Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Vietnam Oral Care Market is valued at USD ~ million, based on a five-year historical analysis, and is driven by population scale, urbanization, rising dental-health awareness, and higher disposable income. Vietnam’s population exceeded 101.1 million in the latest census update, while the urban population reached about 40.59 million, supporting higher purchase frequency across toothpaste, toothbrushes, mouthwash, whitening products, and sensitivity-care products. Market growth is also linked to stronger beauty-and-personal-care spending and premium oral hygiene adoption.

Ho Chi Minh City, Hanoi, Da Nang, Hai Phong, and Can Tho dominate Vietnam oral care demand because they concentrate higher-income households, pharmacy chains, supermarkets, hypermarkets, dental clinics, and e-commerce fulfillment networks. Ho Chi Minh City has more than 9 million residents, while Hanoi is estimated at around 8.5 million residents. Vietnam’s e-commerce market reached USD ~ billion, creating strong online visibility for whitening toothpaste, electric toothbrushes, and imported premium oral-care SKUs.

Market Segmentation

By Product Type

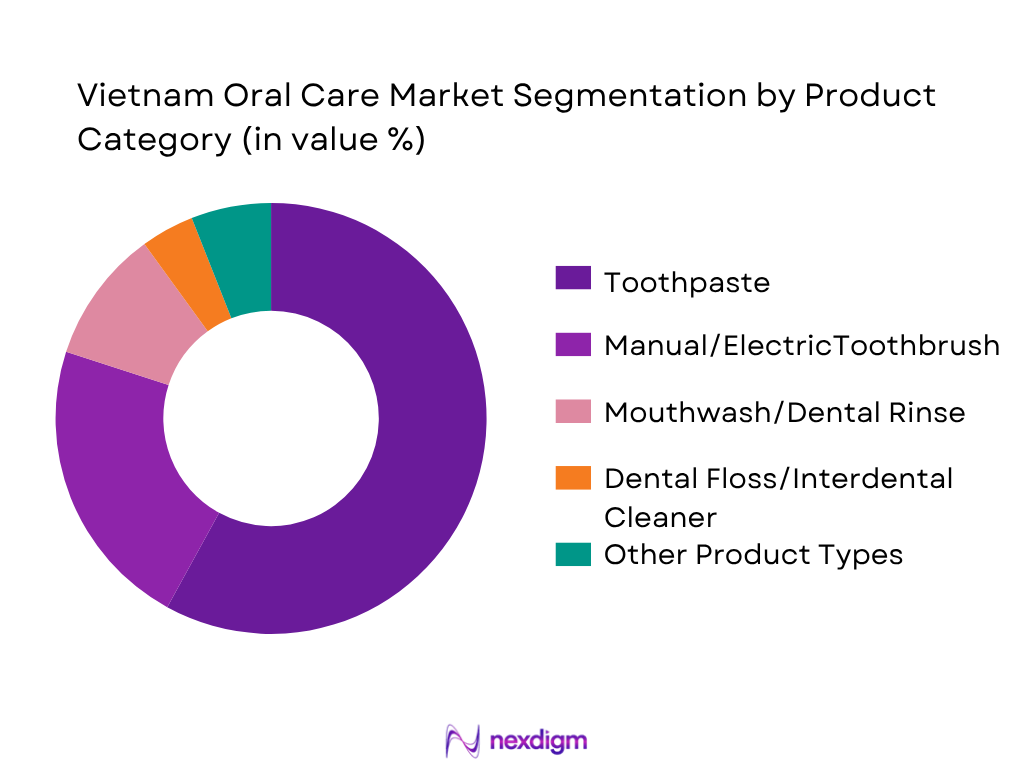

Vietnam Oral Care Market is segmented by product type into toothpaste, manual toothbrushes, electric toothbrushes, mouthwash/dental rinses, dental floss/interdental cleaners, tooth whiteners, denture care, and mouth fresheners. Toothpaste dominates the market because it is the most frequently purchased oral-care product, used daily across income groups and available in mass, herbal, whitening, cavity-protection, gum-care, and sensitivity variants. The segment benefits from deep penetration in traditional grocery stores, supermarkets, pharmacies, and e-commerce marketplaces. Toothbrushes form the second major product group, but replacement cycles are longer than toothpaste purchase cycles. Mouthwash is growing faster in urban areas because consumers increasingly associate it with fresh breath, gum health, and post-brushing hygiene.

By Distribution Channel

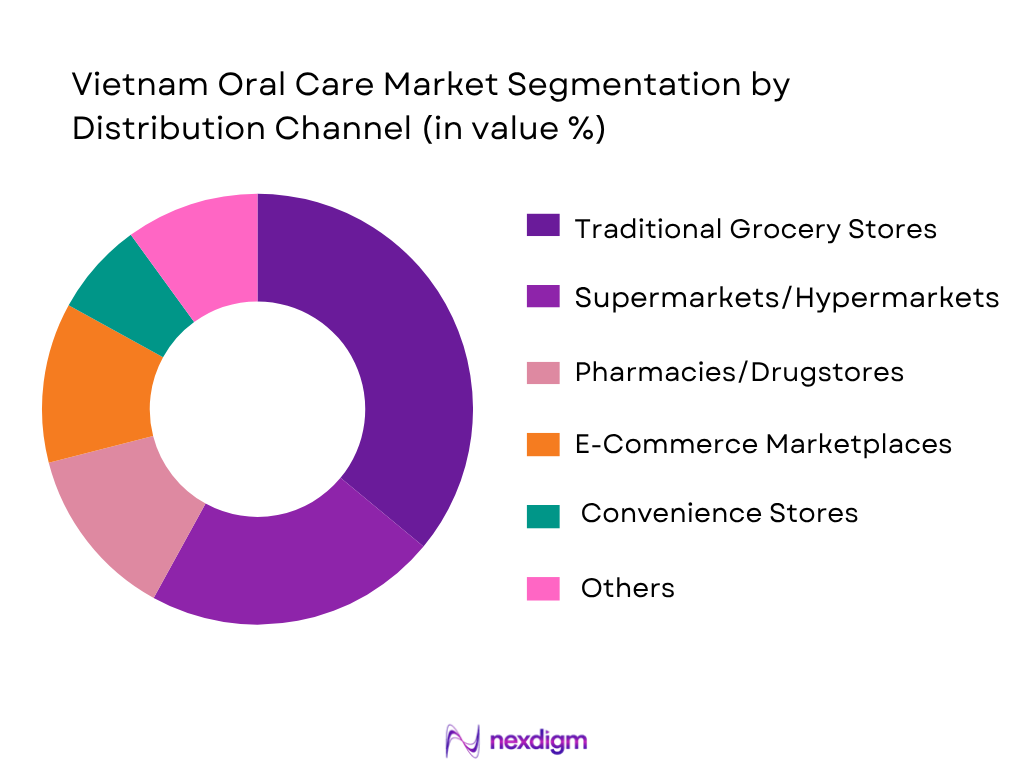

Vietnam Oral Care Market is segmented by distribution channel into traditional grocery stores, supermarkets/hypermarkets, convenience stores, pharmacies/drugstores, health and beauty chains, dental clinics, e-commerce marketplaces, and brand-owned online stores. Traditional grocery stores hold the dominant share because toothpaste and manual toothbrushes remain household essentials purchased alongside daily FMCG products, particularly in suburban and rural provinces. However, modern trade and e-commerce are reshaping premium oral care. Supermarkets and hypermarkets support family packs, bundled SKUs, and promotional buying, while pharmacies and health-and-beauty chains are important for sensitivity toothpaste, gum-care products, and mouthwash. E-commerce marketplaces are expanding rapidly because consumers compare prices, read product reviews, and access imported Korean, Japanese, European, and U.S. oral-care brands. Vietnam’s online retail scale strengthens visibility for electric toothbrushes, whitening kits, and specialized oral-care products.

Competitive Landscape

The Vietnam Oral Care Market is led by multinational FMCG and healthcare companies with strong toothpaste, toothbrush, mouthwash, and specialist-care portfolios. Unilever’s P/S and Closeup, Colgate-Palmolive’s Colgate, Haleon’s Sensodyne, Johnson & Johnson’s Listerine, and Oral-B are prominent across mass, youth, sensitivity, mouthwash, and toothbrush segments. Competition is shaped by SKU breadth, dentist endorsement, whitening claims, herbal/natural formulations, price promotions, pharmacy access, and online marketplace visibility.

| Company / Brand | Establishment Year | Headquarters | Core Vietnam Oral-Care Categories | Key Benefit Positioning | Channel Strength | Premiumization Focus | Local Relevance | Competitive Edge |

| Unilever / P/S, Closeup | 1929 | London, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Colgate-Palmolive / Colgate | 1806 | New York, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Haleon / Sensodyne | 2022 | Weybridge, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Johnson & Johnson / Listerine | 1886 | New Brunswick, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Procter & Gamble / Oral-B | 1837 | Cincinnati, USA | ~ | ~ | ~ | ~ | ~ | ~ |

Vietnam Oral Care Market Analysis

Growth Drivers

Urbanization

Vietnam’s oral care demand is strongly supported by urban concentration because toothpaste, mouthwash, whitening products, and electric toothbrushes gain faster traction in cities with dense retail networks, pharmacies, dental clinics, and e-commerce delivery. The World Bank records Vietnam’s total population at 100,987,686 people and urban population at about 40.2% of total population, creating a large city-based consumer base for modern oral hygiene products. Urban households also have stronger access to supermarkets, convenience stores, pharmacies, and health-and-beauty chains, which improves availability of premium sensitivity toothpaste, kids’ fluoride toothpaste, alcohol-free mouthwash, and branded toothbrushes. Vietnam’s internet penetration reached 84% of population, strengthening product discovery through Shopee, Lazada, TikTok Shop, and brand-led online campaigns. Retail infrastructure further supports oral care because Vietnam’s total retail sales of consumer goods and services reached VND 6.39 quadrillion, while retail sales of goods alone reached VND 4.92 quadrillion, expanding the FMCG base where oral care is purchased as a recurring household essential. .

Disposable Income

Disposable-income growth is a direct driver for Vietnam oral care because consumers move from basic cavity-protection toothpaste toward whitening, gum-care, sensitivity-care, herbal, and children’s specialist products as household budgets improve. Vietnam’s GDP per capita reached USD 4,717.3, while GDP reached USD 476.39 billion, showing a larger consumption economy for branded personal-care products. The General Statistics Office-linked living standards data reported average monthly income per capita at VND 5.4 million, with urban income at VND 6.9 million and rural income at VND 4.5 million. This income gap is important for oral care because urban consumers are more likely to buy premium toothpaste, mouthwash, electric toothbrushes, and imported products, while rural households remain oriented toward mass toothpaste and manual toothbrushes. Healthcare expenditure also rose, with spending per person seeking medical care reaching VND 3.5 million, reinforcing consumer willingness to spend on preventive health-adjacent categories such as oral hygiene.

Market Challenges

Price Sensitivity

Price sensitivity remains a structural challenge in Vietnam oral care because the market must serve both premium urban households and lower-income rural households. The 2024 living standards data shows monthly income per capita at VND 6.9 million in urban areas and VND 4.5 million in rural areas, creating different affordability thresholds for toothpaste, toothbrushes, mouthwash, floss, and electric toothbrushes. Regional income divergence is also material: the Southeast recorded nearly VND 7.1 million monthly income per person, while the Northern midlands and mountainous areas recorded just under VND 3.8 million. For oral care companies, this affects pack-size strategy, promotional intensity, and channel prioritization. Family tubes, small tubes, and multipacks become necessary to defend penetration, while premium SKUs need pharmacy, modern trade, and e-commerce targeting. Average monthly expenditure per capita reached almost VND 3 million, leaving limited room for higher-priced non-essential oral-care add-ons such as floss, whitening strips, and electric toothbrush heads.

Counterfeit Risk

Counterfeit and unclear-origin goods create a trust barrier for Vietnam oral care, especially for imported toothpaste, whitening products, electric toothbrushes, mouthwash, and dentist-recommended premium SKUs sold through fragmented online and offline channels. Vietnam’s government approved an action plan requiring enforcement agencies to use modern technology, digital tools, and databases to strengthen market monitoring, while also requiring major e-commerce platforms, social networks, and media outlets to commit against trading or advertising counterfeit, substandard, unclear-origin, or IP-infringing goods. This is directly relevant to oral care because the category relies on safety-sensitive claims such as fluoride protection, sensitivity relief, whitening efficacy, antibacterial mouthwash action, and children’s oral care suitability. The Ministry of Health also moved to strengthen cosmetics management and product traceability through a national cosmetics database, after enforcement cases involving mandatory product information dossiers. For branded oral-care companies, counterfeit risk raises the need for channel control, QR traceability, authorized seller programs, and stronger marketplace monitoring.

Opportunities

Premium Sensitivity Care

Premium sensitivity care has strong future potential in Vietnam oral care because the consumer base is large, urbanizing, and increasingly health-aware. The World Bank records Vietnam’s population at 100,987,686 people, providing scale for specialist toothpaste, gum-care products, enamel-protection products, and dentist-recommended oral-care ranges. Healthcare spending also supports the premium-care thesis: average healthcare spending per person seeking medical care reached VND 3.5 million, while outpatient spending reached VND 1.8 million. These figures indicate that households are allocating more money to health-related needs, creating room for preventive oral-care positioning. The opportunity is especially strong in Hanoi, Ho Chi Minh City, Da Nang, Hai Phong, and Can Tho, where pharmacies, dental clinics, supermarkets, and e-commerce channels can support higher-value SKUs. Vietnam’s National Oral Health Survey initiative is also collecting clinical oral-exam data, social-survey data, and fluoride-analysis data, which should sharpen future policy and consumer education around tooth decay, gum disease, and preventive care.

Kids’ Oral Care

Kids’ oral care is a high-potential opportunity in Vietnam because the child population is large and oral-health policy attention is increasing. World Bank data records Vietnam’s population aged 0–14 at 23,453,385 people, creating a sizeable addressable base for children’s fluoride toothpaste, soft-bristle toothbrushes, character-led packs, school oral-hygiene programs, and parent-focused preventive education. UNFPA also records Vietnam’s total population at 101,600,000 people, confirming continued national scale for family oral-care categories. The National Oral Health Survey is targeting more than 10,000 participants and includes clinical examinations, lifestyle surveys, and water-fluoride analysis, which is relevant for children’s caries prevention and policy-backed fluoride guidance. For oral-care companies, this creates opportunity to build pediatric dentist partnerships, school-channel education, age-specific toothpaste ranges, low-abrasion formulations, and parent-trust messaging. Demand is likely to be strongest where household education spending and healthcare spending are already rising, as families connect children’s oral hygiene with broader health and wellbeing.

Future Outlook

The Vietnam Oral Care Market is forecast to grow at a 7.18% CAGR for the 2026–2035 period, using the latest Vietnam-specific published growth benchmark as the base trajectory. Growth will be supported by rising preventive dental-care awareness, expansion of pharmacies and modern retail, higher e-commerce penetration, and premium product adoption. Whitening toothpaste, sensitivity-care toothpaste, alcohol-free mouthwash, kids’ oral care, electric toothbrushes, and herbal/natural formulations will remain the strongest opportunity pockets.

Product innovation will move beyond basic cavity protection toward multifunctional claims such as enamel repair, gum protection, antibacterial freshness, SLS-free formulations, hydroxyapatite, charcoal, salt, and green-tea ingredients. Urban consumers will support premiumization, while rural and suburban markets will remain dependent on affordable family packs and small tubes. E-commerce and livestream commerce will increase the competitive importance of reviews, bundled offers, and influencer-led product discovery. Regulatory compliance will remain important because cosmetics in Vietnam require notification, product information dossiers, labeling compliance, safety responsibility, and alignment with the ASEAN Cosmetic Directive.

Major Players

- Unilever Vietnam – P/S

- Unilever Vietnam – Closeup

- Colgate-Palmolive Vietnam – Colgate

- Haleon Vietnam – Sensodyne

- Hawley & Hazel / Colgate-Palmolive – Darlie

- Procter & Gamble – Oral-B

- Johnson & Johnson – Listerine

- Lion Corporation – Systema

- Sunstar – GUM

- LG H&H – Perioe

- Amorepacific – Median

- Kao – Clear Clean

- Dr. Muối

- Ngọc Châu

- Traphaco Oral Care / Herbal Dental Care Portfolio

Key Target Audience

- Oral care product manufacturers

- FMCG distributors and wholesalers

- Pharmacy and drugstore chains

- Supermarket, hypermarket, and convenience-store operators

- E-commerce marketplaces and digital retail platforms

- Dental clinic chains and oral-health service providers

- Investments and venture capitalist firms

- Government and regulatory bodies (Ministry of Health, Drug Administration of Vietnam, Ministry of Industry and Trade, Vietnam Competition Commission)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the Vietnam Oral Care Market ecosystem, including manufacturers, importers, distributors, retailers, pharmacies, dentists, e-commerce platforms, and regulators. Key variables include product type, price tier, channel mix, urban-rural penetration, oral-health awareness, whitening demand, and sensitivity-care adoption.

Step 2: Market Analysis and Construction

Historical market data is compiled from credible industry reports, company sources, trade references, retail indicators, e-commerce statistics, and macroeconomic datasets. The analysis evaluates toothpaste penetration, toothbrush replacement cycles, mouthwash adoption, premium SKU availability, and retail-channel contribution to construct market revenue and volume assumptions.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through structured interviews with oral-care distributors, pharmacy buyers, FMCG retailers, dental practitioners, and e-commerce category managers. These consultations help verify brand visibility, pricing ladders, promotional intensity, product claims, channel margins, and the performance of mass versus premium oral-care products.

Step 4: Research Synthesis and Final Output

The final stage triangulates secondary data, bottom-up SKU analysis, trade interviews, and company-level competitive benchmarking. The output includes market sizing, segmentation, competitive analysis, future growth outlook, and strategic recommendations for manufacturers, investors, distributors, and retail-channel participants in the Vietnam Oral Care Market.

- Executive Summary

- Research Methodology (Market definitions and assumptions, oral care category taxonomy, SKU-level price tracking, retail audit approach, primary interviews with distributors/dentists/retailers, top-down market sizing, bottom-up brand-channel reconstruction, trade margin validation, limitations and forecast assumptions)

- Definition and Scope

- Market Genesis and Evolution

- Oral Hygiene Behaviour and Brushing Frequency Landscape

- Toothpaste-to-Toothbrush Consumption Ratio

- Dental Disease Burden and Preventive Care Need Gap

- Value Chain and Supply Chain Analysis

- Import Dependency and Domestic Manufacturing Footprint

- Route-to-Market Structure

- Regulatory Ecosystem

- Business Cycle and Seasonality

- Growth Drivers (Urbanization, disposable income, oral-health awareness, school dental programs, beauty-conscious whitening demand, modern retail penetration)

- Market Challenges (Price sensitivity, counterfeit risk, low flossing adoption, rural access gap, limited dentist visits, claim substantiation requirements)

- Opportunities (Premium sensitivity care, kids’ oral care, whitening toothpaste, electric toothbrushes, alcohol-free mouthwash, dental-clinic channel, subscription packs)

- Trends (Herbal/natural toothpaste, whitening strips, charcoal claims, Korean/Japanese imported brands, livestream commerce, eco-friendly toothbrushes)

- Government Regulation (Cosmetic notification, ASEAN Cosmetic Directive alignment, labeling, ingredient restrictions, import compliance, post-market surveillance)

- SWOT Analysis (Brand concentration, multinational strength, local herbal positioning, channel fragmentation, premium white-space)

- Stakeholder Ecosystem (Manufacturers, importers, distributors, dentists, pharmacies, modern trade, e-commerce platforms, regulatory bodies)

- Porter’s Five Forces (Supplier power, buyer power, threat of substitutes, threat of new entrants, competitive rivalry)

- Competition Ecosystem (P/S dominance, Closeup youth positioning, Colgate mass-premium stretch, Sensodyne specialist care, Darlie whitening/herbal imports)

- By Value (2020-2025)

- By Volume(2020-2025)

- By Average Selling Price (2020-2025)

- By Per Capita Oral Care Spend (2020-2025)

- By Urban vs Rural Consumption (2020-2025)

- By Modern Trade vs Traditional Trade Contribution (2020-2025)

- By Product Type (In Value%)

Toothpaste

Manual Toothbrush

Electric Toothbrush

Mouthwash/Dental Rinse

Dental Floss/Interdental Cleaner

Tooth Whitener

Denture Care

Mouth Freshener - By Toothpaste Benefit Claim (In Value%)

Cavity Protection

Whitening

Sensitivity Relief

Gum Care

Herbal/Natural

Fresh Breath

Children’s Fluoride

Total Care - By Consumer Age Group (In Value%)

Kids

Teens

Adults

Elderly

Denture Users

Orthodontic Users - By Price Tier (In Value%)

Mass

Masstige

Premium

Dentist-Recommended Premium

Imported Premium - By Distribution Channel (In Value%)

Traditional Grocery

Supermarkets/Hypermarkets

Convenience Stores

Pharmacies/Drugstores

Health & Beauty Chains

Dental Clinics

E-commerce Marketplaces

Brand-Owned Online Stores - By Region (In Value%)

Northern Vietnam

Southern Vietnam

Central Vietnam

Red River Delta

Southeast Vietnam

Mekong Delta

Urban Tier-1 Cities

Rural Provinces - By Pack Format (In Value%)

Family Tubes

Small Tubes

Travel Packs

Pump Bottles

Mouthwash Bottles

Blister-Packed Toothbrushes

Multipacks

Refill/Eco Packs - By Ingredient Positioning (In Value%)

Fluoride

Charcoal

Salt

Green Tea

Betel Leaf

Herbal Extracts

Hydroxyapatite

Alcohol-Free

SLS-Free

Vegan/Cruelty-Free

- Market Share of Major Players by Value and Volume, By Product Type, By Toothpaste Benefit Claim)

- Cross Comparison Parameters (Product portfolio breadth, toothpaste SKU count, whitening claim strength, sensitivity-care portfolio, herbal/natural positioning, dentist recommendation strength, e-commerce marketplace rating/visibility, modern trade shelf presence)

- Pricing Analysis by Key SKUs

- Promotion and Discounting Analysis

- Distribution Reach and Channel Mix

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Unilever Vietnam – P/S

Unilever Vietnam – Closeup

Colgate-Palmolive Vietnam – Colgate

Haleon Vietnam – Sensodyne

Hawley & Hazel / Colgate-Palmolive – Darlie

Procter & Gamble – Oral-B

Johnson & Johnson – Listerine

Lion Corporation – Systema

Sunstar – GUM

LG H&H – Perioe

Amorepacific / Median

Kao – Clear Clean

Dr. Muối

Ngọc Châu

Traphaco Oral Care / Herbal Dental Care Portfolio

- Household Oral Care Basket Analysis

- Adult Toothpaste Purchase Cycle

- Kids’ Oral Care Decision-Making

- Dentist and Pharmacy Recommendation Funnel

- Urban vs Rural Oral Hygiene Behaviour

- Consumer Pain Points

- Brand Switching and Promotional Sensitivity

- Willingness to Pay for Premium Claims

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

- By Per Capita Spend (2026-2035)

- By Premium Oral Care Contribution (2026-2035)

- By E-commerce Contribution (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now