Download PDF

Download PDF Download PDF

Download PDFMarket Overview

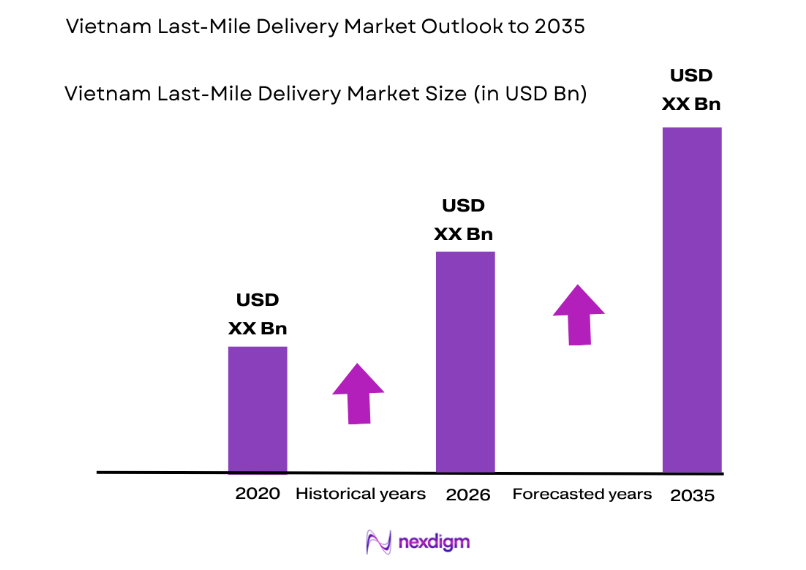

Based on a recent historical assessment, the Vietnam Last-Mile Delivery market generated approximately USD ~ billion in revenue, driven primarily by the rapid expansion of digital commerce platforms and increasing urban parcel shipments. According to Vietnam’s Ministry of Industry and Trade and the Vietnam E-commerce and Digital Economy Agency, the national e-commerce sector generated more than USD ~ billion in online retail sales, producing substantial parcel volumes requiring fast doorstep delivery. Logistics providers continue expanding courier fleets, automated sorting centers, and urban distribution hubs.

Major last-mile delivery operations are concentrated in Ho Chi Minh City, Hanoi, Da Nang, and Hai Phong where dense urban populations and large retail ecosystems create high parcel delivery demand. Ho Chi Minh City functions as the primary e-commerce logistics hub due to its extensive warehouse infrastructure and proximity to manufacturing clusters in southern industrial zones. Hanoi serves as the administrative and distribution center for northern Vietnam, while Da Nang and Hai Phong support regional delivery networks due to their port connectivity and growing consumer markets.

Market Segmentation

By Delivery Mode

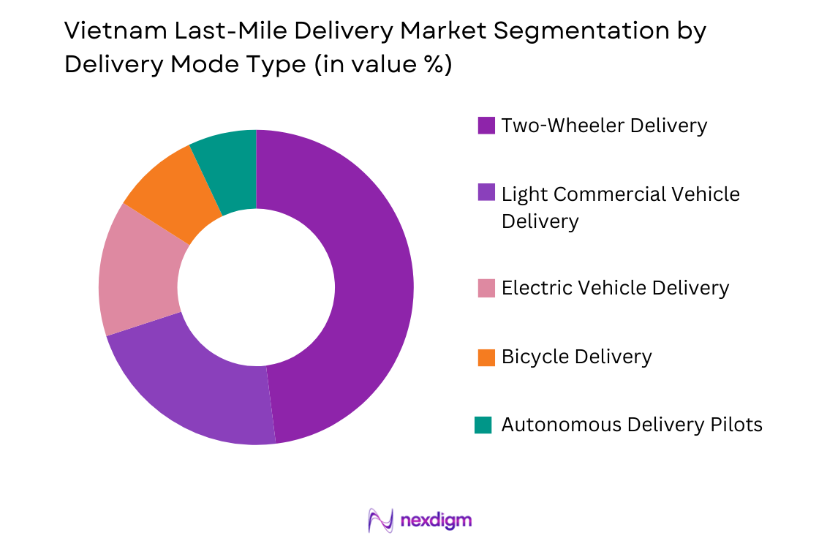

Vietnam Last-Mile Delivery market is segmented by product type into two-wheeler delivery, light commercial vehicle delivery, electric vehicle delivery, bicycle delivery, and autonomous delivery pilots. Recently, two-wheeler delivery has a dominant market share due to Vietnam’s dense urban road networks and the widespread use of motorcycles as primary transportation. Delivery companies rely heavily on motorcycle fleets because they navigate congested urban streets efficiently and enable rapid parcel distribution across residential areas and commercial districts. E-commerce platforms and food delivery applications depend on motorcycle-based courier fleets to complete high-volume deliveries within short timeframes. Lower vehicle acquisition costs, flexible fleet scaling, and the availability of gig-economy drivers further support the widespread adoption of two-wheeler delivery across Vietnam’s last-mile logistics ecosystem.

By End-Use Sector

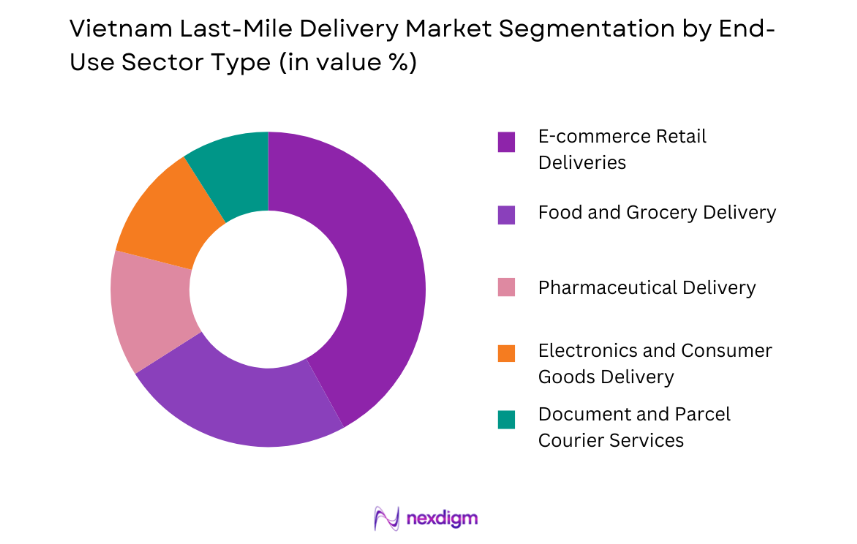

Vietnam Last-Mile Delivery market is segmented by end-use sector into e-commerce retail deliveries, food and grocery delivery, pharmaceutical delivery, electronics and consumer goods delivery, and document and parcel courier services. Recently, e-commerce retail deliveries have a dominant market share due to rapid expansion of digital marketplaces and increasing online shopping activity across Vietnam’s urban population. Online platforms such as Shopee, Lazada, and Tiki generate substantial daily order volumes that require efficient parcel distribution networks connecting fulfillment warehouses with residential customers. Logistics providers operate large courier fleets and automated parcel sorting hubs designed to process high shipment volumes efficiently. The convenience of doorstep delivery combined with expanding mobile payment adoption continues strengthening demand for e-commerce logistics services.

Competitive Landscape

The Vietnam Last-Mile Delivery market features a competitive landscape composed of domestic courier companies, regional logistics operators, and global parcel delivery providers. Rapid growth in e-commerce has intensified competition among logistics firms seeking to expand urban delivery networks and automated parcel sorting infrastructure. Large domestic logistics providers dominate nationwide delivery networks, while international logistics companies leverage advanced supply chain technologies and integrated cross-border logistics services to compete in high-value segments such as electronics distribution and international parcel delivery.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet Size |

| Viettel Post | 1997 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| Vietnam Post | 2005 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| Giao Hang Nhanh | 2012 | Vietnam | ~ | ~ | ~ | ~ | ~ |

| Ninja Van | 2014 | Singapore | ~ | ~ | ~ | ~ | ~ |

| DHL eCommerce | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

Vietnam Last-Mile Delivery Market Analysis

Growth Drivers

Rapid Expansion of E-commerce Platforms and Digital Retail Logistics Networks

Rapid expansion of digital commerce platforms significantly strengthens demand for last-mile delivery services across Vietnam’s logistics ecosystem. Online retail platforms including Shopee, Lazada, and Tiki generate high parcel shipment volumes requiring efficient courier networks capable of delivering orders to millions of consumers across urban and suburban areas. Consumers increasingly prefer home delivery for electronics, fashion products, groceries, and household goods purchased through mobile commerce applications. Logistics providers therefore invest heavily in automated parcel sorting centers, advanced warehouse management systems, and urban distribution hubs designed to process large shipment volumes efficiently. Technology integration allows companies to track parcel movements in real time while optimizing delivery routes to reduce transportation delays. Retail companies increasingly partner with third-party logistics providers capable of managing complex delivery operations and reverse logistics handling for returned products. Growing smartphone penetration and digital payment adoption enable a larger share of Vietnam’s population to participate in online retail transactions. Logistics providers also deploy predictive analytics platforms that forecast parcel demand and allocate delivery fleet capacity accordingly across metropolitan regions. As e-commerce adoption continues expanding across Vietnam’s digital economy, last-mile delivery services remain essential infrastructure supporting online retail supply chains.

High Urban Population Density Supporting Efficient Delivery Networks

High urban population density within Vietnam’s major metropolitan regions creates favorable conditions for efficient last-mile delivery operations across the logistics sector. Cities such as Ho Chi Minh City and Hanoi contain large residential populations concentrated within relatively compact geographic areas, enabling logistics providers to complete multiple deliveries within short travel distances. This urban density significantly improves courier productivity and allows companies to reduce delivery times while lowering operational costs associated with fuel consumption and transportation distance. Retail businesses and e-commerce platforms depend on these densely populated urban markets to maintain fast shipping services that meet consumer expectations for same-day or next-day delivery. Logistics providers therefore establish micro-fulfillment centers and urban parcel distribution hubs located close to residential neighborhoods. These facilities allow companies to process incoming shipments rapidly and dispatch courier fleets capable of delivering parcels within a few hours after order confirmation. Digital route optimization software and mobile courier applications further improve delivery efficiency by directing drivers through the most efficient transportation routes. High levels of smartphone usage also allow customers to track deliveries and coordinate order receipt through mobile applications. As Vietnam’s urban population continues expanding across major cities, dense metropolitan environments will continue supporting the growth of efficient last-mile delivery networks.

Market Challenges

Urban Traffic Congestion and Delivery Infrastructure Constraints

Urban traffic congestion represents a major operational challenge affecting efficiency within Vietnam’s last-mile delivery logistics sector. Major cities such as Ho Chi Minh City and Hanoi experience heavy daily traffic volumes that significantly slow transportation movement and increase delivery times across densely populated urban districts. Delivery drivers frequently encounter road congestion, limited parking availability, and narrow streets that complicate parcel drop-off operations. These logistical obstacles increase operational costs for courier companies as drivers spend more time completing individual deliveries across congested urban areas. Delays caused by traffic congestion also create difficulties for logistics providers attempting to meet strict delivery time commitments promised by e-commerce platforms and retail customers. Logistics companies attempt to mitigate these issues by deploying motorcycle delivery fleets capable of navigating narrow streets and congested road networks more effectively than larger vehicles. However, increasing parcel shipment volumes generated by the expanding digital commerce ecosystem continue intensifying pressure on urban transportation infrastructure. Limited availability of dedicated logistics loading zones within city centers further complicates efficient delivery operations. As parcel shipment volumes continue increasing across metropolitan areas, traffic congestion will remain a significant operational challenge for logistics providers attempting to maintain rapid delivery services.

Fragmented Logistics Networks and Limited Automation Adoption

Fragmented logistics infrastructure across Vietnam’s delivery ecosystem creates operational inefficiencies that restrict scalability within the last-mile logistics market. Many domestic courier companies operate regional delivery networks without fully integrated digital logistics platforms capable of coordinating shipments nationwide. This fragmentation leads to inconsistent service quality, limited shipment visibility, and operational inefficiencies when managing large parcel volumes generated by e-commerce platforms. Smaller logistics operators frequently rely on manual sorting processes and outdated warehouse infrastructure that slows parcel processing and increases labor costs. Limited adoption of automated parcel sorting systems and integrated warehouse management technologies further constrains the ability of logistics companies to scale operations efficiently. Without advanced logistics technologies capable of coordinating real-time delivery routing and shipment tracking, courier networks face challenges managing fluctuating parcel demand during peak online shopping periods. Large logistics providers increasingly invest in automated distribution centers and digital supply chain platforms designed to improve operational efficiency. However, many smaller logistics companies still lack the capital and technological resources necessary to modernize their infrastructure. Improving integration across logistics networks and expanding automation adoption remain critical for strengthening Vietnam’s last-mile delivery infrastructure.

Opportunities

Development of Smart Logistics Technologies and Automated Delivery Systems

Development of smart logistics technologies presents significant growth opportunities for companies operating within Vietnam’s last-mile delivery market. Logistics providers are increasingly adopting advanced technologies such as artificial intelligence powered route optimization systems, automated parcel sorting facilities, and digital fleet management platforms designed to improve operational efficiency. These technologies enable logistics companies to process higher parcel volumes while reducing manual labor requirements and delivery times. Automated parcel sorting systems significantly accelerate shipment processing within distribution centers, allowing companies to dispatch parcels more quickly to delivery drivers. Digital logistics management platforms also enable real-time shipment tracking, providing customers with accurate delivery updates through mobile applications. Emerging innovations including autonomous delivery robots, drone delivery pilots, and electric delivery vehicles also present long-term opportunities for improving delivery efficiency and reducing transportation costs. Logistics companies investing in smart logistics technologies will gain competitive advantages by improving delivery speed, operational efficiency, and customer service quality. As Vietnam’s digital economy continues expanding and parcel shipment volumes increase, technological innovation will become a key driver shaping the future of last-mile delivery logistics.

Expansion of On-Demand Delivery Services and Quick Commerce Platforms

Expansion of on-demand delivery services and quick commerce platforms represents another major opportunity within Vietnam’s last-mile delivery market. Urban consumers increasingly demand rapid delivery of groceries, restaurant meals, pharmaceuticals, and convenience products ordered through mobile applications. Food delivery platforms and quick commerce startups rely on extensive courier networks capable of delivering products within short timeframes directly to residential customers. This shift toward immediate delivery expectations creates strong demand for logistics providers capable of operating real-time dispatch systems and flexible delivery fleets. Companies are therefore establishing urban micro-fulfillment centers and neighborhood distribution hubs designed to support rapid delivery operations. Digital platforms connecting customers, retailers, and delivery drivers enable companies to process orders quickly and allocate delivery resources efficiently. Quick commerce models also encourage retailers to maintain smaller inventory locations located close to urban customers, reducing delivery distance and improving order fulfillment speed. As mobile commerce adoption and digital payment usage continue increasing across Vietnam’s urban population, on-demand delivery services will generate significant new opportunities for logistics providers specializing in last-mile distribution.

Future Outlook

Vietnam’s last-mile delivery market is expected to expand significantly as e-commerce activity, urban consumption, and digital retail ecosystems continue developing. Logistics providers are expected to invest in automated parcel sorting infrastructure, smart delivery technologies, and electric courier fleets designed to improve operational efficiency. Government initiatives supporting digital economy growth and logistics infrastructure modernization will strengthen the delivery ecosystem. Rising demand for rapid delivery services, quick commerce platforms, and integrated logistics networks will continue driving expansion of last-mile delivery services across Vietnam’s urban markets.

Major Players

- Viettel Post

- Vietnam Post

- Giao Hang Nhanh

- Ninja Van

- DHL eCommerce

- J&T Express

- GrabExpress

- AhaMove

- BEST Express Vietnam

- Kerry Express Vietnam

- Lazada Logistics

- Shopee Express

- FedEx Express Vietnam

- UPS Vietnam

- Lalamove Vietnam

Key Target Audience

- E-commerce retailers

- Logistics and courier service providers

- Retail supermarket chains

- Food delivery platform companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Consumer electronics manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the Vietnam Last-Mile Delivery market were identified through analysis of e-commerce parcel volumes, courier fleet capacity, urban logistics infrastructure, and consumer purchasing patterns across digital retail platforms.

Step 2: Market Analysis and Construction

Market structure was developed by analyzing logistics networks, delivery technologies, and operational models used by courier companies. Data from government trade agencies, e-commerce platforms, and logistics industry reports were incorporated.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through consultation with logistics operators, supply chain specialists, and e-commerce distribution experts who provided insights into delivery demand trends and operational challenges.

Step 4: Research Synthesis and Final Output

All research insights were synthesized to develop a comprehensive analytical framework evaluating Vietnam’s last-mile delivery ecosystem, integrating quantitative data, infrastructure analysis, and logistics industry developments.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Growth of E-commerce and Online Retail

Urban Population Density Supporting Efficient Delivery Networks

Adoption of Digital Tracking and Route Optimization Technologies - Market Challenges

High Capital and Operational Costs for Fleet and Infrastructure

Traffic Congestion and Urban Delivery Constraints

Regulatory Compliance for Urban Logistics Operations - Market Opportunities

Expansion of Electric Vehicle and Sustainable Delivery Fleets

Partnerships Between Retailers and Specialized Last-Mile Providers

Integration of AI for Predictive Delivery and Demand Planning - Trends

Increased Adoption of Autonomous Delivery Vehicles

Integration of Smart Lockers and Micro-Distribution Hubs - Government Regulations

Urban Transport Licensing and Compliance

Data Privacy and Consumer Protection Laws

Incentives for Green and Sustainable Logistics - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Sorting and Handling Systems

Delivery Fleet Management Platforms

Route Optimization and Tracking Software

Automated Locker Systems

Temperature-Controlled Delivery Solutions - By Platform Type (In Value%)

Land Delivery Platforms

Air Delivery Platforms

Electric Vehicle Delivery Platforms

Integrated Urban Distribution Platforms - By Fitment Type (In Value%)

On-premise Delivery Solutions

Cloud-based Delivery Solutions

Hybrid Delivery Solutions

Modular Distribution Systems - By End User Segment (In Value%)

E-commerce Retailers

Food and Grocery Delivery Services

Logistics Service Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, End User Segment, Fleet Size, Technology Adoption, Geographic Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Ninja Van Vietnam

Vietnam Post Logistics

DHL eCommerce Vietnam

FedEx Vietnam

UPS Vietnam

GrabExpress Vietnam

Lalamove Vietnam

J&T Express Vietnam

Shopee Xpress Vietnam

Amazon Logistics Vietnam

Kerry Logistics Vietnam

SF Express Vietnam

Aramex Vietnam

DB Schenker Vietnam

Qxpress Vietnam

- E-commerce Retailers Expanding Same-Day and Express Delivery Options

- Food Delivery Platforms Increasing Last-Mile Service Reach

- Consumers Demanding Faster and Trackable Deliveries

- Retailers Outsourcing Delivery Operations to Specialized Providers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now