of Food Additives prescribed under Circular 24/2019/TT-BYT and related national technical regulations (QCVN), with manufacturers required to obtain VFA food additive approval documentation, product registration, and import permits before commercial use in food products. The regulatory approval process, while generally aligned with CODEX Alimentarius standards, requires systematic documentation of identity specifications, purity standards, and technical dossiers for each acidulant grade and application category, creating compliance complexity and administrative cost particularly for specialty and novel acidulant types not previously approved under the Vietnamese permitted list. Simultaneously, the Vietnamese food ingredient market is highly price-competitive, with Chinese commodity acidulant suppliers — particularly in citric acid, acetic acid, and phosphoric acid — able to undercut specialty European and North American suppliers on price by substantial margins, creating persistent commercial pressure on higher-quality suppliers. This price competition is particularly acute among Vietnam’s large base of small and medium-sized food manufacturers who make procurement decisions primarily on cost, limiting the addressable market for premium specialty acidulants to the more sophisticated larger manufacturers targeting export markets with stringent quality and food safety requirements.

Market Opportunities

Natural and Bio-Based Acidulant Demand Growth and Seafood Export Expansion

Vietnam’s growing consumer health awareness and the increasingly stringent food safety and ingredient quality requirements of premium export markets are creating significant opportunities for natural, bio-based, and fermentation-derived food acidulants that can replace synthetic alternatives in clean-label food formulations. According to the Vietnam Food Administration and market research agencies, Vietnamese consumers — particularly in urban centres including Hanoi and Ho Chi Minh City — are demonstrating increasing awareness of food additive content and growing preference for products formulated with naturally derived ingredients, creating commercial incentives for food manufacturers targeting premium domestic and export markets to transition toward fermentation-derived lactic acid, natural malic acid, and bio-based citric acid from EU-certified producers. The EVFTA’s preferential market access to the European Union — a market with among the world’s most stringent clean-label and natural ingredient requirements — creates strong incentives for Vietnam’s export-oriented food manufacturers to upgrade ingredient specifications toward EU-compliant natural and bio-based acidulant sources. Vietnam’s seafood export sector, targeting premium markets in Japan, South Korea, the EU, and the United States, increasingly demands internationally certified, high-purity food-grade acidulants from traceable and auditable supply chains — requirements that favour specialty European producers including Jungbunzlauer and Corbion over lower-cost commodity suppliers with less comprehensive quality documentation. Investment in fermentation-based organic acid production using Vietnam’s abundant domestic sugarcane, cassava, and agricultural residue feedstocks could also create domestic manufacturing opportunities for lactic acid and other bio-based acidulants, reducing import dependency while serving the growing clean-label demand of Vietnam’s premium food processing sector.

Premium Beverage Innovation and EVFTA-Driven Export Food Production Growth

Vietnam’s rapidly evolving premium beverage sector and the structural export market growth driven by free trade agreements are creating high-value growth opportunities for specialty food acidulants targeting sophisticated flavour performance and clean-label positioning. According to the General Statistics Office of Vietnam and the Vietnam Beverage Association, Vietnam’s RTD beverage market is experiencing strong growth driven by rising incomes, urbanisation, and increasing consumer demand for functional beverages, sports drinks, premium juices, and health-oriented beverage formats that require sophisticated acidulation systems beyond standard citric acid-based formulations. Malic acid’s superior flavour profile for fruit-forward beverages, tartaric acid’s role in premium wine and grape-inspired drink formulations, and lactic acid’s application in kombucha, probiotic beverages, and fermented drink categories each represent growing specialty acidulant demand streams within Vietnam’s expanding premium beverage segment. The EVFTA’s elimination or progressive reduction of tariffs on Vietnamese food and beverage exports to the EU — a market of approximately 450 million high-income consumers — is incentivising Vietnamese food manufacturers to invest in product quality, ingredient certification, and regulatory compliance upgrades that require sourcing internationally certified food-grade acidulants meeting EU food additive standards. Similar dynamics apply under CPTPP — providing preferential access to Japan, Australia, Canada, and other premium markets — and RCEP, which expands access to China, South Korea, and ASEAN partners. These trade agreement-driven export growth incentives are progressively shifting Vietnamese food manufacturers toward higher-specification ingredient sourcing, creating a growing commercial opportunity for specialty acidulant suppliers with strong technical credentials and internationally recognised quality certifications.

Future Outlook

The Vietnam Food Acidulants Market is expected to experience robust growth throughout the forecast period, supported by the continued rapid expansion of Vietnam’s food and beverage processing sector, seafood export volume growth, rising domestic demand for processed and convenience foods, and free trade agreement-driven export market development under EVFTA, CPTPP, and RCEP. Demand for specialty acidulants — including fermentation-derived lactic acid, natural malic acid, and bio-based organic acids — is expected to grow at a faster rate than commodity citric acid as Vietnamese food manufacturers targeting premium export markets upgrade ingredient specifications and clean-label positioning. The potential development of domestic bio-based organic acid production using Vietnam’s abundant agricultural fermentation feedstocks represents a long-term structural opportunity to reduce import dependency. Continued expansion of the RTD beverage sector, growth in seafood processing export volumes, and increasing instant noodle and packaged snack production are expected to sustain strong baseline citric acid demand while specialty acidulant categories capture growing market share from the premium and export-oriented manufacturing segments.

Major Players

- Jungbunzlauer Vietnam

- Corbion Vietnam

- Cargill Vietnam

- ADM Vietnam

- Brenntag Vietnam

- TTCA (Thai company supplying Vietnam)

- Weifang Ensign Industry (China-origin citric acid)

- COFCO Biochemical (China-origin citric acid)

- Foodchem International Vietnam

- Sigma-Tau Chemicals Vietnam

- Bartek Ingredients (Malic Acid)

- Fuso Chemical Vietnam

- Naturex (Givaudan) Vietnam

- Univar Solutions Vietnam

- PMP Fermentation Products

Key Target Audience

- Food & Beverage Manufacturers

- Seafood Processing Companies

- Instant Noodle and Packaged Snack Manufacturers

- Sauce, Condiment and Fish Sauce Producers

- Dairy Product Manufacturers

- Food Ingredient Distributors and Importers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Ministry of Health (MOH), Vietnam Food Administration (VFA), National Agro-Forestry-Fisheries Quality Assurance Department (NAFIQAD), Ministry of Industry and Trade (MOIT))

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying all major stakeholders across the Vietnam Food Acidulants Market ecosystem, including acidulant manufacturers, importers, specialty ingredient distributors, food and beverage processors, seafood processing companies, regulatory authorities, and end-use industries. Extensive desk research is conducted using VFA publications, Vietnam Customs trade statistics, GSO economic data, VASEP seafood export statistics, company annual reports, food ingredient databases, industry journals, and proprietary databases to determine the key variables influencing market demand, import supply dynamics, regulatory compliance requirements, and competitive dynamics.

Step 2: Market Analysis and Construction

Historical market information is compiled and analysed to evaluate acidulant import volumes, consumption patterns by application sector, pricing trends, food processing output growth, seafood export volumes, beverage production statistics, and regulatory compliance investment across different food manufacturing categories. A combination of top-down food industry output-based demand modelling and bottom-up import volume analysis is adopted to estimate market revenues, supported by application-level acidulant utilisation rate assessment. Data triangulation techniques are employed to ensure consistency across all market segments and sub-segments.

Step 3: Hypothesis Validation and Expert Consultation

The preliminary market estimates and analytical assumptions are validated through Computer Assisted Telephone Interviews (CATIs) and structured discussions with food acidulant importers and distributors, food and beverage procurement managers, quality assurance specialists, seafood processing technical managers, VFA regulatory affairs professionals, and food industry executives. Their operational and commercial insights are utilised to verify ingredient adoption trends, sourcing strategies, regulatory compliance requirements, pricing dynamics, and future market opportunities while improving the accuracy of market forecasts.

Step 4: Research Synthesis and Final Output

The final phase integrates findings from secondary research and primary interviews to prepare a comprehensive assessment of the Vietnam Food Acidulants Market. Detailed analyses covering market size, segmentation, competitive landscape, import supply chain analysis, application sector demand drivers, regulatory framework, and future growth prospects are developed through multiple rounds of validation. Cross-verification using both supply-side import data and demand-side food production statistics ensures that the final report delivers reliable, actionable, and commercially oriented market intelligence for stakeholders operating in Vietnam’s food acidulants sector.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Rapid Expansion of Vietnam’s Food and Beverage Processing Sector, Rising Urbanisation and Demand for Processed and Convenience Foods, Vietnam’s Large Seafood and Fish Sauce Processing Industry, Free Trade Agreement-Driven Export Market Access, Expanding RTD Beverage and Energy Drink Market, Growing Instant Noodle and Packaged Snack Production)

- Market Challenges (High Import Dependency for Citric Acid and Specialty Acidulants, Price Volatility Due to Chinese Citric Acid Market Fluctuations, Vietnam Food Administration Regulatory Compliance, Intense Price Competition from Low-Cost Regional Suppliers, Raw Material Supply Chain Disruption Risks, Limited Domestic Production of Specialty Acidulants)

- Market Opportunities (Natural and Bio-Based Acidulant Demand Growth, Seafood Export Processing Acidulant Expansion, Premium Beverage Acidulant Innovation, Plant-Based Food Processing Demand, EVFTA and CPTPP Export-Driven Food Production Growth, Fermentation-Derived Acidulant Development)

- Market Trends (Natural Acidulant Preference Growth, Clean Label Ingredient Adoption, Citric Acid Supply Chain Diversification Away from China, Functional Beverage Acidulant Innovation, Seafood Processing Food Safety Compliance, Lactic Acid Fermentation-Based Preservation Trend)

- Government Regulations (Ministry of Health (MOH) Food Safety Regulations, Vietnam Food Administration (VFA) Food Additive Permitted List, National Technical Regulations on Food Additives (QCVN), CODEX Alimentarius Harmonisation, Circular 24/2019/TT-BYT Food Additives Regulation, Export Quality and Food Safety Standards under NAFIQAD)

- Raw Material Supply Analysis (Citric Acid Import Dependency from China, Domestic Sugarcane and Tapioca Fermentation Feedstocks, Lactic Acid Bio-Based Production Potential, Acetic Acid Industrial Supply, Tartaric Acid Import Sources)

- Import Dependency Assessment (Citric Acid, Malic Acid, Fumaric Acid, Tartaric Acid, Phosphoric Acid, Specialty Organic Acids — Predominantly Imported from China, EU and USA)

- Product Application Landscape (Beverage Acidulation, Seafood Preservation, Noodle and Snack Acidulation, Sauce and Condiment pH Control, Dairy Acidification, Bakery Leavening)

- Consumer Health & Food Safety Trends (Clean Label Preference, Natural Preservative Demand, Reduced Synthetic Additive Awareness, Food Safety Consciousness Post-COVID)

- Sustainability Assessment (Bio-Based Acidulant Sourcing, Fermentation-Derived Production, Food Waste Reduction, Carbon Footprint Optimisation)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Acidulant Type (In Value %)

Citric Acid

Acetic Acid & Vinegar

Lactic Acid

Malic Acid

Tartaric Acid

Phosphoric Acid

Fumaric Acid

Glucono-Delta-Lactone (GDL)

Ascorbic Acid

Other Organic Acids - By Source (In Value %)

Synthetic/Chemical Synthesis

Fermentation-Derived

Natural & Bio-Based

Plant-Extracted - By Function (In Value %)

pH Regulation & Acidification

Preservation & Antimicrobial

Flavour Enhancement

Chelation & Antioxidant Synergy

Leavening Agent

Emulsification Support - By Application (In Value %)

Beverages

Processed Foods & Convenience Foods

Condiments, Sauces & Seasonings

Dairy & Dairy Alternatives

Bakery & Confectionery

Seafood Processing & Fish Sauce

Meat Processing

Instant Noodles & Snacks - By Region (In Value %)

Southeast (Ho Chi Minh City Region)

Red River Delta (Hanoi Region)

North Central & Central Coast

Mekong River Delta

- Market Share Analysis (By Value, Volume, Acidulant Type, Application, End User)

- Cross Comparison Parameters (Acidulant Portfolio Breadth, Purity Grade Range, Fermentation vs Synthetic Production, Application Technical Support, Vietnam Distribution Network, VFA Regulatory Compliance, Export-Grade Supply Capability, Price Competitiveness)

- SWOT Analysis of Major Players

- Pricing Analysis (By Acidulant Type, Purity Grade, Application Category, Import Origin, Volume Tier)

- Detailed Profiles of Major Companies

Jungbunzlauer Vietnam

Corbion Vietnam

Cargill Vietnam

ADM Vietnam

Brenntag Vietnam

TTCA

Weifang Ensign Industry

COFCO Biochemical

Foodchem International Vietnam

Sigma-Tau Chemicals Vietnam

Bartek Ingredients

Fuso Chemical Vietnam

Naturex (Givaudan) Vietnam

Univar Solutions Vietnam

PMP Fermentation Products

- Ingredient Utilisation Analysis (Application Intensity, Inclusion Rate, Formulation Complexity, Processing Compatibility)

- Purchasing Criteria Assessment (Price Competitiveness, Purity Grade, VFA Regulatory Compliance, Consistent Supply Availability, Technical Support)

- Product Formulation Analysis (pH Target Achievement, Preservation Efficacy, Flavour Profile Impact, Processing Stability)

- Food Manufacturer Application Preference Analysis (Beverage, Seafood, Noodle, Sauce, Dairy, Bakery Sector Requirements)

- Decision-Making Framework (R&D Teams, Procurement, Quality Assurance, Regulatory Affairs, Production Management)

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now