Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Vietnam truck aggregator market reached USD ~ billion based on a recent historical assessment, driven by accelerating digitalization of freight brokerage and growing demand for efficient truck utilization across manufacturing and retail supply chains. Expansion of eCommerce logistics networks, rising fuel costs encouraging load optimization, and government-backed digital transport initiatives have stimulated platform adoption. Increasing SME participation in online freight marketplaces and rapid mobile technology penetration among truck operators further strengthened transaction volumes and platform revenues across domestic road freight operations.

Ho Chi Minh City and Hanoi dominate Vietnam truck aggregator market activity due to dense industrial clusters, export-oriented manufacturing zones, and high logistics transaction intensity concentrated in these corridors. Ho Chi Minh City’s port connectivity and industrial parks generate large trucking demand, while Hanoi’s northern manufacturing belt and cross-border trade routes support continuous freight flows. Secondary hubs such as Hai Phong and Binh Duong also show strong adoption driven by logistics parks, port access, and expanding distribution infrastructure supporting nationwide supply chains.

Market Segmentation

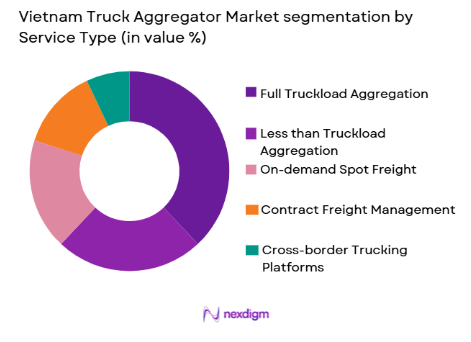

By Service Type

Vietnam Truck Aggregator market is segmented by service type into Full Truckload Aggregation, Less than Truckload Aggregation, On-demand Spot Freight, Contract Freight Management, and Cross-border Trucking Platforms. Recently, Full Truckload Aggregation has a dominant market share due to factors such as high demand from manufacturing exporters requiring dedicated truck capacity, strong presence of large fleet operators on digital platforms, infrastructure suitability for long-haul shipments, and shipper preference for predictable transit and pricing reliability across domestic corridors connecting industrial zones and ports.

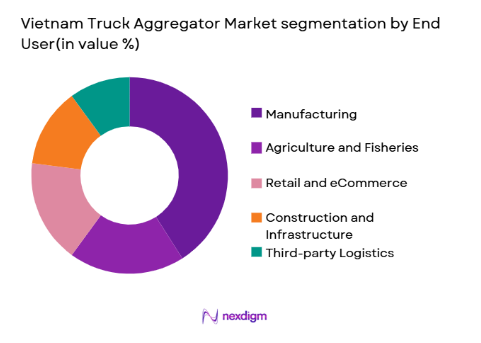

By End-user

Vietnam Truck Aggregator market is segmented by end-user into Manufacturing, Agriculture and Fisheries, Retail and eCommerce, Construction and Infrastructure, and Third-party Logistics. Recently, Manufacturing has a dominant market share due to factors such as concentrated industrial production volumes, consistent outbound freight requirements to ports and distribution centers, established contracts with logistics platforms, infrastructure alignment with industrial parks, and preference for integrated digital freight procurement supporting large-scale domestic and export supply chains.

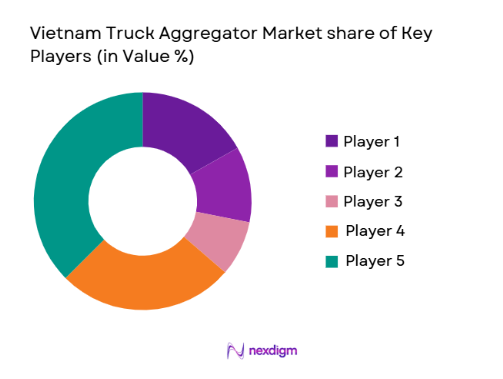

Competitive Landscape

Vietnam truck aggregator market shows moderate consolidation with a mix of domestic digital freight startups and logistics incumbents expanding platform capabilities. Leading players leverage large carrier networks, mobile-based load matching, and integrated logistics services to secure enterprise shippers. Market influence concentrates around firms offering nationwide coverage and technology-enabled freight visibility, while regional specialists maintain presence in niche corridors and cross-border trucking segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Integration Capability |

| Logivan | 2017 | Hanoi | ~ | ~ | ~ | ~ | ~ |

| Abivin | 2015 | Hanoi | ~ | ~ | ~ | ~ | ~ |

| EcoTruck | 2017 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ |

| Ahamove | 2015 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ |

| Lalamove Vietnam | 2013 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ |

Vietnam Truck Aggregator Market Analysis

Growth Drivers

Rapid Expansion of Export-Oriented Manufacturing Logistics Demand:

Vietnam’s transformation into a global manufacturing hub has substantially increased domestic trucking requirements linking factories, ports, and distribution centers across industrial corridors. Large volumes of electronics, textiles, furniture, and consumer goods require reliable long-haul truck capacity, encouraging shippers to adopt aggregator platforms for efficient carrier matching and route optimization. Industrial park development around Ho Chi Minh City, Hanoi, and Hai Phong has intensified freight density, making digital freight marketplaces economically viable. Export-driven supply chains demand predictable transit times and transparent pricing, which aggregator platforms provide through centralized booking and tracking. Manufacturers increasingly prefer digital freight procurement to reduce empty backhauls and logistics costs, reinforcing platform transaction growth. Rising container throughput in Vietnamese ports further amplifies inland trucking demand requiring coordinated capacity sourcing. Aggregators enable SMEs to access nationwide carriers previously unavailable through traditional brokers, expanding market reach. Continuous growth in industrial output sustains high freight volumes that structurally support aggregator adoption across domestic road logistics networks.

Growth of eCommerce and Retail Distribution Logistics:

expansion of Vietnam’s eCommerce sector has created complex distribution networks requiring flexible trucking capacity between fulfillment centers, warehouses, and urban delivery hubs. Online retail growth has increased intercity freight flows of consumer goods, electronics, and fast-moving merchandise, driving demand for on-demand and scheduled trucking services through aggregator platforms. Retailers increasingly adopt digital freight tools to manage seasonal demand spikes and multi-node distribution strategies efficiently. Expansion of modern retail chains and omnichannel logistics has raised shipment frequency and reduced shipment sizes, encouraging use of platform-based capacity aggregation. Aggregators offer real-time booking, tracking, and pricing transparency that aligns with retail supply chain responsiveness requirements. Growth of regional distribution centers in secondary cities has expanded trucking corridors and platform transaction volumes. Retail and eCommerce companies value dynamic capacity access without owning fleets, reinforcing aggregator reliance. Continued digital commerce penetration ensures sustained growth in trucking demand mediated through aggregator ecosystems.

Market Challenges

Fragmented Small-Scale Trucking Industry Structure:

Vietnam’s road freight sector consists predominantly of small fleet operators and independent truck owners, creating structural challenges for digital aggregation platforms seeking standardized service quality and capacity reliability. Many carriers operate informally with limited digital tools, reducing onboarding efficiency and platform utilization rates. Variability in vehicle standards, documentation, and service practices complicates matching algorithms and performance consistency. Aggregators must invest significantly in carrier training, verification, and integration to maintain service reliability across dispersed operators. Price competition among small carriers often undermines platform pricing stability and margins. Limited financial capacity of small operators constrains adoption of telematics and tracking technologies required for digital freight ecosystems. Regional fragmentation also restricts network density in certain corridors, reducing platform effectiveness. Persistent informality within trucking supply slows digital transformation and poses operational complexity for aggregator business models seeking scalable nationwide coverage.

Infrastructure Constraints and Logistics Bottlenecks:

Despite improvements, Vietnam’s road and logistics infrastructure faces congestion, limited highway capacity, and uneven connectivity between industrial zones and ports, affecting trucking efficiency and aggregator service performance. Urban congestion in major cities increases transit variability, reducing predictability required for digital freight scheduling. Port access delays and intermodal coordination challenges extend truck turnaround times and lower fleet utilization rates. Secondary road networks in rural production regions remain underdeveloped, constraining aggregator penetration in agriculture and resource logistics segments. Seasonal weather disruptions further complicate route planning and capacity availability. Infrastructure bottlenecks elevate operating costs for carriers, limiting participation in platform-based freight markets. Aggregators must account for unpredictable transit times in pricing and matching algorithms, affecting service reliability perceptions among shippers. Continued infrastructure limitations thus moderate platform scalability and constrain full realization of digital trucking efficiency gains across national freight corridors.

Opportunities

Integration with Cross-Border ASEAN Road Freight Networks:

Vietnam’s strategic location within Southeast Asia and participation in regional trade agreements create opportunities for truck aggregator platforms to expand into cross-border freight matching across Cambodia, Laos, Thailand, and southern China corridors. Growing regional manufacturing supply chains require coordinated trucking capacity for intermediate goods and finished products moving between ASEAN production hubs. Aggregators can enable digital booking and visibility for cross-border shipments traditionally managed by fragmented brokers. Harmonization of customs and transport regulations across ASEAN facilitates platform expansion into international corridors. Exporters seek reliable cross-border trucking to complement maritime logistics, increasing demand for digitally coordinated fleets. Platforms integrating multilingual interfaces, customs documentation tools, and regional carrier networks can capture emerging cross-border freight flows. Regional economic integration and trade growth will steadily increase cross-border trucking demand addressable through aggregator ecosystems. Expansion into ASEAN corridors offers revenue diversification beyond domestic freight markets.

Embedded Financial and Fleet Services for Carrier Ecosystems:

Truck aggregator platforms can extend beyond freight matching into financial services such as fuel financing, insurance, maintenance programs, and working capital loans tailored to small fleet operators. Vietnam’s fragmented trucking base faces limited access to formal financing, creating demand for platform-enabled financial inclusion tied to freight transaction histories. Aggregators possess operational data enabling risk assessment and credit scoring for carriers previously excluded from banking services. Providing embedded services strengthens carrier loyalty and platform retention while improving fleet reliability and capacity availability. Integrated maintenance and telematics programs can enhance vehicle performance and safety standards across aggregated fleets. Financial products linked to platform earnings cycles support cash flow stability for small operators, encouraging digital participation. Development of carrier ecosystems around platforms creates competitive differentiation and deeper network effects. Monetization of value-added services offers new revenue streams alongside core freight aggregation transactions.

Future Outlook

Vietnam truck aggregator market is expected to expand steadily as digital freight adoption deepens across manufacturing and retail logistics networks. Technology-enabled load matching, telematics integration, and real-time pricing systems will enhance platform efficiency and reliability. Government logistics modernization initiatives and infrastructure investments will support broader adoption across corridors. Growing eCommerce distribution complexity and regional trade integration will sustain demand for scalable digital trucking capacity over the coming years.

Major Players

- Logivan

- Abivin

- EcoTruck

- Ahamove

- Lalamove Vietnam

- Deliveree Vietnam

- GrabExpress Vietnam

- Be Delivery

- GHN Logistics

- Viettel Post

- Giao Hang Tiet Kiem

- Nhat Tin Logistics

- Vinalines Logistics

- Transimex

- Scommerce

Key Target Audience

- Trucking and fleet operators

- Manufacturing companies

- Retail and eCommerce companies

- Logistics service providers

- Supply chain technology vendors

- Infrastructure investment firms

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Market variables including freight demand, digital adoption, fleet structure, platform transactions, and logistics infrastructure were identified through industry databases and transport statistics.

Step 2: Market Analysis and Construction

Data from logistics associations, company disclosures, and trade statistics were synthesized to construct market size and segmentation estimates and competitive structure.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions and findings were validated through interviews with logistics operators, aggregators, and supply chain specialists across Vietnam freight ecosystem.

Step 4: Research Synthesis and Final Output

Validated insights were integrated into structured analysis covering drivers, challenges, segmentation, competition, and future outlook for Vietnam truck aggregator market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid expansion of Vietnam manufacturing exports driving domestic trucking demand

Growth of eCommerce and omnichannel retail logistics requirements

Digital transformation incentives in Vietnam transport sector

SME shipper adoption of digital freight platforms

Rising fuel and labor costs encouraging load optimization - Market Challenges

Fragmented trucking industry with large informal carrier base

Limited digital literacy among small fleet operators

Price competition and low platform switching costs

Regulatory complexity in cross province freight operations

Infrastructure bottlenecks and congestion in key corridors - Market Opportunities

Integration with cross border ASEAN logistics networks

AI driven pricing and capacity optimization services

Embedded finance and fleet services for carriers - Trends

Shift toward real time digital freight matching

Adoption of mobile first booking among SMEs

Platform consolidation through partnerships and acquisitions

Integration of telematics and tracking visibility tools

Growth of contract based digital freight procurement - Government Regulations & Defense Policy

National digital transport and logistics modernization programs

Electronic freight documentation and einvoice mandates

Road transport compliance and vehicle tracking regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Full Truckload Aggregation Platforms

Less than Truckload Matching Platforms

OnDemand Spot Freight Apps

Contract Freight Management Platforms

CrossBorder Trucking Aggregators - By Platform Type (In Value%)

Mobile App Based Aggregators

Web Based Freight Marketplaces

Integrated TMS Enabled Platforms

API Integrated Enterprise Platforms

Cloud Native Freight Exchanges - By Fitment Type (In Value%)

Shipper Direct Platforms

Broker Assisted Platforms

Carrier Managed Platforms

Hybrid Marketplace Platforms

Embedded Logistics Platforms - By EndUser Segment (In Value%)

Manufacturing Enterprises

Agriculture and Fisheries Producers

Retail and ECommerce Companies

Construction and Infrastructure Firms

Third Party Logistics Providers - By Procurement Channel (In Value%)

Direct Digital Booking

Enterprise Contracting

Logistics Broker Partnerships

Freight Forwarder Integration

Government and Industrial Tenders - By Material / Technology (in Value %)

AI Based Load Matching Algorithms

GPS and Telematics Integration

Cloud Logistics Infrastructure

Digital Freight Documentation Systems

Blockchain Enabled Freight Platforms

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Platform Scale, Carrier Network Size, Pricing Model, Technology Integration, Geographic Coverage, Service Types, Enterprise Solutions, Data Analytics Capability, CrossBorder Capability, ValueAdded Services)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Logivan

Abivin

EcoTruck

Ahamove

Lalamove Vietnam

Deliveree Vietnam

GrabExpress Vietnam

Be Delivery

GHN Logistics

Viettel Post

Giao Hang Tiet Kiem

Nhat Tin Logistics

Vinalines Logistics

Transimex

Scommerce

- Manufacturers adopting aggregators for cost efficient nationwide distribution

- Agriculture producers using digital trucking for time sensitive shipments

- Retail and eCommerce firms requiring scalable on demand capacity

- 3PL providers integrating aggregator capacity into service portfolios

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now