Download PDF

Download PDFMarket Overview

The Vietnam Used Harvester market current size stands at around USD ~ million, reflecting steady demand for pre-owned agricultural machinery among cost-sensitive buyers and service contractors. The market is shaped by replacement cycles, refurbishment activity, and the circulation of imported used units through dealer networks. Supply is influenced by machine age, refurbishment quality, and availability of spare parts, while demand is supported by seasonal harvesting intensity and mechanization needs across fragmented farm holdings and service cooperatives.

Demand concentration is highest in the Mekong Delta and Red River Delta due to dense paddy cultivation, irrigation coverage, and higher mechanization penetration. Secondary demand clusters extend across the Southeast and North Central and Central Coast, supported by logistics corridors and proximity to refurbishment hubs. Dealer ecosystems are more mature near provincial capitals, while policy enforcement on used equipment imports and emissions compliance is tighter in port-linked regions, shaping regional availability and channel structure.

Market Segmentation

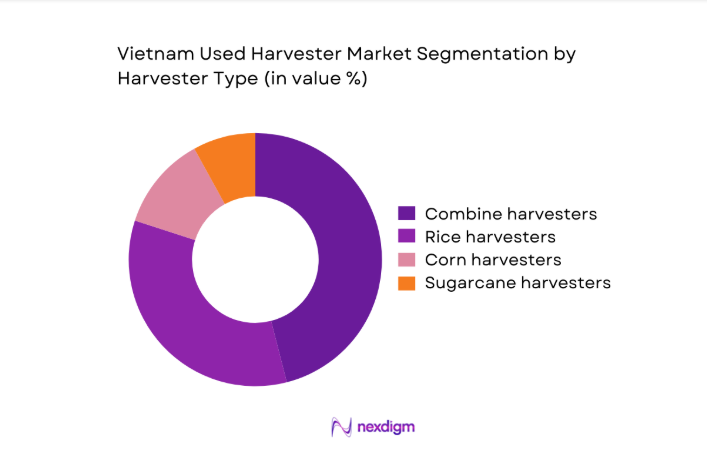

By Harvester Type

Used combine harvesters dominate due to their versatility across rice-intensive landscapes, enabling faster turnaround during compressed harvest windows and supporting contract harvesting fleets. Rice harvesters maintain strong uptake among smallholder clusters requiring lighter machines for waterlogged fields, while corn and sugarcane harvesters are adopted selectively in mechanized pockets. The dominance of combines is reinforced by parts availability, operator familiarity, and higher resale liquidity through established dealer channels. Regional cropping patterns, service contractor fleet strategies, and field conditions determine sub-segment traction, with equipment suitability for narrow bunds and wet soils influencing preference. Refurbishment capability further tilts demand toward platforms with standardized components and serviceable drivetrains.

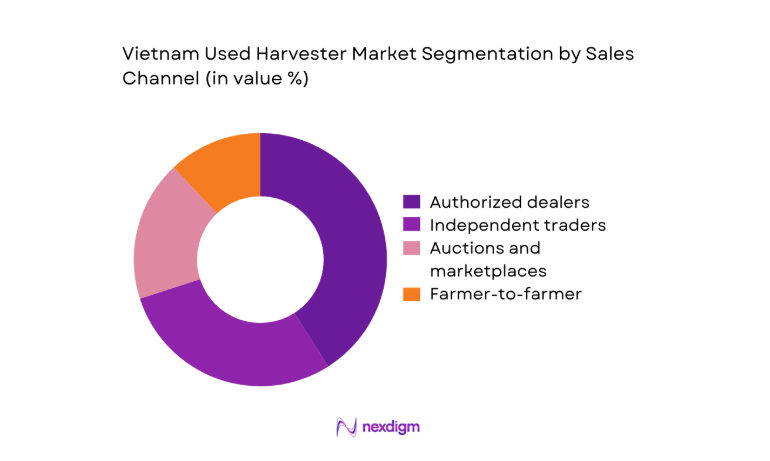

By Sales Channel

Authorized dealers lead due to refurbishment standards, warranty offerings, and financing facilitation, attracting institutional buyers and cooperatives seeking uptime assurance. Independent traders remain relevant in rural provinces, providing faster availability and flexible negotiations for price-sensitive farmers. Auctions and marketplaces are growing as discovery channels for seasonal purchases, while direct farmer-to-farmer transactions persist for localized exchanges and short distance logistics. Channel dominance reflects trust in post-sale support, access to spare parts, and credit facilitation, with dealers leveraging service networks to lock in fleet operators. Digital listings improve price transparency, but physical inspection remains decisive due to variable machine conditions.

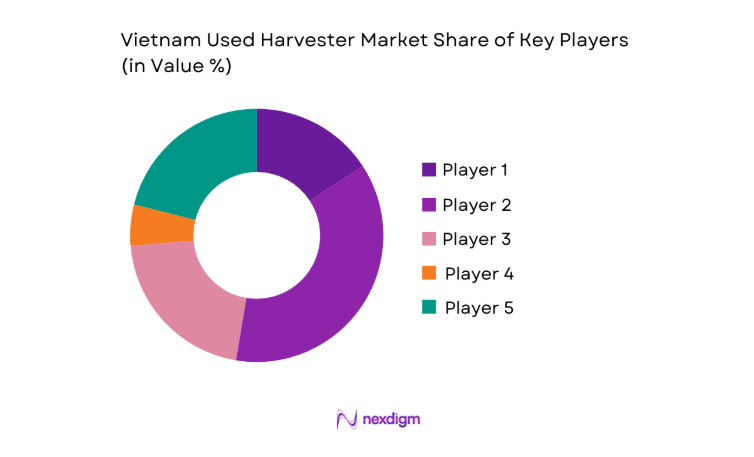

Competitive Landscape

The competitive environment is fragmented, with OEM-affiliated dealers, independent refurbishers, and regional traders shaping access, service quality, and refurbishment depth across key agricultural provinces.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Kubota Corporation | 1890 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Yanmar Holdings | 1912 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Iseki & Co., Ltd. | 1926 | Matsuyama, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| CLAAS Group | 1913 | Harsewinkel, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

Vietnam Used Harvester Market Analysis

Growth Drivers

Mechanization demand driven by rural labor shortages

Rural labor migration toward urban centers reduced the agricultural workforce by 320000 between 2022 and 2024, intensifying reliance on mechanized harvesting across rice-dominant provinces. Average farm plot consolidation increased to 1.9 hectares in 2024 from 1.6 in 2022, enabling more efficient equipment utilization. Seasonal labor availability during peak harvests fell by 18000 workers in key deltas in 2025, lengthening harvest windows without mechanization. Provincial mechanization programs expanded operator training capacity to 4200 trainees annually by 2024, improving machine uptime. Irrigated paddy coverage rose by 110000 hectares during 2023–2025, strengthening demand for reliable harvesting capacity.

Expansion of contract harvesting services and cooperatives

Registered agricultural service cooperatives increased by 740 between 2022 and 2025, expanding fleet-based harvesting coverage across multi-crop districts. Contract harvesting operations logged 2.6 million service days in 2024, reflecting rising outsourcing by smallholders seeking predictable harvest completion. Cooperative membership reached 3.1 million farmers in 2025, enabling pooled equipment utilization and maintenance scheduling. Provincial transport upgrades added 1280 kilometers of rural roads during 2023–2025, reducing machine relocation time across communes. Training certifications for machine operators expanded to 8600 recipients in 2024, improving safety and productivity. Seasonal demand peaks now align with coordinated service rosters, sustaining equipment utilization intensity.

Challenges

Quality inconsistency and lack of standard grading for used machines

Inspection pass rates for pre-owned harvesters varied widely, with 3100 units failing functional checks in 2024 due to drivetrain wear and hydraulic leakage. Dealer refurbishment protocols differ across 38 provinces, creating uneven performance outcomes and buyer risk. Field breakdown incidents reached 9400 cases during peak seasons in 2023–2025, increasing downtime and contractor penalties. Parts compatibility issues affected 2700 machines in 2024, extending repair cycles beyond 14 days in remote districts. Technical inspection capacity remained limited to 62 certified centers nationwide in 2025, constraining standardized grading coverage. Inconsistent maintenance histories undermine buyer confidence and elevate lifecycle uncertainty.

Limited access to affordable financing for smallholder farmers

Formal credit penetration among smallholders reached 41 in 2024, leaving significant reliance on informal lending with higher default risk. Average loan processing times exceeded 28 days in 2023, misaligning with narrow harvest windows that demand rapid equipment access. Cooperative-backed guarantees covered only 19000 farmers in 2025, restricting broader fleet acquisition. Collateral registration delays affected 24000 applications during 2024, slowing transactions. Rural banking outlets numbered 980 branches in 2025, limiting proximity for remote communes. Seasonal income volatility from climate variability disrupted repayment schedules for 120000 borrowers in 2023–2025, tightening lender risk thresholds and constraining equipment financing availability.

Opportunities

Formalization of certified refurbishment and grading programs

Provincial pilot programs accredited 26 refurbishment workshops by 2024, improving quality assurance and resale confidence. Standardized inspection checklists reduced post-sale failure incidents by 1800 cases in 2025. Technician certification programs expanded to 3100 participants during 2023–2025, strengthening refurbishment throughput. Digital service logs were adopted by 420 dealers in 2024, enabling traceability of maintenance histories. Warranty-backed resale schemes covered 8700 machines in 2025, lowering buyer risk and improving utilization reliability. Alignment with emissions compliance testing at 54 regional centers streamlined re-registration processes, shortening transaction cycles and improving channel credibility.

Digital marketplaces and price transparency for used harvesters

Active online listings for used harvesters surpassed 19000 in 2024, expanding discovery beyond provincial dealer networks. Platform-verified inspections covered 6200 machines in 2025, reducing information asymmetry for remote buyers. Average listing response times fell to 36 hours in 2023–2025, accelerating transaction velocity. Logistics coordination partnerships enabled 7800 cross-province deliveries in 2024, widening buyer reach. Digital escrow adoption reached 4100 transactions in 2025, strengthening trust. Mobile penetration across farming households reached 74 in 2024, supporting platform adoption and data-driven matching between machine specifications and field conditions.

Future Outlook

The Vietnam Used Harvester market is expected to advance steadily through 2035 as mechanization deepens across irrigated rice regions and cooperative-led service models mature. Policy enforcement on used equipment standards will shape refurbishment formalization and channel consolidation. Digital marketplaces and certified refurbishment are likely to professionalize transactions, while financing innovations and service bundling should expand access in underserved provinces. Climate variability and compressed harvest windows will further reinforce demand for reliable harvesting capacity.

Major Players

- Kubota Corporation

- Yanmar Holdings

- Iseki & Co., Ltd.

- CLAAS Group

- CNH Industrial

- AGCO Corporation

- Mahindra & Mahindra

- John Deere

- Sonalika International

- Kuhn Group

- Sampo Rosenlew

- Preet Agro

- Tafe Motors and Tractors

- LS Mtron

- Zoomlion Heavy Industry

Key Target Audience

- Agricultural service cooperatives and contractor fleets

- Smallholder farmer associations and producer groups

- Authorized agricultural machinery dealers

- Independent refurbishment workshops and traders

- Investments and venture capital firms

- Ministry of Agriculture and Rural Development

- Vietnam Register and provincial transport authorities

- Rural commercial banks and microfinance institutions

Research Methodology

Step 1: Identification of Key Variables

Field-relevant variables were defined around machine age, refurbishment depth, service coverage, parts availability, channel accessibility, and operator capacity. Regional cropping patterns, irrigation intensity, and harvest seasonality were mapped to determine demand clusters. Regulatory checkpoints and emissions compliance requirements were integrated to reflect transaction friction points.

Step 2: Market Analysis and Construction

Provincial-level transaction flows, refurbishment throughput, and service coverage were structured into an analytical framework. Channel performance indicators and logistics accessibility were layered to assess regional availability. Ecosystem maturity was constructed using dealer density, service center coverage, and operator training capacity.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on demand concentration, channel dominance, and refurbishment impact were validated through structured interviews with dealers, service contractors, and cooperative managers. Regulatory practitioners provided insights on compliance bottlenecks. Field technicians reviewed failure modes and maintenance cycles to validate quality risk assumptions.

Step 4: Research Synthesis and Final Output

Findings were synthesized into regionally differentiated insights aligned to operational realities. Cross-validation ensured consistency across channels, refurbishment practices, and service ecosystems. Strategic implications were distilled to support market entry, channel optimization, and service-led differentiation pathways.

- Executive Summary

- Research Methodology (Market Definitions and grading of used harvesters by age and condition, Primary interviews with used machinery dealers and refurbishers across Mekong Delta and Red River Delta, Farmer surveys on purchase behavior and financing for pre-owned harvesters, Analysis of import flows and customs data for used agricultural machinery, Telematics and service records from authorized service centers, Price tracking from auctions, online marketplaces, and dealer listings)

- Definition and Scope

- Market evolution

- Usage patterns and cropping seasonality

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Mechanization demand driven by rural labor shortages

Expansion of contract harvesting services and cooperatives

High new equipment prices increasing adoption of used units

Short harvesting windows for rice driving capacity needs

Growth in double and triple-cropping in irrigated regions

Availability of Japanese-origin used machinery supply - Challenges

Quality inconsistency and lack of standard grading for used machines

Limited access to affordable financing for smallholder farmers

High maintenance and spare parts availability for older models

Regulatory uncertainty on used machinery imports and emissions compliance

Low penetration of warranty and aftersales coverage

Fragmented dealer network in rural provinces - Opportunities

Formalization of certified refurbishment and grading programs

Digital marketplaces and price transparency for used harvesters

Dealer-backed financing and pay-per-harvest models

Localization of spare parts and remanufacturing hubs

Trade-in programs linked to OEM dealer networks

Expansion into underserved upland and coastal provinces - Trends

Rising preference for compact combine harvesters for paddy fields

Increased sourcing of used machines from Japan and South Korea

Bundling of service contracts with used equipment sales

Growth of cooperative ownership and rental fleets

Adoption of basic telematics retrofits for fleet management

Seasonal pricing cycles aligned with rice harvest peaks - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Harvester Type (in Value %)

Combine harvesters

Rice harvesters

Corn harvesters

Sugarcane harvesters - By Engine Power Class (in Value %)

Below 70 HP

70–120 HP

Above 120 HP - By Machine Age (in Value %)

Below 3 years

3–5 years

5–8 years

Above 8 years - By Refurbishment Level (in Value %)

As-is used

Dealer refurbished

OEM-certified refurbished - By Sales Channel (in Value %)

Authorized dealers

Independent used equipment traders

Auctions and marketplaces

Direct farmer-to-farmer - By Region (in Value %)

Mekong Delta

Red River Delta

North Central and Central Coast

Southeast

Central Highlands

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (product range, refurbishment capability, pricing bands, geographic coverage, financing availability, warranty terms, parts availability, service network reach)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Kubota Corporation

Yanmar Holdings

Iseki & Co., Ltd.

CLAAS Group

CNH Industrial

AGCO Corporation

Mahindra & Mahindra

John Deere

Sonalika International

Kuhn Group

Sampo Rosenlew

Preet Agro

Tafe Motors and Tractors

LS Mtron

Zoomlion Heavy Industry

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now