Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Vietnam’s semiconductor infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by multinational semiconductor assembly, testing, and packaging investments alongside expansion of electronics manufacturing clusters. Global firms increased spending on cleanrooms, process utilities, and advanced manufacturing support systems to localize semiconductor supply chains. Government incentives for high-tech manufacturing and foreign direct investment further stimulated development of fabrication-ready industrial parks, specialty gas distribution networks, and contamination-controlled production environments supporting chip assembly and advanced packaging operations.

Northern provinces including Bac Ninh, Thai Nguyen, and Hai Phong dominate semiconductor infrastructure deployment due to concentration of multinational electronics and semiconductor manufacturing complexes supported by established industrial ecosystems and logistics connectivity. Ho Chi Minh City and surrounding southern economic zones host advanced packaging and testing facilities benefiting from skilled labor pools and export-oriented manufacturing bases. These regions provide power reliability, industrial land availability, and supplier networks required for semiconductor facility infrastructure development.

Market Segmentation

By Product Type

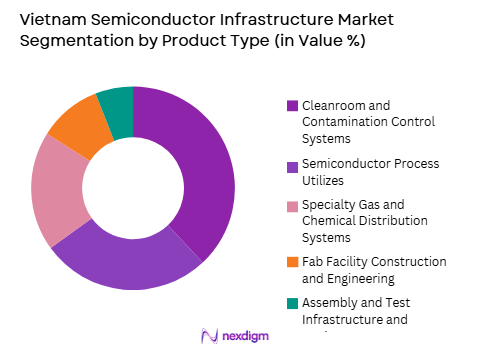

Vietnam Semiconductor Infrastructure market is segmented by product type into cleanroom and contamination control systems, semiconductor process utilities, specialty gas and chemical distribution systems, fab facility construction and engineering, and assembly and test infrastructure equipment. Recently, cleanroom and contamination control systems has a dominant market share due to factors such as stringent semiconductor manufacturing standards, expansion of assembly and packaging plants, and rising investment in controlled production environments.

By End User

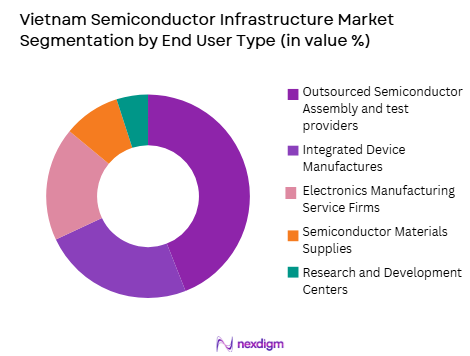

Vietnam Semiconductor Infrastructure market is segmented by end user into outsourced semiconductor assembly and test providers, integrated device manufacturers, electronics manufacturing services firms, semiconductor materials suppliers, and research and development centers. Recently, outsourced semiconductor assembly and test providers has a dominant market share due to factors such as Vietnam’s strategic role in global packaging supply chains, labor competitiveness, and rapid expansion of multinational OSAT operations. Global chip companies increasingly shift assembly and testing capacity to Vietnam to diversify production away from concentrated geographies.

Competitive Landscape

Vietnam’s semiconductor infrastructure market is dominated by global engineering, cleanroom, and industrial construction firms partnering with multinational semiconductor manufacturers establishing assembly and packaging facilities. International technology infrastructure vendors supply contamination control, gas distribution, and process utility systems, while local construction and industrial developers execute facility development. Competition centers on turnkey semiconductor facility capability, compliance with semiconductor standards, and ability to deliver rapid scalable infrastructure for multinational investors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Semiconductor Facility Capability |

| Samsung Engineering | 1970 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Air Liquide | 1902 | France | ~ | ~ | ~ | ~ | ~ |

| Linde | 1879 | UK | ~ | ~ | ~ | ~ | ~ |

| Exyte | 1912 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kajima Corporation | 1840 | Japan | ~ | ~ | ~ | ~ | ~ |

Vietnam Semiconductor Infrastructure Market Analysis

Growth Drivers

Foreign Direct Investment in Semiconductor Assembly and Packaging Facilities

Vietnam has emerged as a strategic destination for multinational semiconductor firms seeking geographic diversification of assembly, testing, and packaging operations, resulting in substantial investment in semiconductor infrastructure across industrial zones. Global chip manufacturers and outsourced semiconductor assembly providers are establishing large-scale packaging plants requiring cleanrooms, process utilities, chemical distribution systems, and contamination-controlled manufacturing environments. Competitive labor costs, stable political conditions, and proximity to Asian electronics supply chains make Vietnam attractive for back-end semiconductor manufacturing. Government incentives including tax benefits, land concessions, and high-tech industrial park development accelerate foreign investment in semiconductor facilities. Expansion of electronics manufacturing clusters in northern provinces creates ecosystem synergies supporting semiconductor packaging operations. As multinational companies scale Vietnamese operations to support global chip demand, infrastructure investment in cleanroom facilities, utilities, and fab-ready industrial spaces increases significantly. These foreign direct investment flows form the primary structural driver of Vietnam’s semiconductor infrastructure market growth.

Government High-Tech Manufacturing and Semiconductor Strategy Initiatives

Vietnam’s national industrial strategy prioritizes semiconductor and high-tech manufacturing development through policy incentives, infrastructure planning, and investment promotion programs that stimulate semiconductor facility construction and supporting infrastructure deployment. Government agencies are establishing semiconductor-focused industrial parks with pre-built cleanroom-ready spaces, reliable power supply, and advanced utilities to attract multinational chip investors. Strategic partnerships with global semiconductor firms aim to localize assembly, packaging, and eventually fabrication capabilities. Public investment in energy, logistics, and high-tech workforce training supports semiconductor ecosystem expansion. Regulatory frameworks and investment incentives reduce entry barriers for semiconductor manufacturers establishing facilities in Vietnam. State-backed infrastructure programs also improve specialty gas supply networks and chemical logistics required for semiconductor processes. As national semiconductor ambitions strengthen, government-led industrial infrastructure development continues to drive semiconductor facility construction and associated infrastructure demand across Vietnam.

Market Challenges

Limited Domestic Semiconductor Ecosystem and Upstream Capability

Vietnam’s semiconductor infrastructure market faces constraints due to limited domestic semiconductor design, fabrication, and materials ecosystem, resulting in heavy dependence on foreign firms and technologies for infrastructure development and operation. Absence of large-scale wafer fabrication facilities restricts demand for advanced front-end semiconductor infrastructure relative to packaging operations. Local suppliers of specialty chemicals, gases, and semiconductor equipment remain underdeveloped, increasing reliance on imported infrastructure systems. Workforce expertise in semiconductor facility design, contamination control engineering, and process utility management is limited domestically. Technology transfer from multinational firms remains gradual, slowing ecosystem maturation. These structural gaps constrain diversification of semiconductor infrastructure beyond assembly and testing facilities and limit domestic value addition.

High Capital and Utility Requirements of Semiconductor Facilities

Semiconductor manufacturing infrastructure requires substantial capital investment and reliable utilities including ultra-pure water, stable electricity, specialty gases, and advanced waste treatment systems, posing challenges for rapid infrastructure expansion in Vietnam. Semiconductor facilities demand uninterrupted power and high-quality water systems exceeding standard industrial infrastructure capabilities. Development of such utilities requires coordinated investment in energy, water treatment, and industrial services infrastructure. High upfront costs and long development timelines discourage smaller investors and local firms. Environmental compliance requirements for chemical handling and waste management increase project complexity and cost. Infrastructure developers must integrate advanced utilities within industrial parks to meet semiconductor standards. These capital and utility constraints slow expansion of semiconductor manufacturing infrastructure beyond established industrial zones.

Opportunities

Expansion into Advanced Packaging and Semiconductor Back-End Technologies

Vietnam has significant opportunity to expand semiconductor infrastructure supporting advanced packaging technologies such as system-in-package, heterogeneous integration, and chiplet assembly as global semiconductor supply chains evolve. Advanced packaging facilities require higher-grade cleanrooms, precision process utilities, and specialized assembly infrastructure beyond conventional packaging lines. Multinational chip firms increasingly seek diversified advanced packaging locations outside traditional hubs, creating opportunity for Vietnam to upgrade semiconductor infrastructure capability. Government incentives and industrial park readiness can attract investment in advanced packaging plants. Development of such infrastructure increases technological sophistication and value addition within Vietnam’s semiconductor sector. As advanced packaging demand grows globally, Vietnam can position itself as a regional hub for next-generation semiconductor back-end manufacturing infrastructure.

Development of Domestic Semiconductor Industrial Parks and Supply Chains

Vietnam can capitalize on semiconductor infrastructure demand by developing specialized semiconductor industrial parks integrating cleanrooms, utilities, gas supply networks, and logistics tailored to chip manufacturing requirements. Dedicated semiconductor zones reduce infrastructure costs and deployment timelines for investors by providing pre-engineered facilities. Localization of specialty gas, chemical, and materials supply chains within these parks enhances ecosystem resilience. Partnerships with global infrastructure and semiconductor firms can accelerate technology transfer and workforce development. Such integrated semiconductor industrial parks attract multiple investors, creating cluster economies and sustained infrastructure demand. As Vietnam advances semiconductor ambitions, development of dedicated semiconductor infrastructure ecosystems presents long-term market opportunity.

Future Outlook

Vietnam’s semiconductor infrastructure market is expected to expand steadily as multinational assembly and packaging investments deepen and government semiconductor strategies mature. Advanced packaging and cleanroom demand will increase alongside expansion of electronics manufacturing clusters. Development of semiconductor-ready industrial parks and utilities will attract new investors. Localization of supply chains and infrastructure capability will strengthen ecosystem depth. Continued foreign investment and policy support will sustain long-term infrastructure growth.

Major Players

- Exyte

- Air Liquide

- Linde

- Samsung Engineering

- Kajima Corporation

- Taikisha

- JGC Holdings

- Kurita Water Industries

- Veolia Water Technologies

- SUEZ

- INTECH Group

- CTCI

- Hoa Binh Construction

- Tan Tao Group

- Vinavico Group

Key Target Audience

- Semiconductor manufacturers

- OSAT providers

- Electronics manufacturing firms

- Industrial park developers

- Specialty gas suppliers

- Government and regulatory bodies

- Investments and venture capitalist firms

- Industrial infrastructure investors

Research Methodology

Step 1: Identification of Key Variables

Key variables including semiconductor facility investments, cleanroom capacity additions, utilities infrastructure deployment, and industrial park development were identified. Infrastructure spending patterns across semiconductor assembly, packaging, and manufacturing facilities were mapped to quantify market demand.

Step 2: Market Analysis and Construction

Bottom-up modeling combined facility construction costs, cleanroom installations, and utilities infrastructure investment to estimate market size. Segmentation reflected infrastructure categories and end-user facility deployment across semiconductor operations in Vietnam.

Step 3: Hypothesis Validation and Expert Consultation

Industry consultations with semiconductor manufacturers, infrastructure engineering firms, and industrial developers validated investment trends, facility requirements, and deployment costs. Experts confirmed infrastructure standards, ecosystem constraints, and policy influences affecting market growth.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights were synthesized into market estimates, segmentation, and competitive analysis. Cross-verification ensured consistency across facility investments, infrastructure deployments, and industrial ecosystem development to produce final outputs.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government incentives and foreign direct investment in semiconductor manufacturing

Expansion of OSAT and electronics manufacturing ecosystem

Global supply chain diversification toward Southeast Asia - Market Challenges

Limited domestic wafer fabrication capability and technology depth

High capital and technical complexity of semiconductor facilities

Dependence on imported semiconductor equipment and materials - Market Opportunities

Development of advanced packaging and power semiconductor facilities

Integration into global semiconductor supply chains

Establishment of national semiconductor research and pilot fabs - Trends

Growth of outsourced semiconductor assembly and test capacity

Investment in advanced packaging and heterogeneous integration

Localization of semiconductor supply chain infrastructure - Government regulations

National semiconductor industry development strategy

Foreign investment incentives for high tech manufacturing

Technology transfer and localization requirements - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Facility Infrastructure

Semiconductor Assembly and Test Infrastructure

Cleanroom and Contamination Control Systems

Fab Utilities and Process Support Systems

Specialty Gas and Chemical Distribution Systems - By Platform Type (In Value%)

Front-End Wafer Fabrication Plants

Back-End Assembly and Test Facilities

Semiconductor R&D and Pilot Lines

Power Semiconductor Production Lines

Advanced Packaging Facilities - By Fitment Type (In Value%)

Greenfield Semiconductor Facilities

Brownfield Fab Expansion Projects

Modular Cleanroom Installations

Integrated Fab Utility Systems

Retrofitted Assembly Line Infrastructure - By End User Segment (In Value%)

Integrated Device Manufacturers

Outsourced Semiconductor Assembly and Test Providers

Foundry and Wafer Fabrication Operators

Electronics Manufacturing Services Firms

Government and Research Institutions - By Procurement Channel (In Value%)

Direct OEM Equipment Procurement

Engineering Procurement Construction Contracts

System Integrator Fab Solutions

Government Semiconductor Programs

Joint Venture Technology Partnerships

- Market Share Analysis

- Cross Comparison Parameters (Facility Scale Capability, Process Node Support, Cleanroom Engineering Expertise, Fab Utility Integration, Advanced Packaging Capability, EPC Project Execution Strength, Local Supply Chain Integration, Technology Transfer Capability, Regional Fab Experience, Equipment Installation Precision)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amkor Technology Vietnam

Intel Products Vietnam

Samsung Electronics Vietnam

Foxconn Industrial Internet Vietnam

ASE Technology Vietnam

JCET Vietnam

SPIL Vietnam

TSMC Vietnam

Lam Research Vietnam

Applied Materials Vietnam

Tokyo Electron Vietnam

Air Liquide Vietnam

Linde Vietnam

ASMPT Vietnam

Besco Vietnam

- OSAT providers drive infrastructure expansion in assembly and packaging facilities

- Multinational electronics firms require localized semiconductor supply chains

- Government and research institutes invest in pilot and R&D fabs

- Foundry operators explore regional fabrication and packaging capacity

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now