Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Vietnam’s semiconductor manufacturing market represents a rapidly expanding segment of the country’s advanced electronics industry, supported by strong foreign direct investment and government-led industrial development policies. Based on a recent historical assessment, Vietnam’s semiconductor manufacturing ecosystem generated approximately USD ~ in industry value through semiconductor assembly, testing, packaging, and emerging fabrication activities. Growth is driven by multinational semiconductor companies establishing manufacturing operations, expanding global electronics demand, and increasing supply-chain diversification strategies among semiconductor firms seeking alternative manufacturing locations across Southeast Asia.

Ho Chi Minh City, Hanoi, and Bac Ninh have emerged as the dominant semiconductor manufacturing clusters due to their well-developed electronics manufacturing infrastructure and access to skilled technical labor. These regions host major semiconductor packaging and testing facilities operated by multinational technology companies while benefiting from proximity to global electronics supply chains across East Asia. Government-supported technology parks, advanced manufacturing zones, and export-oriented industrial policies further strengthen the concentration of semiconductor manufacturing investment within these major Vietnamese industrial regions.

Market Segmentation

By Product Type

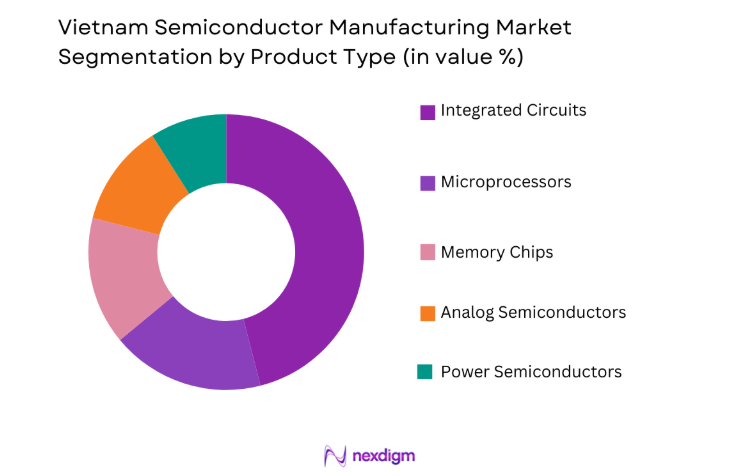

Vietnam Semiconductor Manufacturing Market is segmented by product type into Integrated Circuits, Microprocessors, Memory Chips, Analog Semiconductors, and Power Semiconductors. Recently, Integrated Circuits has a dominant market share due to factors such as strong demand from consumer electronics manufacturers, extensive global supply chain integration, and large-scale semiconductor packaging and testing facilities operating within Vietnam’s electronics manufacturing clusters. Integrated circuits serve as essential components across smartphones, computing devices, telecommunications equipment, and automotive electronics. Multinational semiconductor companies operating manufacturing facilities in Vietnam focus heavily on IC packaging, testing, and assembly operations that support global semiconductor distribution networks. These manufacturing activities require high-volume production capacity and advanced semiconductor packaging technologies that further reinforce the dominance of integrated circuits within Vietnam’s semiconductor manufacturing ecosystem.

By End-Use Industry

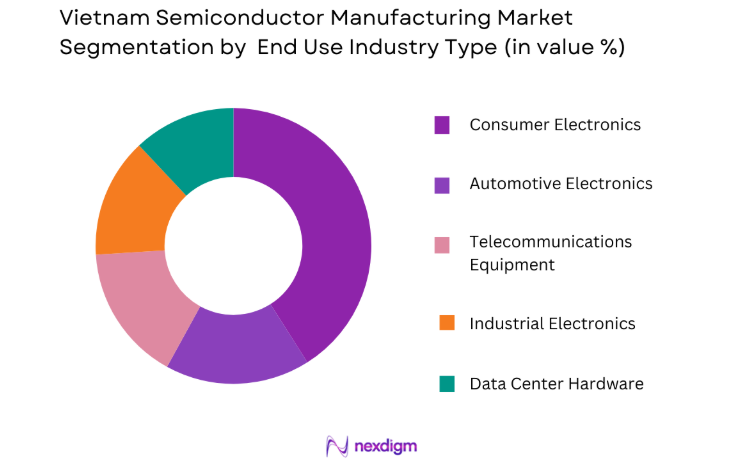

Vietnam Semiconductor Manufacturing Market market is segmented by end-use industry into Consumer Electronics, Automotive Electronics, Telecommunications Equipment, Industrial Electronics, and Data Center Hardware. Recently, Consumer Electronics has a dominant market share due to factors such as Vietnam’s extensive electronics manufacturing ecosystem, global smartphone production networks, and strong export-oriented electronics assembly industries operating throughout the country. Consumer electronics manufacturers require large volumes of semiconductors for smartphones, tablets, computers, wearable devices, and smart home products. Vietnam hosts numerous global electronics assembly operations supplying international technology brands, which significantly increases semiconductor demand from the consumer electronics sector. Semiconductor packaging and testing facilities located within Vietnam therefore operate closely with consumer electronics manufacturing clusters, strengthening the dominance of this end-use segment across the semiconductor manufacturing supply chain.

Competitive Landscape

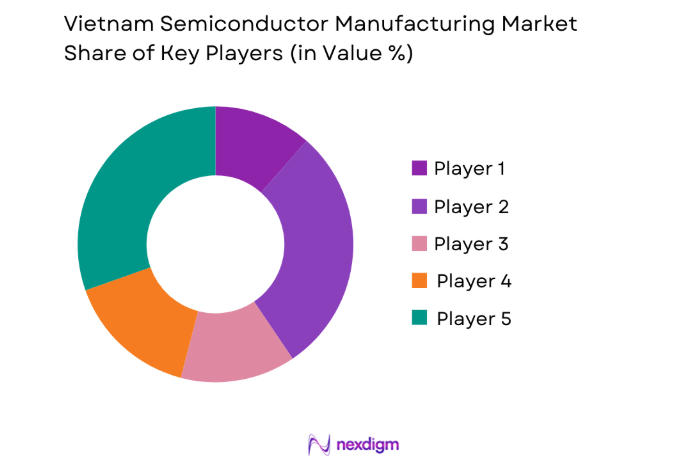

Vietnam’s semiconductor manufacturing market demonstrates a moderately consolidated competitive landscape dominated by multinational semiconductor corporations operating large assembly, packaging, and testing facilities within the country. Global technology companies drive technological development through advanced semiconductor manufacturing equipment, specialized chip packaging technologies, and integrated electronics supply chains linking Vietnam to global semiconductor markets. Strong collaboration between international semiconductor firms and Vietnam’s industrial technology parks continues to strengthen the competitive environment and accelerate industry development.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Manufacturing Presence in Vietnam |

| Intel Corporation | 1968 | United States | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

| Amkor Technology | 1968 | United States | ~ | ~ | ~ | ~ | ~ |

| ASE Technology Holding | 1984 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | United States | ~ | ~ | ~ | ~ | ~ |

Vietnam Semiconductor Manufacturing Market Analysis

Growth Drivers

Expansion of Foreign Direct Investment in Semiconductor Manufacturing Facilities

Rapid expansion of foreign direct investment into Vietnam’s semiconductor manufacturing sector significantly strengthens the country’s position within the global semiconductor supply chain. Multinational semiconductor companies increasingly establish manufacturing facilities across Vietnam in order to diversify global semiconductor production and reduce supply chain risks associated with geographic concentration. Vietnam offers competitive manufacturing costs, stable political conditions, and a growing pool of skilled engineering professionals capable of supporting semiconductor production activities. Government industrial policies actively promote semiconductor investment through tax incentives, infrastructure development, and technology park expansion. Major global semiconductor corporations have already developed large packaging and testing facilities within Vietnam that support semiconductor exports worldwide. Supply chain diversification strategies implemented by global technology companies further increase Vietnam’s attractiveness as an alternative semiconductor manufacturing destination. Electronics manufacturing clusters located across Bac Ninh, Ho Chi Minh City, and Da Nang provide integrated supply chain ecosystems supporting semiconductor assembly and electronics production. Advanced semiconductor packaging technologies including system-in-package solutions and high-density chip integration increasingly operate within Vietnam’s manufacturing facilities. As semiconductor demand continues rising globally due to digital technologies, artificial intelligence applications, and advanced electronics production, foreign direct investment into Vietnam’s semiconductor manufacturing sector continues expanding rapidly.

Rapid Expansion of Consumer Electronics Manufacturing Ecosystems

Vietnam’s rapidly expanding consumer electronics manufacturing ecosystem significantly accelerates demand for semiconductor manufacturing capacity across the country. Global electronics manufacturers increasingly establish large production facilities within Vietnam to manufacture smartphones, laptops, wearable devices, and other consumer electronic products. Semiconductor chips serve as the fundamental components powering these electronic devices, creating strong domestic demand for semiconductor packaging, assembly, and testing operations. Vietnam hosts manufacturing operations supplying global technology companies that require high-volume semiconductor integration within consumer electronics products. Large electronics manufacturing clusters across northern and southern Vietnam operate advanced production lines that integrate semiconductors within complex electronic systems. The strong presence of multinational electronics manufacturers further stimulates semiconductor ecosystem development through supplier networks and component manufacturing partnerships. Consumer electronics production requires numerous semiconductor components including processors, memory chips, power management integrated circuits, and wireless communication chips. Semiconductor manufacturing facilities located within Vietnam operate closely with electronics assembly plants to ensure efficient component supply chains. As global demand for connected consumer electronics devices continues increasing due to digital lifestyles, mobile computing, and smart home technologies, semiconductor manufacturing demand within Vietnam continues expanding significantly.

Market Challenges

Limited Domestic Semiconductor Design and Fabrication Capabilities

Vietnam’s semiconductor manufacturing industry currently faces structural challenges related to limited domestic semiconductor design capabilities and advanced wafer fabrication infrastructure. The country’s semiconductor ecosystem primarily focuses on assembly, packaging, and testing operations rather than full semiconductor fabrication processes. Advanced wafer fabrication facilities require extremely high capital investment, specialized engineering expertise, and advanced semiconductor manufacturing technologies. Most semiconductor chips manufactured within Vietnam are fabricated elsewhere before being shipped into the country for packaging and testing operations. Limited domestic semiconductor research and development infrastructure restricts the ability of local companies to develop proprietary semiconductor technologies. Semiconductor design capabilities remain concentrated within a small number of multinational technology companies operating research facilities within Vietnam. Building a comprehensive semiconductor manufacturing ecosystem requires long-term investments in semiconductor engineering education, research laboratories, and advanced fabrication infrastructure. Semiconductor fabrication plants also require extremely complex supply chains involving high-purity materials, specialized equipment, and advanced process engineering capabilities. Without significant domestic semiconductor design and fabrication capacity, Vietnam remains dependent on international semiconductor supply chains for critical chip production technologies.

Global Semiconductor Supply Chain Volatility and Technology Competition

The semiconductor industry experiences frequent supply chain volatility driven by geopolitical tensions, technology competition, and rapid fluctuations in global semiconductor demand. Semiconductor manufacturing operations within Vietnam depend heavily on international supply chains for semiconductor wafers, advanced manufacturing equipment, and specialized materials used throughout chip production processes. Global semiconductor shortages and disruptions can significantly impact semiconductor packaging and testing facilities operating within Vietnam. Semiconductor manufacturing also involves complex international trade relationships influenced by export regulations, technology transfer restrictions, and geopolitical competition among major semiconductor producing countries. Competition among global semiconductor manufacturing hubs including Taiwan, South Korea, China, and the United States creates additional pressure on emerging semiconductor production locations such as Vietnam. Advanced semiconductor manufacturing technologies evolve rapidly, requiring constant upgrades in manufacturing equipment and engineering expertise. Semiconductor companies must continuously invest in advanced packaging technologies, automation systems, and semiconductor process improvements to remain competitive within the global semiconductor industry. These supply chain uncertainties and technology competition challenges require Vietnam’s semiconductor industry to continuously strengthen its technological capabilities and supply chain resilience.

Opportunities

Development of Advanced Semiconductor Packaging Technologies

The global semiconductor industry increasingly adopts advanced semiconductor packaging technologies designed to enhance chip performance, energy efficiency, and system integration capabilities. Vietnam’s semiconductor manufacturing sector has strong potential to become a global hub for advanced packaging technologies including system-in-package architectures, 3D chip stacking, and heterogeneous chip integration. Advanced packaging technologies allow semiconductor manufacturers to combine multiple semiconductor components within compact chip systems capable of delivering high computational performance. Semiconductor companies already operating manufacturing facilities within Vietnam are investing in advanced chip packaging research and manufacturing capabilities. Advanced packaging requires specialized semiconductor engineering expertise, precision manufacturing equipment, and highly controlled production environments that align well with Vietnam’s growing electronics manufacturing ecosystem. Global demand for advanced semiconductor packaging solutions continues increasing due to artificial intelligence processors, high-performance computing chips, and next generation mobile devices. Semiconductor manufacturers increasingly outsource advanced packaging operations to specialized facilities located within global electronics manufacturing clusters. Vietnam therefore holds significant opportunities to expand its semiconductor industry through technological leadership in advanced semiconductor packaging solutions supporting the global semiconductor supply chain.

Government Supported Semiconductor Innovation and Technology Ecosystem Development

Vietnam’s government actively promotes semiconductor technology development through national industrial strategies focused on advanced electronics manufacturing and digital technology innovation. National technology development programs encourage semiconductor companies to establish research facilities, advanced manufacturing plants, and engineering training programs across Vietnam’s technology parks. Public investments into semiconductor education programs aim to develop a highly skilled semiconductor engineering workforce capable of supporting advanced semiconductor manufacturing operations. Technology partnerships between multinational semiconductor companies and Vietnamese universities support semiconductor design training, microelectronics research, and semiconductor process engineering education. Government incentives including tax reductions, investment subsidies, and infrastructure development encourage global semiconductor manufacturers to expand operations within Vietnam. Industrial technology zones across Ho Chi Minh City, Da Nang, and northern Vietnam provide specialized facilities designed to support high-technology manufacturing industries. As global semiconductor demand continues expanding due to artificial intelligence, data center infrastructure, automotive electronics, and advanced communication systems, Vietnam’s government-supported semiconductor innovation ecosystem creates significant opportunities for long-term semiconductor industry growth.

Future Outlook

Vietnam’s semiconductor manufacturing market is expected to experience strong expansion as global semiconductor companies continue diversifying supply chains across Southeast Asia. Government industrial strategies supporting semiconductor investment, technology parks, and workforce development programs will further strengthen the country’s semiconductor ecosystem. Rising global demand for consumer electronics, automotive semiconductors, and data center processors will increase semiconductor production requirements. Technological advancements in advanced semiconductor packaging, integrated chip systems, and electronics manufacturing automation are also expected to accelerate Vietnam’s role within global semiconductor supply chains.

Major Players

- Intel Corporation

- Samsung Electronics

- Amkor Technology

- ASE Technology Holding

- Texas Instruments

- Qualcomm Incorporated

- SK Hynix

- Micron Technology

- Infineon Technologies

- NXP Semiconductors

- STMicroelectronics

- Renesas Electronics

- Broadcom Inc

- MediaTek Inc

- ON Semiconductor

Key Target Audience

- Semiconductor Manufacturing Companies

- Consumer Electronics Manufacturers

- Automotive Electronics Manufacturers

- Semiconductor Equipment Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Telecommunications Infrastructure Companies

Research Methodology

Step 1: Identification of Key Variables

Key semiconductor manufacturing variables including production capacity, investment flows, semiconductor packaging technologies, and electronics manufacturing demand were identified. These variables formed the analytical framework used to evaluate Vietnam’s semiconductor manufacturing ecosystem and its integration with global semiconductor supply chains.

Step 2: Market Analysis and Construction

Market data was compiled using industry publications, semiconductor trade statistics, company financial disclosures, and government industrial policy reports. The data was analyzed to construct an accurate view of semiconductor manufacturing activity, industry structure, and competitive positioning within Vietnam.

Step 3: Hypothesis Validation and Expert Consultation

Industry insights were validated through consultation with semiconductor engineers, electronics manufacturing specialists, and supply chain experts. Their technical perspectives helped confirm the operational realities of semiconductor assembly, packaging, and testing facilities operating within Vietnam’s electronics manufacturing clusters.

Step 4: Research Synthesis and Final Output

All validated information was consolidated into a structured market research framework combining qualitative analysis and quantitative insights. The final research output provides a comprehensive understanding of Vietnam’s semiconductor manufacturing industry dynamics, competitive environment, and future development opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of Electronics Manufacturing and Export Industries in Vietnam

Government Incentives Encouraging Foreign Semiconductor Investment

Growing Data Center and Telecommunications Infrastructure Development - Market Challenges

High Capital Requirements for Semiconductor Fabrication Facilities

Limited Domestic Semiconductor Engineering Talent Pool

Dependence on Imported Semiconductor Manufacturing Equipment - Market Opportunities

Development of Semiconductor Assembly and Testing Hubs

Strategic Partnerships with Global Semiconductor Foundries

Increasing Demand for Semiconductor Chips in Consumer Electronics Manufacturing - Trends

Rising Investment in Semiconductor Packaging and Testing Facilities

Growing Integration of Advanced Semiconductor Technologies in Electronics Manufacturing - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor Wafer Fabrication Systems

Semiconductor Assembly and Packaging Systems

Semiconductor Testing Systems

Semiconductor Manufacturing Equipment

Semiconductor Materials and Specialty Chemicals - By Platform Type (In Value%)

Consumer Electronics Manufacturing

Automotive Electronics Manufacturing

Telecommunications Infrastructure Manufacturing

Industrial Electronics Manufacturing - By Fitment Type (In Value%)

Front End Semiconductor Fabrication

Back End Assembly and Packaging

Integrated Semiconductor Manufacturing Facilities

Outsourced Semiconductor Manufacturing Services - By End User Segment (In Value%)

Electronics and Consumer Device Manufacturers

Telecommunications Infrastructure Providers

Automotive and Industrial Electronics Manufacturers

- Market Share Analysis

- Cross Comparison Parameters (Technology Node Capability, Fabrication Capacity, Packaging Technology, Equipment Integration, Supply Chain Partnerships, Pricing Structure, Innovation Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intel Corporation

Samsung Electronics

Taiwan Semiconductor Manufacturing Company

United Microelectronics Corporation

GlobalFoundries

STMicroelectronics

Infineon Technologies

Texas Instruments

Amkor Technology

ASE Technology Holding

Applied Materials

ASML Holding

KLA Corporation

Lam Research

Foxconn Technology Group

- Electronics Manufacturers Increasing Demand for Integrated Circuit Production

- Telecommunications Companies Expanding Semiconductor Usage for Network Infrastructure

- Automotive Electronics Producers Requiring Semiconductor Components for Smart Vehicles

- Industrial Equipment Manufacturers Utilizing Semiconductor Devices in Automation Systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now