Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Vietnam’s online insurance market is valued at approximately USD ~ billion in digitally originated gross written premiums, based on a recent historical assessment of national insurance supervisory disclosures and insurer digital sales reporting. The market is driven by rapid digital adoption, expanding middle-class protection awareness, and mobile-first distribution through bancassurance platforms and standalone insurer apps. E-commerce integration and simplified micro-insurance products have accelerated online policy purchases across urban consumers seeking accessible and low-cost coverage.

Ho Chi Minh City and Hanoi dominate Vietnam’s online insurance activity due to concentration of digitally connected populations, insurer headquarters, and financial services ecosystems, while emerging growth is visible in Da Nang and Binh Duong linked to industrial employment and rising urban incomes. Strong fintech presence, smartphone penetration, and e-commerce usage reinforce metropolitan leadership. Younger digitally native consumers and bancassurance distribution partnerships explain sustained online insurance adoption in Vietnam’s major urban centers.

Market Segmentation

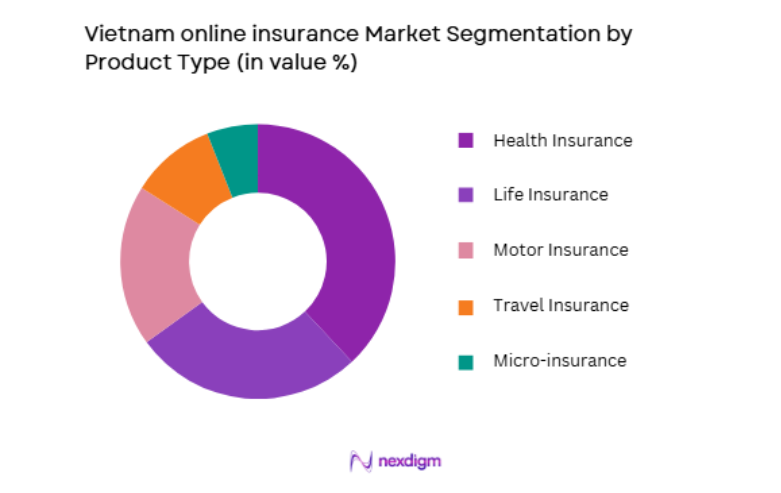

By Product Type

Vietnam Online Insurance market is segmented by product type into health insurance, life insurance, motor insurance, travel insurance, and micro-insurance. Recently, health insurance has a dominant market share due to factors such as rising healthcare cost awareness, pandemic-driven protection demand, and suitability for digital purchase through simplified underwriting. Short-term health and hospitalization products are easily standardized for online channels compared with complex life policies, enabling rapid digital distribution. Urban consumers prioritize health coverage due to increasing private healthcare utilization.

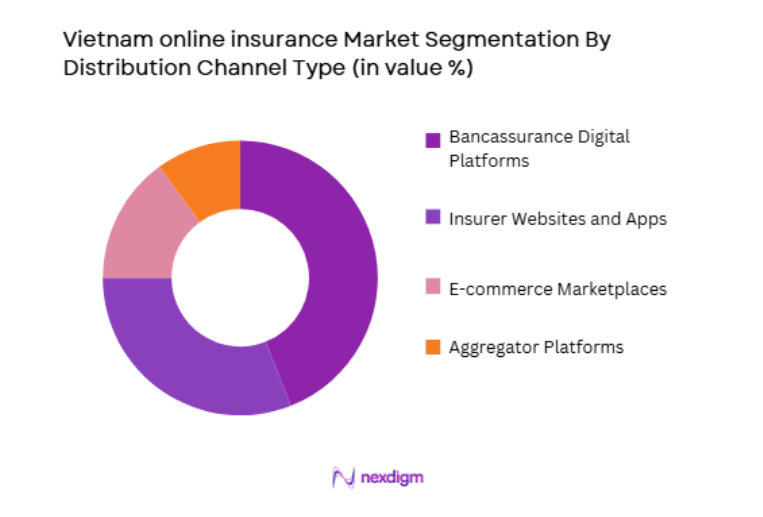

By Distribution Channel

Vietnam Online Insurance market is segmented by distribution channel into insurer websites and apps, bancassurance digital platforms, e-commerce marketplaces, and aggregator platforms. Recently, bancassurance digital platforms have a dominant market share due to factors such as existing banking customer bases, integrated payment infrastructure, and trust associated with bank-linked insurance offerings. Banks embed insurance purchase journeys within mobile banking apps, enabling seamless cross-selling to large user bases. Customer financial data availability supports targeted insurance recommendations and simplified onboarding. Regulatory encouragement of bancassurance partnerships has strengthened digital insurance distribution through banks.

Competitive Landscape

Vietnam’s online insurance market is moderately concentrated, with leading domestic insurers and international joint ventures leveraging bancassurance alliances and mobile platforms to scale digital policy sales. Banks play a central distribution role, shaping competitive positioning through exclusive partnerships. Insurers differentiate through app functionality, instant underwriting, and bundled digital protection products, while fintech entrants and aggregators intensify competition in standardized insurance categories.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Bancassurance Partner Strength |

| Bao Viet Insurance | 1964 | Hanoi | ~ | ~ | ~ | ~ | ~ |

| Prudential Vietnam | 1999 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ |

| Manulife Vietnam | 1999 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ |

| AIA Vietnam | 2000 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ |

| PVI Insurance | 1996 | Hanoi | ~ | ~ | ~ | ~ | ~ |

Vietnam Online Insurance Market Analysis

Growth Drivers

Rapid Smartphone Penetration and Mobile-First Financial Services Adoption

Vietnam’s widespread smartphone adoption and mobile internet usage are fundamentally transforming insurance distribution by enabling insurers and banks to deliver policy purchase, underwriting, and servicing entirely through digital channels accessible to a large and increasingly connected consumer base across urban and semi-urban regions. Mobile banking ecosystems with integrated financial services allow insurance cross-selling within familiar digital environments, lowering acquisition costs and simplifying customer onboarding. Younger demographics comfortable with app-based transactions show strong willingness to purchase insurance online without agent interaction. Insurers deploy instant underwriting algorithms and digital identity verification to enable real-time policy issuance on mobile platforms. Push notifications and personalized offers enhance engagement and retention. Mobile payment infrastructure supports seamless premium collection. Digital claims submission and tracking improve service experience. The ubiquity of smartphones is thus a foundational enabler expanding Vietnam’s online insurance market scale and accessibility.

Expansion of Bancassurance Partnerships Driving Digital Policy Distribution

Vietnam’s banking sector has rapidly expanded bancassurance alliances with insurers, leveraging extensive customer bases and trusted financial relationships to distribute insurance products through digital banking platforms, significantly accelerating online insurance adoption across retail consumers. Banks integrate insurance offerings within mobile apps, allowing customers to purchase policies during routine financial transactions. Customer financial data enables targeted cross-selling and risk-based product recommendations. Exclusive distribution agreements incentivize banks to prioritize partner insurers’ digital products. Regulatory acceptance of bancassurance models supports scaling of digital insurance sales. Banks’ credibility reduces consumer skepticism toward online insurance purchases. Integrated payment and auto-debit features simplify premium management. Digital onboarding within banking apps eliminates paperwork barriers. Bancassurance-led digitalization is therefore a central growth engine for Vietnam’s online insurance market.

Market Challenges

Low Insurance Literacy and Consumer Trust Barriers in Digital Channels

Despite increasing internet penetration, many Vietnamese consumers still have limited understanding of insurance products and coverage terms, creating hesitancy toward purchasing policies through online channels without human advisory support, which constrains the growth potential of purely digital insurance distribution models. Misconceptions about claim processes and coverage exclusions reduce willingness to transact digitally. Lack of personalized guidance in online environments can lead to product mismatch concerns. Consumers often prefer face-to-face explanations for long-term insurance commitments. Negative perceptions from historical mis-selling cases affect trust in digital offerings. Rural populations exhibit lower familiarity with online financial services. Complex life insurance structures are difficult to communicate digitally. Customer support limitations in digital channels hinder confidence. These literacy and trust barriers remain significant constraints on Vietnam’s online insurance market expansion.

Regulatory and Data Privacy Compliance Constraints on Digital Insurance Expansion

Vietnam’s evolving regulatory environment governing electronic transactions, data protection, and insurance distribution imposes compliance requirements that increase operational complexity and cost for insurers scaling online channels, potentially slowing innovation and market expansion in digital insurance services. Insurers must implement secure data storage and identity verification systems aligned with privacy regulations. Approval processes for new digital products can be lengthy. Cross-border data handling restrictions affect multinational insurers’ technology architectures. Consumer consent and cybersecurity requirements increase compliance overhead. Regulatory oversight of online marketing and sales practices requires monitoring systems. Smaller insurers face higher relative compliance burdens. Technology investment needed for regulatory adherence raises entry barriers. These regulatory dynamics shape operational challenges within Vietnam’s online insurance market.

Opportunities

Growth of Micro-Insurance and On-Demand Digital Protection Products

Vietnam’s large population of uninsured and underinsured consumers presents significant opportunity for insurers to expand online distribution of low-premium micro-insurance and short-duration protection products tailored to digital purchase behavior and affordability constraints across emerging middle-income and gig-economy segments. Mobile platforms enable cost-efficient distribution of bite-sized insurance policies with simplified coverage and instant issuance. Consumers can purchase event-based or short-term protection aligned with specific needs. Insurers can reach rural and informal workers lacking access to traditional agents. Partnerships with e-commerce and ride-hailing platforms enable contextual insurance offerings. Digital wallets support small-ticket premium payments. Government interest in financial inclusion supports micro-insurance expansion. Low product complexity suits digital communication. Micro-insurance thus represents a major growth avenue in Vietnam’s online insurance market.

Integration of Embedded Insurance within E-Commerce and Digital Ecosystems

Vietnam’s rapidly expanding digital commerce and platform economy creates strong opportunity for insurers to embed insurance products directly within online purchase journeys, enabling seamless contextual protection offerings across travel, electronics, logistics, and mobility transactions conducted through digital marketplaces and service platforms. Embedded insurance allows customers to add coverage during product or service purchase with minimal friction. E-commerce platforms provide large user bases and behavioral data for targeted insurance offers. Logistics and delivery services can bundle shipment protection. Travel booking platforms integrate trip insurance automatically. Digital ecosystems enable high-frequency micro-insurance transactions. Insurers gain scalable distribution without traditional sales costs. Platform partnerships enhance visibility and trust. Embedded insurance integration is therefore a transformative opportunity for Vietnam’s online insurance market.

Future Outlook

Vietnam’s online insurance market is expected to grow rapidly over the next five years driven by mobile-first distribution, bancassurance digitalization, and embedded insurance integration across e-commerce ecosystems. Regulatory clarity on digital transactions and data protection will support innovation. Expanding middle-class protection demand and micro-insurance adoption will broaden market reach. Technology-enabled underwriting and claims automation will enhance efficiency and customer experience. Digital financial inclusion policies will further accelerate online insurance penetration.

Major Players

- Bao Viet Insurance

- Prudential Vietnam

- Manulife Vietnam

- AIA Vietnam

- PVI Insurance

- FWD Vietnam

- Generali Vietnam

- Dai-ichi Life Vietnam

- Cathay Life Vietnam

- Hanwha Life Vietnam

- BIDV MetLife

- PTI Insurance

- MIC Insurance

- Liberty Insurance Vietnam

- Sun Life Vietnam

Key Target Audience

- Insurance companie

- Commercial banks

- Fintech platforms

- E-commerce platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Digital payment providers

- Telecommunications companies

Research Methodology

Step 1: Identification of Key Variables

Key variables including digital premium volume, product mix, distribution channels, consumer adoption patterns, and regulatory frameworks were identified. Data inputs were sourced from insurance supervisory statistics, insurer disclosures, and digital finance adoption indicators to establish Vietnam’s online insurance baseline.

Step 2: Market Analysis and Construction

Digital insurance sales were mapped across product and channel segments, linking bancassurance penetration and mobile adoption with premium generation. Insurer distribution structures and platform partnerships were integrated to construct market size and segmentation estimates.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on consumer digital behavior, insurance adoption barriers, and regulatory impact were validated against insurer strategies, banking distribution practices, and fintech ecosystem trends. Cross-verification ensured alignment with Vietnam’s digital finance environment.

Step 4: Research Synthesis and Final Output

Quantitative premium data and qualitative industry insights were synthesized into a structured market model covering size, segmentation, drivers, and competitive dynamics. Analytical integration ensured consistency with Vietnam’s insurance sector and digital economy evolution.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Smartphone Penetration and Digital Payment Adoption in Vietnam

Expansion of Insurtech and Embedded Insurance Ecosystems

Government Digitalization Policies and E-KYC Enablement - Market Challenges

Low Insurance Awareness and Trust in Online Channels

Regulatory Ambiguity in Digital-Only Insurance Distribution

Cybersecurity and Data Privacy Concerns in Insurtech Platforms - Market Opportunities

Growth of Microinsurance and Inclusive Digital Coverage

Partnerships Between Insurers and Super Apps

AI-Driven Underwriting and Personalized Policy Pricing - Trends

Shift Toward Embedded and On-Demand Insurance Products

Increasing Use of Mobile Wallets for Policy Purchase - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Online Life Insurance

Online Health Insurance

Online Motor Insurance

Online Travel Insurance

Online Microinsurance - By Platform Type (In Value%)

Insurer Direct Digital Platforms

Insurance Aggregator Marketplaces

Bancassurance Digital Channels

E-Commerce Embedded Insurance

Mobile Wallet Insurance Platforms - By Fitment Type (In Value%)

Standalone Digital Policies

Embedded Insurance Products

Subscription-Based Insurance

On-Demand Usage Insurance - By End User Segment (In Value%)

Urban Digital Consumers

SMEs and Microenterprises

Gig Economy Workers

- Market Share Analysis

- Cross Comparison Parameters (Distribution Channel, Product Breadth, Digital Onboarding, Pricing Model, Claims Automation Level, E-KYC Integration, Partner Ecosystem Depth, Mobile App Functionality)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bao Viet Insurance Digital

PVI Insurance Online

PTI Insurance Digital

Bao Minh Online

Manulife Vietnam Digital

Prudential Vietnam Online

AIA Vietnam Digital

FWD Vietnam Digital

Generali Vietnam Online

Liberty Vietnam Online

Chubb Vietnam Digital

MSIG Vietnam Online

Cathay Life Vietnam Digital

Hanwha Life Vietnam Digital

VietinBank Insurance Online

- Digital Adoption Among Young Urban Consumers

- Insurance Needs of Platform Economy Workers

- SME Demand for Low-Cost Digital Coverage

- Growing Acceptance of Mobile-Based Policy Servicing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now