UAE Corporate Tax

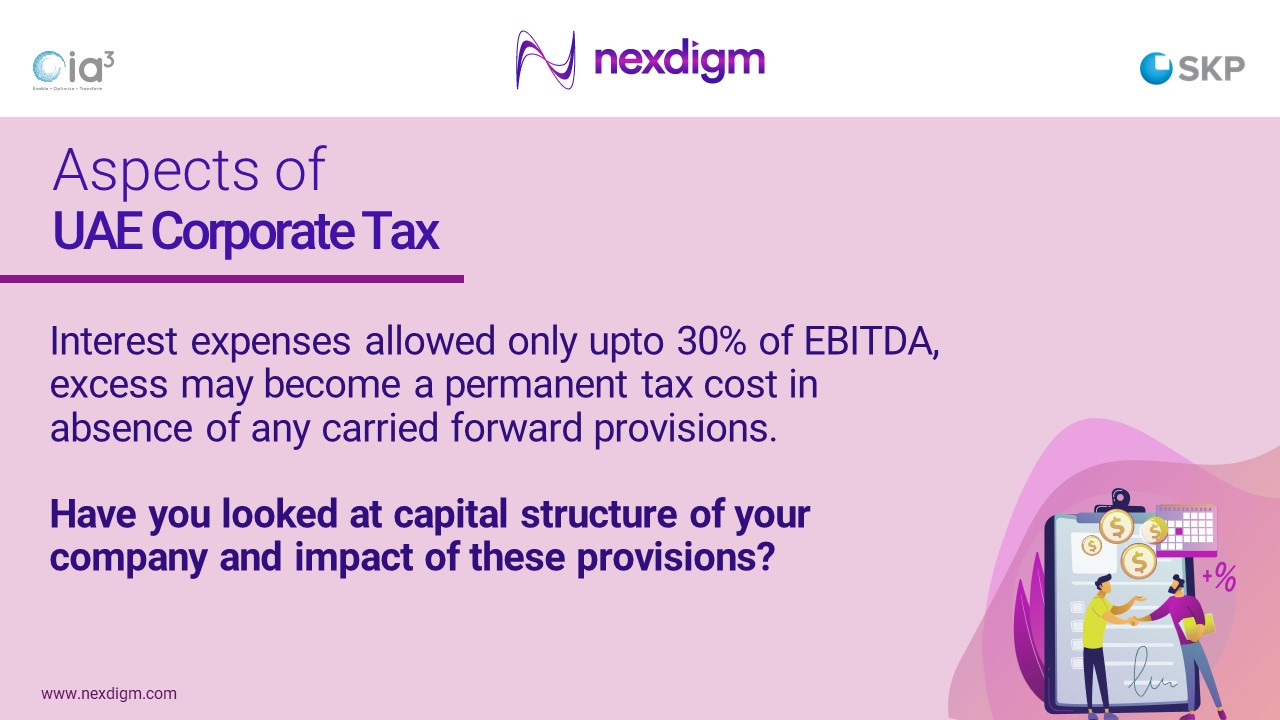

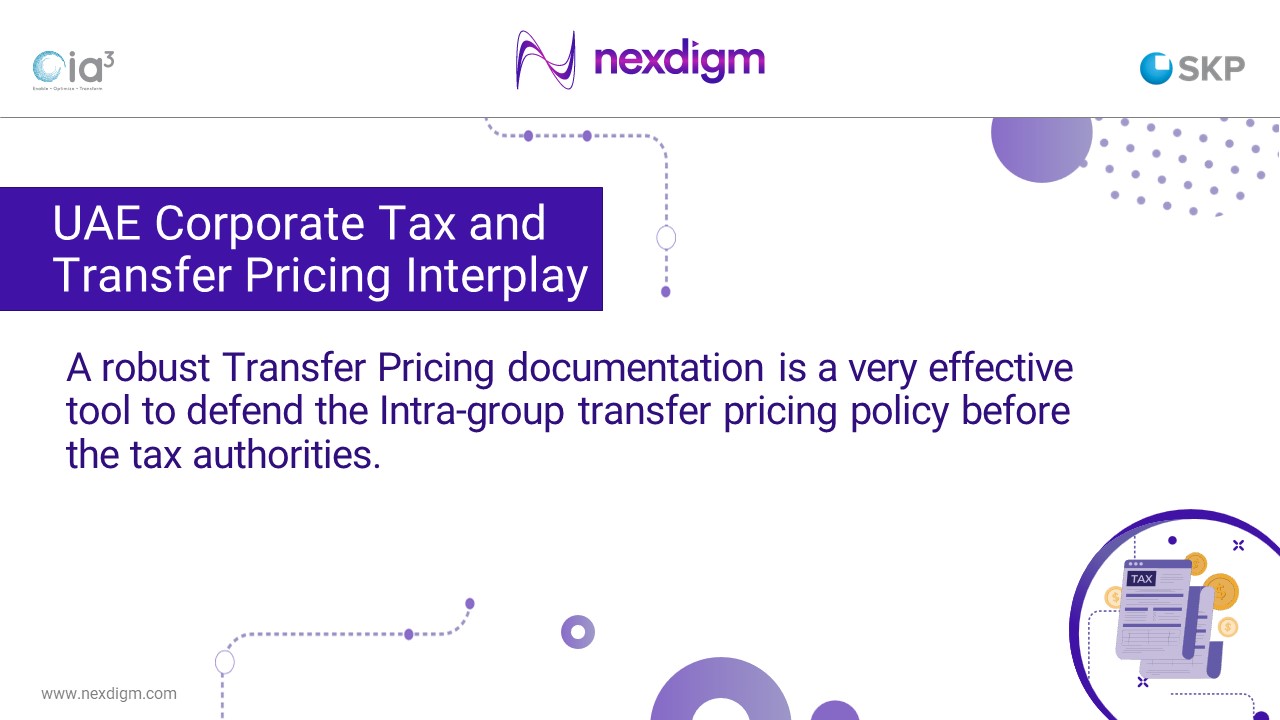

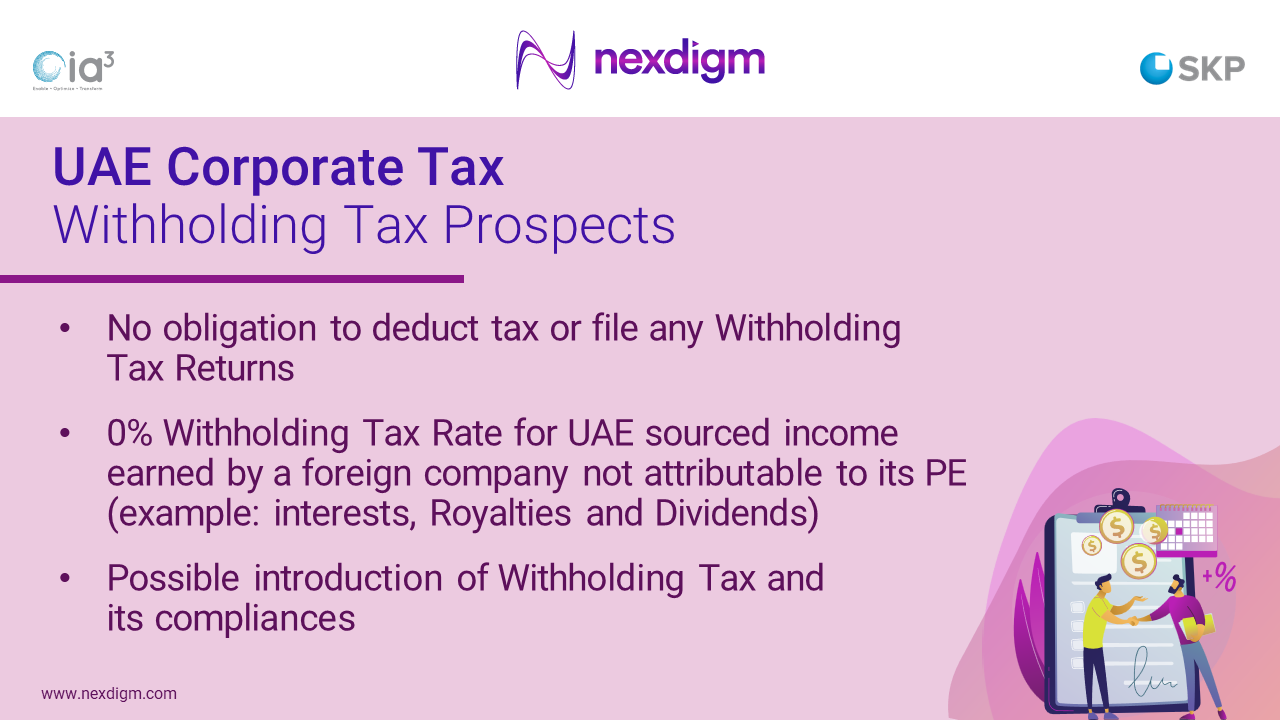

With the introduction of the UAE Corporate Tax law, the UAE Tax and Transfer Pricing landscape is expected to witness significant changes. Moreover, the law aims to ensure that only business or business-related activity income is taxed while ensuring that personal income, notably from employment, investments, and real-estate (without licensing requirements), is not subject to UAE Corporate Tax.

However, the Transfer Pricing will become crucial as inter-company and intra-group transactions will be impacted and undertaken at arm’s length. More importantly, there would be an increased tax and compliance burden on the businesses, and any non-compliance or non-adherence is expected to attract heavy penalties.

Our Services

Impact Compliance

Assess organizational readiness and evaluate impact of CT and Transfer Pricing Law

Advise on the most tax-efficient corporate structure

Compliance Management

Assist in obtaining tax registration and assist in ongoing compliances, annual returns, and disclosures

Determining tax liability to be discharged

Transfer Pricing

Formulating a Transfer Pricing policy

Advising on tax-efficient Transfer Pricing strategies

Assistance in preparing and filing disclosure forms

Preparing Transfer Pricing documentation as required by CT Law

Insights

UAE Transfer Pricing Disclosure: What You Need to Know

10 October 2024

UAE Corporate Tax Regime: Impact on Free Zone Entities

20 February 2024

How Holding Companies Could Hold

Ground under UAE Corporate Tax

12 February 2024

TP Guide 2023 A Disquisition to UAE TP Rules

8 February 2024

Corporate Tax Registration

of Juridical Persons

20 September 2023

Webinars

Determining Tax bill under UAE Corporate Tax law

UAE Corporate Tax and Transfer Pricing – Key Strategies

Uncovering the Intricacies of UAE’s CT Regime

UAE TP – Intra-group arrangements that could potentially hike your tax bill

Alerts

Summary of significant changes in Executive Regulations of Federal Decree-Law

7 October 2024

Key transfer pricing considerations on FTA’s guidance for determining taxable income

12 August 2024

FTA issues Public Clarification on Director, Manpower and Visa Facilitation Services

6 June 2024

Synopsis of the new Corporate Tax Guide for Free Zone Person

24 May 2024

FTA announces mandatory UAE Pass-based login on the EmaraTax portal from September 2024

8 May 2024

UAE provides timelines for making an application for Corporate Tax Registration

28 February 2024

Key Changes in Determining Qualifying Income of a Qualifying Free Zone Person

7 November 2023

Podcasts

Connect with Us

Nishit Parikh

nishit.parikh@nexdigm.com

Trupti Mehta

trupti.mehta@nexdigm.com

Imran A. Siddiqui

imran.siddiqui@nexdigm.com