Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Vietnam’s home finance market represents outstanding residential mortgage loans issued by commercial banks and housing finance institutions to individual borrowers. Based on recent historical assessments from central bank credit statistics and housing finance disclosures, total residential mortgage credit exceeds USD ~ billion, driven by rapid urban housing demand, rising middle-income homeownership aspirations, and expansion of retail lending portfolios among domestic banks transitioning from corporate to consumer credit growth strategies.

Home finance activity is concentrated in Ho Chi Minh City and Hanoi, where urban population density, condominium development, and formal property transactions are highest. These cities host the majority of bank branches, mortgage advisory services, and developer-linked lending programs supporting apartment purchases. Industrialization-driven migration and salaried employment clusters reinforce demand for financed housing ownership in these metropolitan regions, while secondary cities remain less penetrated due to lower formal property supply and banking access.

Market Segmentation

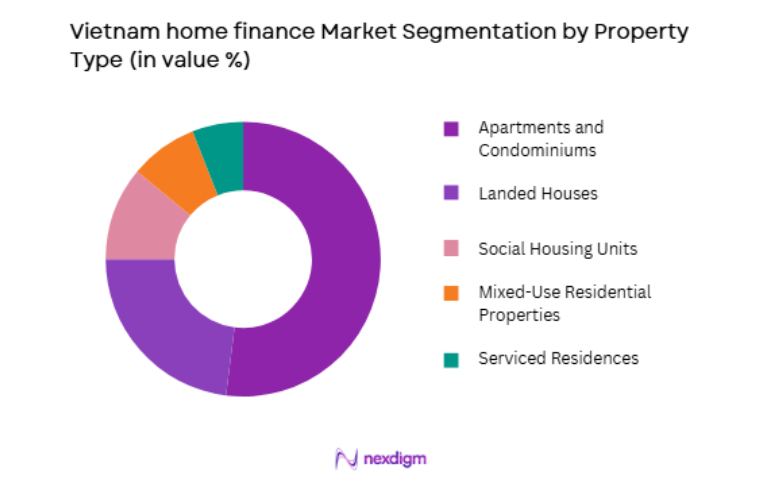

By Property Type

Vietnam Home Finance market is segmented by property type into apartments and condominiums, landed houses, social housing units, serviced residences, and mixed-use residential properties. Recently, apartments and condominiums have a dominant market share due to factors such as urban land constraints, large-scale developer projects, and affordability relative to landed housing. Mortgage lending is closely integrated with condominium presales and developer financing partnerships, enabling banks to originate standardized housing loans at scale. Rapid urban migration toward metropolitan employment hubs reinforces demand for high-density residential units financed through structured installment mortgages. Landed houses are often self-built or informally transacted, reducing formal mortgage penetration. Social housing programs remain limited in supply, while serviced and mixed-use residences target niche investor segments.

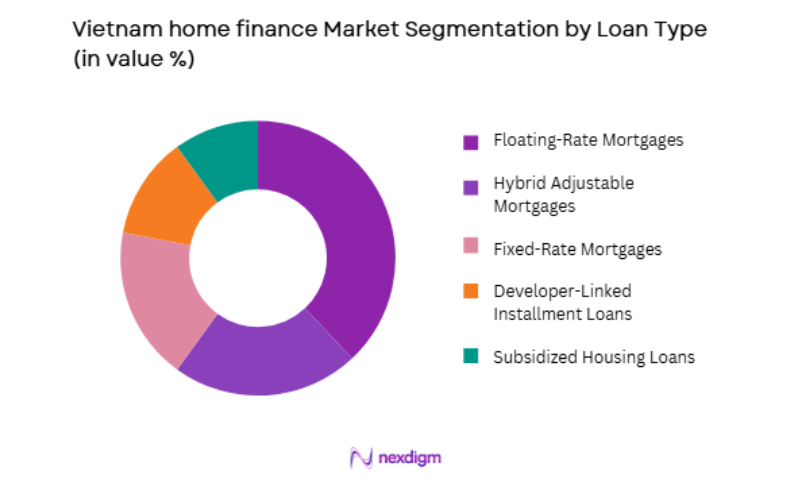

By Loan Type

Vietnam Home Finance market is segmented by loan type into fixed-rate mortgages, floating-rate mortgages, hybrid adjustable mortgages, developer-linked installment loans, and subsidized housing loans. Recently, floating-rate mortgages have a dominant market share due to factors such as banking funding structures, interest rate pass-through mechanisms, and borrower acceptance of variable installment payments. Vietnamese banks primarily mobilize short- to medium-term deposits, encouraging mortgage pricing linked to reference lending rates rather than long-term fixed structures. Borrowers prioritize initial affordability and loan accessibility over rate stability, reinforcing floating-rate adoption. Developer-linked installment loans are growing but typically convert into floating mortgages after project completion. Fixed-rate products remain limited due to interest rate volatility and funding mismatch risks for lenders. Floating-rate mortgages therefore dominate Vietnam’s housing finance lending portfolios.

Competitive Landscape

Vietnam’s home finance sector is highly bank-centric, dominated by state-owned and large private commercial banks with nationwide branch networks and retail lending platforms. Mortgage origination is often integrated with developer partnerships and salaried borrower payroll relationships, reinforcing scale advantages of major banks. Competition is intensifying through digital loan processing and preferential mortgage packages tied to residential projects, while smaller banks focus on niche borrower segments and regional markets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio Focus |

| Vietcombank | 1963 | Hanoi | ~ | ~ | ~ | ~ | ~ |

| BIDV | 1957 | Hanoi | ~ | ~ | ~ | ~ | ~ |

| VietinBank | 1988 | Hanoi | ~ | ~ | ~ | ~ | ~ |

| Techcombank | 1993 | Hanoi | ~ | ~ | ~ | ~ | ~ |

| VPBank | 1993 | Hanoi | ~ | ~ | ~ | ~ | ~ |

Vietnam Home Finance Market Analysis

Growth Drivers

Urbanization and expanding middle class homeownership demand

Vietnam’s sustained urban migration and income growth are structurally increasing demand for financed housing ownership across metropolitan regions. Rising salaried employment in manufacturing, services, and technology sectors is expanding borrower eligibility for formal mortgage lending programs. Condominium development aligned with urban planning provides standardized collateral suitable for bank mortgage underwriting. Cultural preference for homeownership encourages households to leverage long-term credit to secure residential assets. Banking sector strategy is shifting toward retail lending to diversify revenue beyond corporate credit exposure. Government housing policies promoting ownership access reinforce mortgage demand across emerging urban populations. Household formation among younger professionals is increasing demand for financed apartments near employment centers. Mortgage tenors extending beyond fifteen years improve affordability for middle-income borrowers entering housing markets. Property developers collaborate with banks to provide pre-approved financing, accelerating loan origination volumes. These structural urbanization and income dynamics collectively drive expansion of Vietnam’s home finance market.

Banking sector retail credit expansion and mortgage product innovation

Vietnamese banks are strategically expanding retail loan portfolios to capture stable interest income and diversify asset risk. Mortgages represent secured long-term lending with lower default risk compared to unsecured consumer credit. Banks are introducing preferential interest packages, flexible repayment structures, and grace periods to attract homebuyers. Digital loan application and approval platforms reduce processing time and enhance borrower accessibility. Integration of mortgage financing with residential project sales pipelines enables large-scale loan origination tied to developer partnerships. Competitive pressure among banks is improving mortgage affordability and customer service standards. Payroll-linked lending programs leverage employer relationships to assess borrower creditworthiness efficiently. Risk management frameworks and property valuation systems are strengthening mortgage underwriting capacity. Expansion of branch and digital distribution networks increases geographic reach of housing loans. These banking sector strategies are reinforcing sustained growth in Vietnam’s home finance lending volumes.

Market Challenges

Property market volatility and developer project risks

Vietnam’s home finance sector is closely linked to the real estate development cycle, exposing mortgage portfolios to property market fluctuations. Delays or legal issues in residential projects can affect collateral validity and borrower repayment behavior. Oversupply in certain condominium segments can depress property values underlying mortgage security. Regulatory scrutiny of developer financing structures may constrain project-linked mortgage growth. Borrowers purchasing presale units face completion and title risks affecting loan disbursement timelines. Market downturns reduce transaction volumes, slowing mortgage origination pipelines for banks. Concentration of lending toward urban condominium projects increases systemic exposure to real estate cycles. Liquidity stress among developers can cascade into housing supply disruptions and borrower uncertainty. These real estate market dependencies create cyclical risk for Vietnam’s home finance sector stability.

Interest rate sensitivity and funding mismatch in mortgage lending

Vietnamese banks primarily fund lending through short-term deposits, creating maturity mismatches when issuing long-term mortgages. Interest rate fluctuations directly affect floating mortgage installments, increasing borrower repayment risk during tightening cycles. Limited availability of long-term fixed funding instruments constrains stable mortgage pricing structures. Rising funding costs can compress bank margins or reduce mortgage affordability for borrowers. Household income variability heightens sensitivity to installment increases under floating-rate loans. Lack of secondary mortgage markets restricts risk transfer and liquidity management for lenders. Macroeconomic monetary tightening can sharply reduce housing credit growth. These funding and interest rate dynamics challenge sustainable expansion of Vietnam’s mortgage lending ecosystem.

Opportunities

Affordable housing finance and government supported lending programs

Vietnam’s growing urban population includes large segments of lower-income households underserved by formal housing finance. Expansion of subsidized mortgage schemes and public housing credit programs can widen homeownership access. Partnerships between government agencies, developers, and banks can enable structured affordable housing finance models. Standardized underwriting for smaller loan sizes can reduce administrative costs and improve inclusion. Development of social housing supply aligned with financing availability can stimulate mortgage penetration beyond affluent buyers. International development finance institutions may support housing credit frameworks and guarantee schemes. Financial inclusion initiatives can integrate informal workers into mortgage eligibility assessments. Affordable housing finance thus represents a major untapped growth avenue within Vietnam’s home finance market.

Digital mortgage ecosystems and alternative credit assessment models

Adoption of digital identity, income verification, and property data platforms can transform mortgage origination efficiency in Vietnam. Automated underwriting using alternative credit data can expand eligibility beyond formally salaried borrowers. Integration with property registries and developer systems can streamline loan processing and collateral validation. Mobile banking channels enable borrower engagement and repayment management across loan lifecycles. Data analytics can improve risk pricing and portfolio monitoring for lenders. Digital mortgage marketplaces can enhance transparency and competition across loan products. Reduced processing costs enable banks to serve smaller borrowers profitably. Technology-enabled lending therefore offers significant scalability for Vietnam’s home finance market expansion.

Future Outlook

Vietnam’s home finance market is expected to expand steadily as urban housing demand, condominium development, and retail banking penetration increase. Digital mortgage platforms and affordable housing programs will broaden borrower access across income segments. Regulatory strengthening of property ownership and lending frameworks will enhance market stability. Rising household incomes and urbanization will sustain long-term mortgage demand, supporting continued growth in Vietnam’s housing finance ecosystem.

Major Players

- Vietcombank

- BIDV

- VietinBank

- Techcombank

- VPBank

- ACB

- Sacombank

- MB Bank

- HD Bank

- SHB

- TP Bank

- OCB

- LienVietPostBank

- Eximbank

- VIB

Key Target Audience

- Commercial banks

- Housing finance institutions

- Real estate developers

- Mortgage lenders

- Investments and venture capitalist firms

- Government and regulatory bodies

- Property investment firms

- Fintech lending platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables including mortgage outstanding credit, housing demand, borrower demographics, and property supply dynamics were identified from central bank credit data and housing statistics. Lending structures, interest frameworks, and collateral types were mapped to define the market scope.

Step 2: Market Analysis and Construction

The home finance ecosystem was constructed by analyzing mortgage issuance across banks, property types, and loan structures. Segmentation and competitive positioning were derived from banking disclosures and housing transaction patterns. Market size alignment ensured consistency with residential credit data.

Step 3: Hypothesis Validation and Expert Consultation

Insights were validated through triangulation with housing finance trends, bank lending data, and property market indicators. Financial sector expertise informed borrower behavior, lending risk, and institutional strategies shaping Vietnam’s mortgage market.

Step 4: Research Synthesis and Final Output

Quantitative credit data and qualitative housing market dynamics were synthesized into market sizing, segmentation, and strategic analysis. Drivers, challenges, and opportunities were assessed against macroeconomic and urbanization trends to produce the final Vietnam home finance market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Urbanization and Housing Demand Expansion

Rising Middle-Class Income Levels

Government Housing Development Programs - Market Challenges

High Property Price to Income Ratios

Credit Risk and Informal Income Verification

Limited Long-Term Funding Sources - Market Opportunities

Affordable Housing Finance Expansion

Digital Mortgage Origination Platforms

Green and Energy-Efficient Home Financing - Trends

Shift Toward Longer Tenor Mortgages

Bank-Developer Financing Partnerships - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Mortgage Loans for Primary Residences

Mortgage Loans for Secondary Homes

Home Equity Loans

Construction & Self-Build Financing

Refinancing & Balance Transfer Loans - By Platform Type (In Value%)

State-Owned Commercial Banks

Joint-Stock Commercial Banks

Housing Finance Companies

Digital Lending Platforms

Developer-Linked Financing Channels - By Fitment Type (In Value%)

New Purchase Financing

Resale Property Financing

Under-Construction Property Financing

Land Purchase Financing - By End User Segment (In Value%)

Urban Salaried Households

Self-Employed Borrowers

Rural Migrant Homebuyers

- Market Share Analysis

- Cross Comparison Parameters (Loan Tenor, Interest Rate Type, Loan-to-Value Ratio, Approval Turnaround Time, Developer Tie-Ups)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Vietcombank

BIDV

VietinBank

Techcombank

VPBank

Asia Commercial Bank

Sacombank

MB Bank

VIB

HDBank

TPBank

LienVietPostBank

SHB

OCB

Home Credit Vietnam

- Increasing First-Time Homebuyer Demand in Cities

- Growing Mortgage Adoption Among Young Families

- Rising Investor Activity in Urban Apartments

- Demand for Flexible Financing Among Informal Earners

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now