Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Vietnam Used Tractor market current size stands at around USD ~ million, reflecting a well-established secondary machinery ecosystem supported by import channels, refurbishment networks, and dealer-led resale models. Demand is anchored in replacement cycles among small and medium farms, cost-sensitive mechanization upgrades, and availability of reconditioned units aligned to local cropping systems. Market liquidity is sustained by active trade-in practices, seasonal purchasing behavior, and service-led sales propositions that extend equipment lifecycles across diverse agro-climatic zones.

Activity is concentrated in the Mekong Delta, Red River Delta, and Central Highlands, where dense irrigation networks, intensive rice and upland crop systems, and higher mechanization penetration create steady turnover of used equipment. Provincial hubs benefit from proximity to ports, bonded warehouses, and refurbishment clusters, improving access to imported inventory. Local policies supporting farm mechanization, alongside cooperative-led equipment sharing, reinforce demand concentration and foster mature dealer ecosystems with stronger aftersales capabilities and spare parts availability.

Market Segmentation

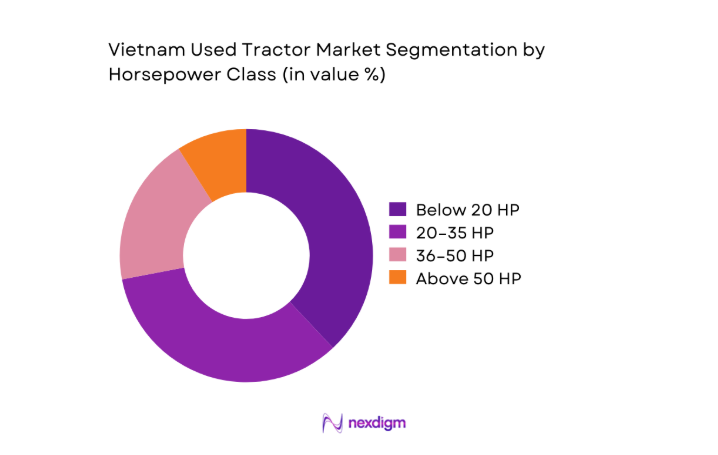

By Horsepower Class

Lower horsepower units dominate due to suitability for fragmented landholdings, narrow field access, and multi-crop rotations. Compact configurations enable maneuverability in paddy fields and small plots, while moderate power bands support diversified upland farming and light haulage. Buyers prioritize ease of maintenance, fuel efficiency, and compatibility with locally available implements. The prevalence of service providers further sustains demand for standardized power ranges that simplify fleet management and parts stocking. Dealer refurbishment programs favor popular power bands, ensuring higher availability and faster resale turnover. Seasonal workloads and cooperative sharing models reinforce preference for versatile horsepower classes that can be deployed across planting, tillage, and transport tasks.

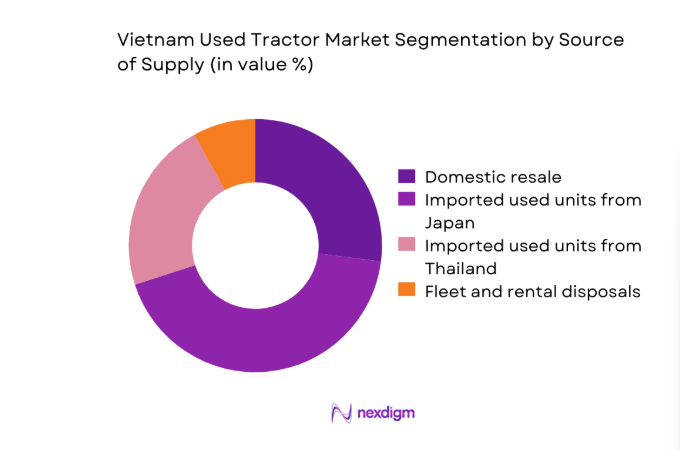

By Source of Supply

Imported used units lead supply due to consistent inflows of reconditioned equipment aligned with local preferences for reliability and durability. Dealer networks curate inventory from established refurbishment channels, improving quality assurance and parts compatibility. Domestic resale remains active within provincial clusters, supported by trade-ins from contract service providers and cooperative fleets. Fleet and rental disposals add episodic volumes, often bundled with service histories that improve buyer confidence. The source mix reflects logistics access to ports, refurbishment capacity in peri-urban hubs, and the maturity of broker networks that aggregate demand from rural districts. Supply continuity benefits from established inspection protocols and documentation practices.

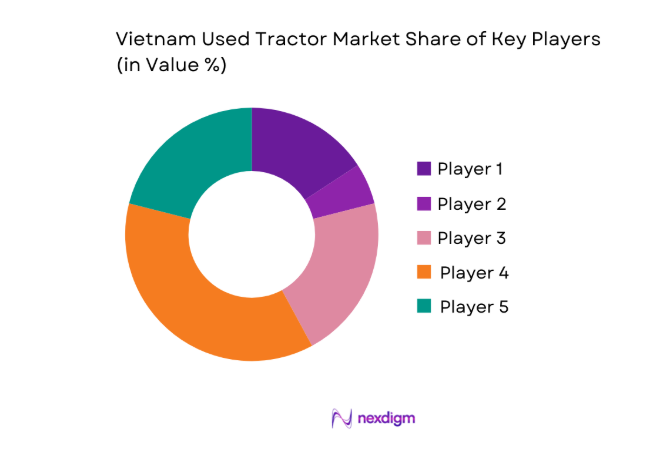

Competitive Landscape

The competitive environment is shaped by authorized dealers, independent refurbishers, and regional trading houses that curate imported inventory and provide localized service coverage. Differentiation centers on refurbishment depth, warranty offerings, parts availability, and field service responsiveness, with channel strength across provincial hubs influencing buyer trust and repeat purchases.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Kubota Vietnam | 2008 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ | ~ |

| Yanmar Vietnam | 2015 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ | ~ |

| ISEKI Vietnam | 2012 | Hanoi | ~ | ~ | ~ | ~ | ~ | ~ |

| Vikyno Group | 1981 | Ho Chi Minh City | ~ | ~ | ~ | ~ | ~ | ~ |

| Truong Hai Auto Corporation | 1997 | Quang Nam | ~ | ~ | ~ | ~ | ~ | ~ |

Vietnam Used Tractor Market Analysis

Growth Drivers

Rising mechanization in smallholder rice farming

Irrigated rice areas expanded in several delta districts supported by canal rehabilitation completed in 2022 and 2023, improving field accessibility for mechanized tillage. Local authorities recorded 146 new cooperative service units in 2024, enabling shared access to equipment for land preparation and transport. Rural labor availability declined in 2022 and 2023 as 312000 workers migrated to industrial zones, intensifying demand for mechanized solutions. Provincial road upgrades added 1240 kilometers of all-weather access by 2024, reducing downtime for field-to-village movements. Extension programs trained 18200 operators in 2025, improving utilization intensity across cropping cycles.

High price gap between new and used tractors

Household credit uptake for durable farm equipment increased through subsidized lending windows introduced in 2023, yet new equipment affordability remained constrained for small plots. Agricultural banks approved 68400 equipment-related loans in 2024, with repayment tenors aligned to seasonal cash flows. Import inspections cleared 21800 refurbished units in 2022 and 2023 combined, expanding accessible alternatives. Provincial mechanization plans targeted 91 districts in 2024, prioritizing rapid deployment of workable assets. Operator training centers certified 6400 mechanics in 2025, improving maintenance outcomes and extending service life, reinforcing buyer confidence in refurbished equipment pathways.

Challenges

Inconsistent quality and lack of certification standards

Border inspection protocols recorded 327 consignments flagged for documentation inconsistencies in 2022 and 2023, creating uneven quality screening across entry points. Provincial workshops varied in refurbishment practices, with 41 inspection criteria applied in some hubs versus 19 in others during 2024 audits. Local testing facilities completed 1860 safety checks in 2025, insufficient for nationwide coverage. The absence of unified grading frameworks complicates resale transparency, increasing transaction friction for rural buyers. Training throughput for certified inspectors reached 420 in 2024, lagging the scale of inflows. These gaps elevate verification burdens for dealers and prolong sales cycles across provinces.

Limited access to formal financing for used equipment

Rural credit programs expanded branch coverage by 128 locations during 2022 and 2023, yet documentation requirements constrained approvals for refurbished assets. Microfinance disbursements supported 76400 farm borrowers in 2024, though collateral standards limited eligibility for equipment older than 8 years. Cooperative guarantees covered 2190 transactions in 2025, improving access but remaining localized. Mobile banking adoption reached 41 rural districts by 2024, enabling payments but not asset-backed lending. Credit officers received 960 hours of training in 2023 to assess refurbished equipment risk, indicating institutional learning curves that slow wider financing inclusion.

Opportunities

Dealer-led refurbishment and warranty programs

Provincial trade departments licensed 312 refurbishment workshops by 2024, enabling standardized reconditioning protocols aligned with safety inspections. Warranty uptake increased across dealer networks, with 17400 units covered in 2023 and 2024 combined, reflecting buyer preference for risk mitigation. Training partnerships certified 2850 technicians in 2025, improving turnaround times for reconditioning cycles. Logistics hubs expanded warehousing capacity by 96 sites during 2022 and 2023, reducing lead times between import clearance and showroom availability. Digital service logs adopted by 148 dealers in 2024 improved traceability, supporting resale transparency and building confidence in certified programs.

Financing partnerships with rural banks and MFIs

Memoranda between provincial cooperatives and lenders increased from 34 in 2022 to 112 in 2024, facilitating bundled credit for equipment and maintenance. Pilot guarantee schemes covered 5200 transactions in 2023, lowering risk thresholds for refurbished asset lending. Mobile onboarding enabled 26800 rural applicants to submit documentation in 2024, shortening approval cycles. Training for credit assessors reached 1180 participants by 2025, improving appraisal consistency. Branch-level service points expanded to 67 communes in 2023, enhancing reach for seasonal borrowers. These mechanisms support scalable access pathways without distorting procurement behaviors.

Future Outlook

Over the coming decade, continued mechanization programs, rural infrastructure upgrades, and the professionalization of refurbishment services will support steady circulation of used tractors. Regulatory alignment on inspection standards and financing frameworks is expected to improve buyer confidence. Digital marketplaces and service bundling will further streamline discovery and aftersales engagement, strengthening provincial dealer ecosystems.

Major Players

- Kubota Vietnam

- Yanmar Vietnam

- ISEKI Vietnam

- Mitsubishi Agricultural Machinery

- Siam Kubota Corporation

- Vikyno Group

- Vinapro Co., Ltd.

- An Phat Machinery JSC

- Truong Hai Auto Corporation

- Tan Thanh Agricultural Machinery

- Hoa Phat Machinery

- Viet Nhat Machinery Trading

- Thanh Dat Agricultural Equipment

- Minh Phat Machinery Co., Ltd.

- Phu Thai Machinery

Key Target Audience

- Smallholder farmers and cooperatives

- Contract farming service providers

- Agricultural machinery dealers and refurbishers

- Equipment rental and fleet operators

- Spare parts distributors and service workshops

- Agribusiness processors with captive farming operations

- Investments and venture capital firms

- Government and regulatory bodies with agency names

Research Methodology

Step 1: Identification of Key Variables

The study defines technical variables covering tractor age, horsepower classes, refurbishment depth, service network coverage, and channel structures. Contextual variables include regional cropping systems, infrastructure access, and policy alignment shaping demand. Data parameters focus on transaction flows, utilization patterns, and maintenance intensity across provinces.

Step 2: Market Analysis and Construction

Primary field inputs from dealer audits and workshop assessments are triangulated with institutional indicators on mechanization programs and rural infrastructure deployment. Regional demand clusters are mapped to logistics access and service density to construct province-level dynamics without relying on aggregate scale disclosures.

Step 3: Hypothesis Validation and Expert Consultation

Findings are validated through structured consultations with provincial trade officials, cooperative managers, and certified technicians. Operational constraints, inspection practices, and financing workflows are stress-tested against observed transaction frictions to refine causal linkages underpinning demand and supply continuity.

Step 4: Research Synthesis and Final Output

Insights are synthesized into thematic narratives across segmentation, competition, and adoption pathways. The final output integrates policy context, institutional capacity, and operational realities to provide actionable perspectives for stakeholders evaluating refurbishment, financing partnerships, and channel expansion strategies.

- Executive Summary

- Research Methodology (Market Definitions and used tractor classifications by horsepower and age, Dealer and broker transaction audits across Mekong Delta and Red River Delta, Import auction data tracking from Japan and Thailand, Farm owner surveys by crop type and mechanization stage, Price benchmarking across refurbished and as-is units, Spare parts and service network mapping)

- Definition and Scope

- Market evolution

- Usage patterns by farm size and crop systems

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising mechanization in smallholder rice farming

High price gap between new and used tractors

Availability of imported Japanese reconditioned units

Labor shortages and aging rural workforce

Expansion of contract farming and service providers

Improving rural road connectivity enabling tractor mobility - Challenges

Inconsistent quality and lack of certification standards

Limited access to formal financing for used equipment

High maintenance costs for older imported models

Fragmented dealer and broker network

Spare parts availability variability by brand and age

Regulatory uncertainty on emissions and import rules - Opportunities

Dealer-led refurbishment and warranty programs

Financing partnerships with rural banks and MFIs

Growth of custom hiring centers in rural districts

Digital marketplaces for used farm machinery

Demand from emerging mechanization zones in upland regions

Localization of spare parts supply chains - Trends

Shift toward compact four-wheel tractors for diversified farms

Increasing preference for Japanese-origin brands

Bundled sales with service contracts and spare parts

Adoption of mobile-based listing and price discovery

Rising trade-in programs by authorized dealers

Growth of rental fleets transitioning assets to resale - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Horsepower Class (in Value %)

Below 20 HP

20–35 HP

36–50 HP

Above 50 HP - By Tractor Type (in Value %)

Two-wheel tractors

Four-wheel compact tractors

Utility tractors

Row-crop tractors - By Source of Supply (in Value %)

Domestic resale

Imported used units from Japan

Imported used units from Thailand

Fleet and rental disposals - By Condition and Refurbishment Level (in Value %)

As-is condition

Dealer refurbished

Certified pre-owned with warranty - By End Use Application (in Value %)

Rice cultivation

Upland crop farming

Horticulture and plantations

Aquaculture and pond maintenance

Transport and haulage - By Region (in Value %)

Red River Delta

Northern Midlands and Mountains

North Central and Central Coast

Central Highlands

Southeast

Mekong Delta

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (brand reputation, dealer network reach, refurbishment quality, warranty coverage, spare parts availability, pricing competitiveness, financing tie-ups, aftersales service footprint)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Kubota Vietnam

Yanmar Vietnam

ISEKI Vietnam

Mitsubishi Agricultural Machinery

Siam Kubota Corporation

Vikyno Group

Vinapro Co., Ltd.

An Phat Machinery JSC

Truong Hai Auto Corporation

Tan Thanh Agricultural Machinery

Hoa Phat Machinery

Viet Nhat Machinery Trading

Thanh Dat Agricultural Equipment

Minh Phat Machinery Co., Ltd.

Phu Thai Machinery

- Demand and utilization drivers

- Procurement and negotiation dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now